How to Align Investment Goals with Risk Tolerance

Align goals with time horizons, evaluate risk capacity vs. willingness, choose asset allocation, diversify, and rebalance regularly.

Your investment success depends on balancing your goals with how much risk you can handle. Too much risk can lead to panic during market downturns, while too little risk might leave you short of your financial targets. Here's a quick roadmap to get started:

- Set Clear Goals: Define specific, measurable objectives like saving $50,000 for a home in 4 years or $1.2 million for retirement by age 65.

-

Categorize Goals by Time Horizon:

- Short-term (<5 years): Prioritize safety with cash or bonds.

- Mid-term (5–10 years): Use a mix of bonds and stable equities.

- Long-term (10+ years): Focus on growth with stocks or ETFs.

-

Assess Risk Tolerance:

- Risk Capacity: How much financial risk you can afford.

- Risk Willingness: Your emotional comfort with market swings.

- Match Investments to Goals: Align your portfolio’s asset allocation (stocks, bonds, cash) to your goals and risk tolerance.

- Review Regularly: Adjust your portfolio annually or after life changes to stay on track.

The key is creating a plan you can stick with, even during market ups and downs, to meet your financial milestones.

Define Your Financial Goals

Setting clear investment objectives is the first step toward building a portfolio that aligns with your needs. Vague goals like "save more money" or "build wealth" aren't actionable. As Vanguard explains:

Investment planning is the process of determining your financial goals and aligning your financial resources to meet them.

When your goals are specific, it becomes easier to design a strategy that fits. Clear objectives also help you match each goal with the right level of risk, making asset allocation more effective.

A good framework for setting goals is the SMART method: Specific, Measurable, Achievable, Relevant, and Time-based. For example, instead of saying "save for retirement", aim for something like, "accumulate $1.2 million by age 65 to provide $48,000 annually." Similarly, replace "buy a house someday" with "save $50,000 for a down payment within four years." This level of detail gives you a clear roadmap - how much to save each month and what returns your investments need to generate.

Writing down your goals can significantly improve your chances of success. Studies show that documented goals can boost success rates from 35% to over 70%. A simple document listing your goals, their target amounts, timelines, and progress tracking methods can help you stay focused. Regularly reviewing this document ensures you're on track.

Once you've defined your goals, the next step is to categorize them based on their time horizon.

Identify Short-Term and Long-Term Goals

Financial goals typically fall into different timeframes, each requiring a tailored approach. Short-term goals are those you aim to achieve within one to five years, such as building an emergency fund, saving for a vacation, or buying a car. Intermediate-term goals span five to ten years and might include saving for a home down payment or starting a business. Long-term goals go beyond ten years and often focus on retirement or wealth accumulation.

Why does this matter? Your time horizon dictates how much risk you can take. Short-term goals need low-risk investments to protect your capital, while long-term goals can handle more risk since there's time to recover from market fluctuations and benefit from compounding growth.

For retirement planning, Fidelity suggests specific savings milestones based on your age: save at least 1× your income by age 30, 3× by 40, 7× by 55, and 10× by 67. Retirees over 70 often spend over half their budget on essentials like housing (31–36%) and healthcare (up to 15.5%), so your savings need to account for these expenses.

| Goal Category | Time Horizon | Primary Objective | Typical Examples | Recommended Assets |

|---|---|---|---|---|

| Short-Term | < 5 years | Capital preservation, liquidity | Emergency fund, vacation, car | Cash, CDs, Money Market Funds |

| Mid-Term | 5–10 years | Balanced growth/income | Home down payment, education | Mix of bonds and stable equities |

| Long-Term | 10+ years | Growth, inflation protection | Retirement, legacy planning | Stocks, Equity Mutual Funds, ETFs |

This breakdown helps align your investment choices with each goal's risk and time horizon.

Prioritize Goals Based on Time Horizon

After defining your goals, rank them by importance and urgency. Not all goals carry the same weight - some are essential, while others are optional. Start by analyzing your monthly cash flow to understand how much you can allocate toward different objectives. Then, focus on the goals that are critical to your financial stability.

For example, building an emergency fund that covers three to six months of expenses is a key priority. This safety net prevents you from dipping into long-term savings during unexpected events. Similarly, paying off high-interest debt, like credit cards with rates of 18%–25%, should take precedence over investments that might only yield 5%–10%.

Your life stage also influences which goals take priority. Younger investors in their 20s and 30s might focus on retirement savings to maximize compounding over time. By their 40s and 50s, priorities often shift to funding college for children or accelerating retirement contributions. As retirement approaches, the focus typically transitions to income generation and preserving capital.

Experts recommend avoiding stock market investments for money needed within five years due to volatility risks. As your goals approach their target dates, gradually moving assets from stocks to safer options like short-term bonds or cash can help safeguard your savings. Revisit your priorities annually or after major life events - such as marriage, career changes, or unexpected challenges - to ensure your strategy stays aligned with your evolving needs.

sbb-itb-a9ac3c2

Assess Your Risk Tolerance

Once you've outlined your financial goals, the next step is figuring out how much risk you can handle. This involves evaluating both your financial capacity and emotional comfort with market fluctuations. Misjudging this balance can throw your entire plan off course - either by taking on too much risk and jeopardizing your objectives or by being overly cautious and falling short of what you need. Let’s dive into the key components of risk tolerance to help you make informed decisions.

Understand Risk Capacity vs. Risk Willingness

Risk tolerance is made up of two parts: how much risk you’re willing to take and how much risk you’re able to take. Risk willingness is about your emotional reaction to market drops, while risk capacity is determined by your financial situation and ability to absorb losses.

As Nevenka Vrdoljak, Senior Quantitative Investment Analyst at Merrill and Bank of America Private Bank, points out:

People tend to focus only on their comfort level with risk. But your ability to take risks based on your financial situation is just as important.

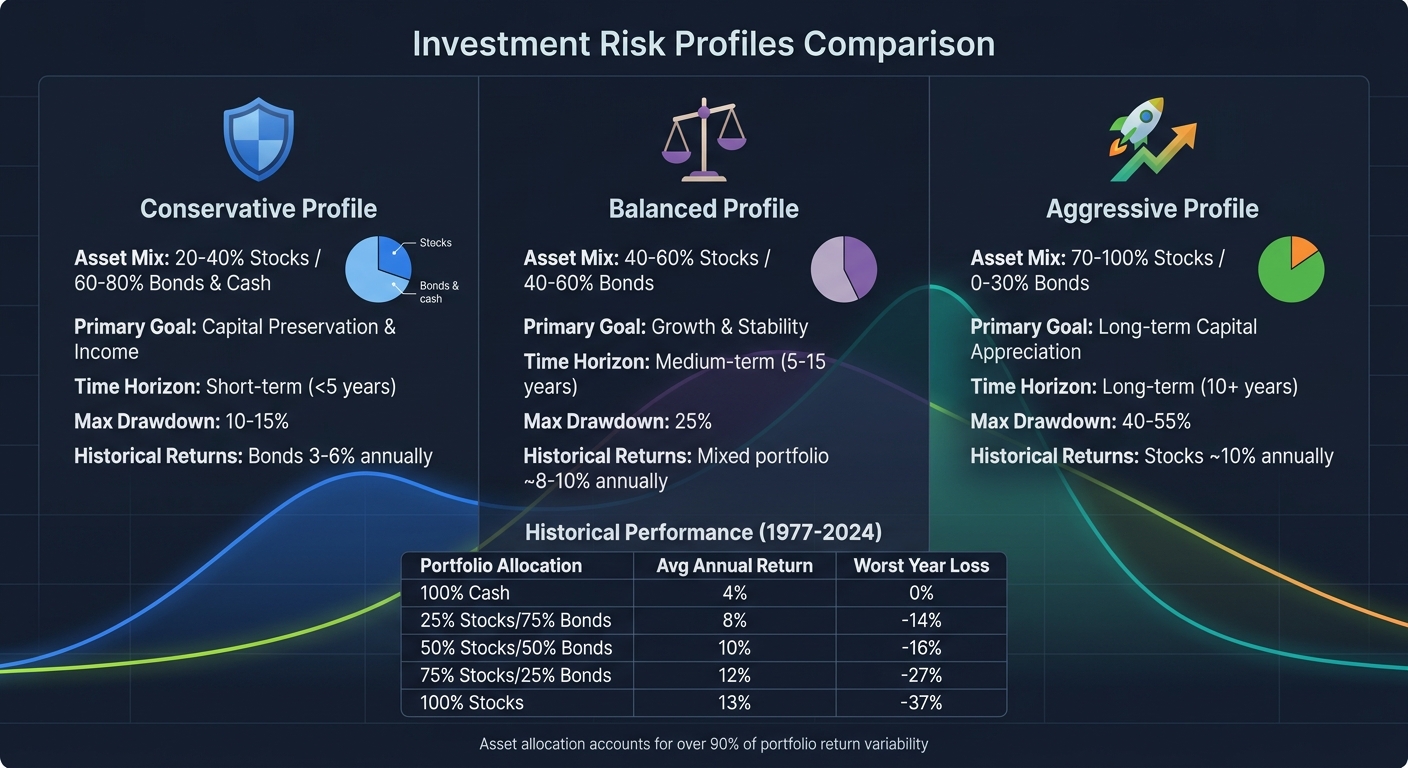

Risk capacity is influenced by factors like age, income stability, financial obligations, and your investment time horizon. For example, a 30-year-old with no dependents, steady income, and decades until retirement has a high capacity for risk. However, that same individual at 60, supporting aging parents and a child in college, would have much less capacity - even if their emotional comfort with risk hasn’t changed. Historical data shows that from 1977 to 2024, a portfolio of 100% equities delivered an average annual return of 13% but suffered a worst-year loss of 37%. In contrast, a balanced 50/50 portfolio averaged 10% annually with a worst-year loss of 16%.

Other financial responsibilities like a mortgage, children’s education, or elder care can also reduce your ability to handle downturns. Income stability plays a role too - a tenured professor generally has more capacity than a freelance consultant, even if their incomes are similar. Unexpected shocks, such as job loss or medical emergencies, can quickly lower your risk capacity.

A handy rule of thumb is the Rule of 110: subtract your age from 110 to estimate the percentage of your portfolio that should be in stocks. For example, a 25-year-old might allocate 85% to stocks and 15% to bonds or cash. If you’re comfortable with higher risk, you could use the Rule of 120, which suggests a 95% stock allocation for the same age. These are starting points, not hard rules, and should be adjusted based on your unique situation.

Use Tools and Scenarios for Self-Assessment

With a grasp of risk capacity and willingness, you can use practical tools like AI-powered portfolio analysis to measure your tolerance. Self-assessment tools often pose questions about hypothetical scenarios. For instance, how would you react if your portfolio dropped 20% in a year? If the thought of staying invested feels unbearable, your risk willingness may be lower than you assumed.

Scenario-based questions are another way to test your comfort level. For example, would you prefer a guaranteed return or a chance at a higher, but uncertain, payoff? Your answers can reveal how much risk you’re comfortable taking.

Anil Suri, Head of Asset Allocation and Portfolio Construction Analytics at Merrill and Bank of America Private Bank, highlights the importance of tying risk tolerance to personal goals:

Risk tolerance really comes to life when it's tied to a clear personal goal, not just as some general trait.

Reflecting on past behavior can also be telling. Think back to March 2020 - when markets plunged - how did you respond? Did you stay the course or sell in a panic? Your past actions often provide the clearest picture of your future tendencies. This isn’t about judgment; it’s about understanding your natural reactions to build a portfolio that can weather volatility. For self-directed investors, using portfolio intelligence tools can provide the clarity needed to manage these positions effectively.

Several tools can help formalize this process. The Schwab Intelligent Portfolios Investor Profile Questionnaire focuses on your behavioral tendencies and decision-making history. Vanguard’s Investor Questionnaire offers asset allocation suggestions based on your goals, time horizon, and risk tolerance. The University of Missouri’s 13-question assessment provides a research-backed score to help categorize your risk capacity. By combining these insights, you can align your financial ability and emotional comfort with actionable investment strategies.

Another approach is the "bucketing" strategy, which matches risk levels to specific goals. For example, your emergency fund should be in a low-risk, highly liquid bucket (like cash or money market funds), while retirement savings with a 20-year horizon can be invested more aggressively. This method allows you to tailor risk to individual goals rather than applying a single strategy across your entire portfolio.

| Portfolio Allocation | Average Annual Return (1977-2024) | Worst Year Loss |

|---|---|---|

| 100% Cash | 4% | 0% |

| 25% Equities / 75% Fixed Income | 8% | -14% |

| 50% Equities / 50% Fixed Income | 10% | -16% |

| 75% Equities / 25% Fixed Income | 12% | -27% |

| 100% Equities | 13% | -37% |

Finally, it’s crucial to reassess your risk capacity after major life events like a job loss, medical emergency, or financial windfall. Even if your emotional comfort with risk remains unchanged, these events can significantly alter your financial ability to take risks. Regular reviews ensure your portfolio stays aligned with your current circumstances rather than outdated assumptions.

Match Investment Goals to Risk Profiles Using Asset Allocation

Investment Risk Profiles: Asset Allocation and Expected Returns by Time Horizon

Using your risk tolerance as a foundation, asset allocation transforms your financial goals into an actionable investment plan. This process - spreading your investments across stocks, bonds, and cash - is a major factor in how your portfolio performs, accounting for over 90% of return variability.

Different objectives require different approaches. For example, an emergency fund needs to be readily available and stable, making cash or money market funds the ideal choice. On the other hand, a retirement account with a 20-year timeline can take on more risk, benefiting from an equity-heavy portfolio. By combining your goals with your risk tolerance, you can create a personalized asset allocation strategy.

Conservative, Balanced, and Aggressive Profiles

Risk profiles help you determine how much market fluctuation you can handle and what kind of returns you can anticipate. Each profile comes with a specific mix of assets, tolerance for losses, and appropriate timeframes.

A conservative profile focuses on preserving your capital and generating steady income, prioritizing safety over growth. This approach typically includes 20%–40% in stocks and 60%–80% in bonds and cash. It's ideal for short-term goals (less than five years) or for retirees who want to avoid significant losses. The downside is lower returns - bonds historically yield 3%–6% annually, compared to stocks' 10%. A conservative portfolio generally has a maximum drawdown of 10%–15%, so if losses exceed that, it may mean you're taking on more risk than intended.

A balanced (moderate) profile aims to strike a balance between growth and stability. With 40%–60% in stocks and 40%–60% in bonds, this allocation is well-suited for medium-term goals, spanning five to fifteen years. Expect some price swings, with a maximum drawdown of around 25%, but also the potential for higher returns compared to a conservative strategy. This profile is a great fit for those who need growth but can't tolerate the volatility of an all-stock portfolio.

An aggressive profile is designed for long-term capital growth, accepting significant short-term volatility to maximize returns. With 70%–100% in stocks and little to no bonds, this strategy is best for goals more than ten years away. Be prepared for a maximum drawdown of 40%–55%, which requires both financial stability and emotional resilience to handle market downturns. The reward? Access to the stock market's historical annual returns of around 10%.

| Risk Profile | Typical Asset Mix (Stocks/Bonds) | Primary Goal | Time Horizon | Max Drawdown Tolerance |

|---|---|---|---|---|

| Conservative | 20%–40% Stocks / 60%–80% Bonds & Cash | Capital Preservation & Income | Short (<5 years) | 10%–15% |

| Balanced | 40%–60% Stocks / 40%–60% Bonds | Growth & Stability | Medium (5–15 years) | 25% |

| Aggressive | 70%–100% Stocks / 0%–30% Bonds | Long-term Capital Appreciation | Long (10+ years) | 40%–55% |

Adjust Asset Allocation for Goal Alignment

To keep your strategy on track, it's important to adjust your asset allocation as your goals and circumstances change. Regular rebalancing - restoring your portfolio to its target mix after market fluctuations - and recalibrating - updating your targets to reflect life changes - are key.

A glide path strategy gradually shifts your allocation from aggressive to conservative as your goal's target date approaches. For instance, a 20-something investor might start with 90%–100% in stocks, then reduce to 75%–85% in their 40s, 60%–70% in their 50s, and 40%–60% in retirement.

Kayla Rae Fernandez, CFP at California Financial Advisors, underscores the importance of staying consistent:

An investor's rebalancing strategy should remain relatively consistent over time.

One effective method is corridor rebalancing, which avoids over-trading by only making adjustments when an asset class drifts by a set percentage - typically 5% - from its target weight. For example, if your goal is 60% stocks but gains push it to 66%, it's time to rebalance. In taxable accounts, you can rebalance by directing new contributions to under-weighted assets instead of selling over-weighted ones, which can trigger capital gains taxes.

Major life events should also prompt a portfolio review. David Rae, President of DRM Wealth Management, advises:

If you have major life changes like a job change, marriage or divorce, additions to the family, or perhaps an inheritance, you should review and adjust your current financial plan.

For example, losing a job might lower your risk capacity, suggesting a shift toward bonds. Conversely, receiving an inheritance could allow for more aggressive investments. The key is to ensure your portfolio reflects your current situation, not outdated assumptions from years ago.

Build a Diversified Portfolio

After determining your asset allocation, the next step is to create a portfolio that spreads risk across various dimensions. Diversifying from a single asset to a portfolio of 20 can reduce volatility by about 40%. Most of this risk reduction occurs early - within the first 20-30 holdings - after which adding more assets yields smaller benefits.

Diversification works across asset classes (like stocks, bonds, real estate, and commodities), sectors (such as technology, healthcare, and energy), and regions (U.S., international, and emerging markets). Each category reacts differently to economic changes. For instance, bonds often perform well during recessions when stocks decline. As of February 2026, the S&P 500 had a price-to-earnings (P/E) ratio of 27.62, while small caps (IWM) traded at a lower 18.86, and value stocks (VOOV) stood at 23.87. This illustrates how different market segments can offer unique risk-return dynamics.

A core-satellite approach is a practical way to structure your portfolio. It involves dedicating 60-80% to broad, low-cost index funds like $VTI (U.S. total market), $VXUS (international stocks), and $BND (total bond market). The remaining 20-40% can target specific sectors or opportunities, allowing you to balance market-wide exposure with focused strategies. For example, an 80/20 stock-bond portfolio has historically captured around 90% of the stock market's returns while experiencing only about 70% of the volatility.

Once this diversified base is established, you can explore options strategies to further enhance income and manage risk.

Use Options Strategies for Income

Options strategies can complement diversification by generating income and managing risk. Covered calls and cash-secured puts are two popular methods. These strategies involve selling options premiums on stocks you already own or waiting to buy shares at a discount. Research on the Russell 2000 index over 182 months found that buy-write strategies delivered a total return of 263% (8.87% annually) compared to the index's 226% (8.11% annually), with 4.5% lower volatility.

For risk management, protective puts act like insurance, setting a floor against major losses. A collar strategy combines a protective put with a covered call, balancing limited risk with capped upside. For example, an investor holding Nvidia (NVDA) shares that climbed from $200 to $800 could buy an $800 put and sell a $900 call. This locks in a minimum exit price of $800 while still allowing gains up to $900 - protecting a 300% profit from a sudden market downturn. When using options, ensure that no single sector exceeds 25-30% of your total deployed capital to avoid concentrated risks.

Use ThetaEdge for Portfolio-Aware Analysis

For investors managing their own portfolios, ThetaEdge offers tools to align options strategies with individual goals and risk preferences. The platform connects to over 80 brokerages via read-only access, analyzing opportunities like covered calls, cash-secured puts, and protective strategies. It provides detailed evaluations, including strike price, expiration, premium, probability of assignment, breakeven points, and potential outcomes.

ThetaEdge also includes features like portfolio Greeks for analyzing overall exposure, income tracking with historical performance, and daily AI-generated opportunity summaries sent by email. Importantly, it does not execute trades or offer investment advice - decisions remain in your hands. This approach ensures options strategies enhance your broader diversification plan without compromising long-term objectives. With tools like ThetaEdge, you can confidently integrate income-generating tactics into a portfolio designed for both growth and risk management.

Review and Adjust Regularly

Once your asset allocation is set, the next step is to keep an eye on your portfolio and make adjustments as needed. Markets change, life happens, and your financial goals may shift over time. Without regular check-ins, your portfolio can stray from its intended balance. Research shows that if you don’t rebalance, your allocations can drift significantly, which might increase your overall risk.

Experts generally suggest reviewing your portfolio annually to manage costs and taxes effectively. Vanguard, for instance, recommends checking in every six months to strike a balance between managing risk and keeping costs low. Interestingly, studies indicate that whether you rebalance monthly, quarterly, or annually, the impact on average returns and volatility is nearly the same. However, annual rebalancing results in far fewer adjustments - about 93 over a lifetime compared to over 1,000 with monthly rebalancing.

Set Reassessment Triggers

Instead of relying solely on a calendar schedule, consider setting specific conditions that signal when it’s time to review your portfolio. One common approach is the 5/25 rule: rebalance if an asset class moves 5 percentage points away from its target allocation or 25% from its original weight. For example, if your target stock allocation is 60% and it drifts to 65%, that’s your cue to adjust.

Beyond market shifts, personal milestones can also signal the need for a portfolio review. Major life events - such as getting married, having a child, buying a home, or receiving an inheritance - can affect your risk tolerance or time horizon. Maura Humphreys, Senior Vice President of Financial Solutions at Fidelity, explains:

The amount of risk that's appropriate for a person's portfolio isn't set in stone. Your risk tolerance is dynamic and changes over time along with changes in your situation.

Additionally, sharp market movements can throw your portfolio off balance, requiring adjustments to keep your risk under control.

Make Adjustments to Maintain Alignment

To keep your portfolio aligned with your goals and risk tolerance, timely adjustments are key. When rebalancing, aim to minimize costs and taxes. You can use new contributions or dividend reinvestments to restore your target allocations. In taxable accounts, consider selling long-held assets to reduce tax impacts. Assets held for over a year qualify for lower long-term capital gains tax rates (0%, 15%, or 20%) compared to ordinary income rates.

Also, watch out for concentration risk. If any single stock or bond issuer makes up more than 5% of your portfolio, it may be time to trim that position to maintain diversification. Withdrawals can also be used strategically to reduce overweight positions. For those using options strategies, such as those analyzed with tools like ThetaEdge, it’s important to review your portfolio’s Greeks and income metrics to ensure these strategies align with your overall allocation without adding unintended risks.

Rebalancing regularly helps enforce a disciplined approach - selling assets that have risen in value ("sell high") and buying those that have dropped ("buy low"). This can reduce the temptation to make emotional decisions during market swings. By setting clear triggers and following a consistent process, you can keep your investments aligned with your changing financial goals.

Conclusion

Aligning your investment goals with your risk tolerance takes clarity, discipline, and regular reviews. Begin by setting clear goals based on your time horizon - short-term (1–3 years), medium-term (3–5 years), or long-term (5+ years). It’s also important to separate risk capacity (your financial ability to handle losses) from risk tolerance (your emotional comfort with uncertainty). Striking the right balance between these factors is key. You need to take on enough risk to achieve growth but avoid overexposure that could derail your plans during market downturns. This balance becomes the foundation for all future portfolio adjustments.

Once your goals are aligned with a conservative, balanced, or aggressive asset mix, the ongoing work begins. Portfolio performance relies heavily on maintaining your target allocations. As markets shift and your circumstances evolve, your portfolio will naturally drift. Regular reviews are essential to ensure your investments remain aligned with your objectives.

To complement your asset allocation, platforms like ThetaEdge provide tools that integrate options strategies while respecting your risk profile. Connecting to over 80 brokerages, ThetaEdge offers portfolio-aware risk analyses, including delta-based assignment probabilities, breakeven points, and annualized yields, helping you assess opportunities within the context of your overall strategy. Its risk profile filters (Conservative, Balanced, Aggressive) prioritize opportunities that match your comfort level, while "what-if" scenarios let you explore potential outcomes before committing capital.

FAQs

How do I calculate my risk capacity vs. risk willingness?

Risk capacity refers to your financial ability to absorb losses, determined by factors like your assets, income, and savings. On the other hand, risk willingness is about your emotional tolerance for market ups and downs. While they’re related, they don’t always align naturally.

To bring these two into harmony, start by evaluating your financial situation - how resilient are you to potential losses? Next, think about your emotional reactions to market swings. Do sharp declines make you anxious, or are you able to stay calm? Tools such as risk assessment questionnaires can help clarify where you stand on both fronts.

When you identify gaps between your financial reality and emotional comfort, you can adjust your portfolio accordingly. The goal is to find a balance that reflects both your financial strength and your peace of mind.

What asset mix fits my goal’s time horizon and risk profile?

Balancing growth and stability is key when deciding on the right asset mix. If your goals are long-term and you can handle more risk, leaning heavily into stocks might provide greater growth opportunities, though it comes with more volatility. On the other hand, if your goals are shorter-term or you prefer less risk, a more conservative approach - favoring bonds and cash - can help safeguard your principal while still aiming for some growth. The key is to adjust your allocation to fit your objectives and what feels right for you.

When should I rebalance or change my portfolio allocation?

When your portfolio's asset allocation strays noticeably from your target mix, it’s time to take action. This drift often happens because of market fluctuations or changes in your personal financial situation. Keeping a close eye on your portfolio is crucial - regular rebalancing ensures your investments stay aligned with your risk tolerance and long-term goals. By doing this, you maintain consistency with your original strategy and keep your risk level within a range you’re comfortable with.