Covered Calls and Index Returns: Study Insights

40-year analysis: covered calls lower returns but cut volatility, improve risk-adjusted results, and earn premiums in flat or high-IV markets.

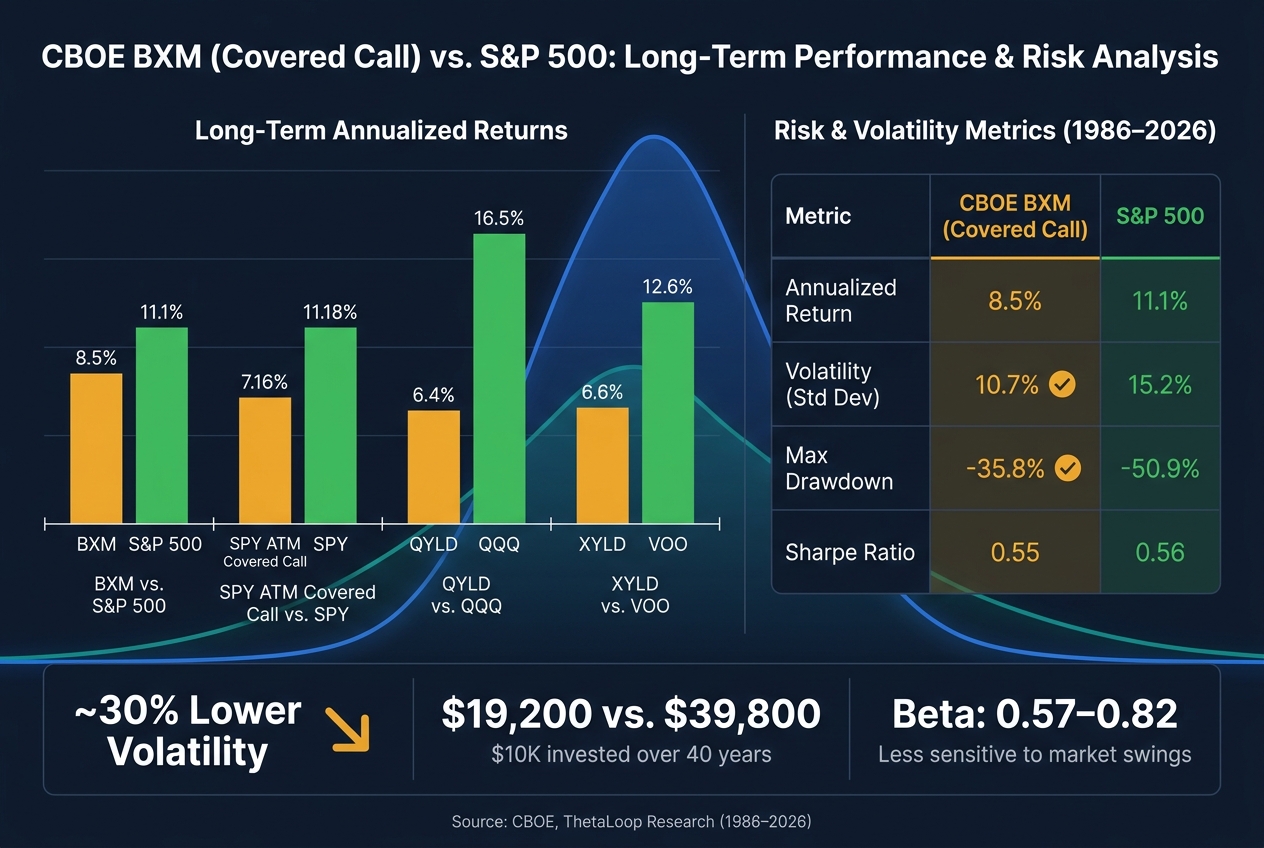

Covered calls offer a way to generate income by selling call options on stocks or indexes you already own. They reduce risk and volatility but limit upside returns. A 40-year analysis (1986–2026) shows the CBOE BuyWrite Index (BXM), a benchmark for covered call strategies, delivered 8.5% annualized returns, compared to 11.1% for the S&P 500. While covered calls underperform in bull markets, they provide steadier returns with lower volatility, making them attractive for income-focused investors.

Key Takeaways:

- Returns: Covered calls lag behind index returns in strong bull markets.

- Volatility: Reduced by ~30%, offering a smoother investment experience.

- Risk-Adjusted Performance: Higher Sharpe ratios due to lower drawdowns.

- Market Conditions: Perform better in flat or sideways markets but struggle in rapid recoveries.

- Premium Income: Higher premiums during periods of elevated implied volatility (IV).

Covered calls are best suited for those prioritizing steady income and reduced risk over maximizing growth. Strike selection and timing, particularly during high IV periods, are crucial for optimizing results. Using a covered call checklist can help ensure all variables are accounted for before execution.

Covered Calls vs. Index Benchmarks: How Returns Compare

Covered Calls vs. S&P 500: 40-Year Performance Comparison (1986–2026)

Long-Term Return Findings

When comparing covered call strategies to the S&P 500, the numbers tell a clear story: covered calls generally underperform in terms of raw returns, particularly during extended bull markets. The CBOE S&P 500 BuyWrite Index (BXM), a widely recognized benchmark for covered call performance, has delivered an 8.5% annualized return since June 1986, while the S&P 500 achieved 11.1% over the same period. That 2.6% annual difference may seem small, but it compounds significantly over time.

A 21-year backtest of a SPY at-the-money (ATM) covered call strategy reinforces this pattern, showing 7.16% annualized returns compared to 11.18% for SPY itself. The shortfall becomes more pronounced during strong rallies, as gains beyond the strike price are forfeited. This trade-off highlights the balance between generating income and sacrificing growth potential.

Interestingly, research has also identified a consistent trend: strategies targeting higher yields tend to deliver lower overall returns. Selling options closer to the money produces larger premiums but limits upside even more. As researchers Roni Israelov and David Ndong observed:

"We believe it is nearly irrefutable that higher derivative income covered call strategies should be expected to deliver lower returns."

Risk-Adjusted Performance

While covered calls may lag in raw returns, they shine in risk-adjusted performance. The premiums collected from selling calls act as a buffer against minor market declines, resulting in lower volatility and smaller drawdowns. For instance, the BXM has historically shown a standard deviation of 10.7%, compared to 15.2% for the S&P 500. Similarly, its maximum drawdown since 1986 was -35.8%, much less severe than the S&P 500’s -50.9%.

Additionally, option-writing indices like BXM, BXMD, and PUT have demonstrated betas ranging from 0.57 to 0.82 relative to the S&P 500. This means they are less sensitive to market swings. Over a 35-year period, these indices have achieved higher Sharpe and Sortino ratios than the S&P 500. The key here isn’t higher returns, but higher returns per unit of risk. For self-directed investors seeking smoother, more predictable performance, these metrics can be particularly appealing.

Fees, Costs, and Live Results

When moving from theoretical benchmarks to real-world ETFs, additional costs come into play, further eroding returns. Unlike benchmarks such as the BXM, live ETFs incur management fees and trading commissions, which can significantly impact results.

| Fund | Annualized Return | vs. Benchmark | Expense Ratio |

|---|---|---|---|

| QYLD (Nasdaq-100 Covered Call) | 6.4% | vs. QQQ: 16.5% | 0.60% |

| XYLD (S&P 500 Covered Call) | 6.6% | vs. VOO: 12.6% | - |

The performance gaps are striking. For QYLD, the annual return difference compared to QQQ is nearly 10 percentage points, while XYLD trails VOO by around 6 points. These gaps can’t be explained by fees alone. Factors like transaction costs from frequent option rolling, which is one of the key reasons to roll covered calls, tracking error, and return of capital distributions - where part of the yield is actually a return of your own principal - also contribute to the disparity.

As Morningstar aptly put it:

"Eye-catching premiums from covered-call funds are simply compensation for transforming risk."

For investors, the lesson is clear: don’t be swayed by high distribution yields alone. The total return after costs is the only metric that truly reflects the strategy’s effectiveness. These real-world considerations emphasize the need to evaluate net returns carefully when incorporating covered calls into your portfolio.

sbb-itb-a9ac3c2

How Market Conditions Affect Covered Call Performance

Looking at how market environments impact covered call strategies, it's clear that outcomes vary significantly depending on whether markets are rising, falling, or moving sideways.

Bull and Bear Market Outcomes

Market trends heavily influence how covered calls perform. In strong bull markets, the strategy’s capped upside can drag down returns. For instance, during the five strongest bull years between 2013 and 2023, the CBOE BuyWrite Index (BXM) lagged behind the S&P 500 by an average of 13.3 percentage points per year. That’s a notable trade-off for the income generated from premiums.

On the other hand, in flat or sideways markets, covered calls tend to shine. When the S&P 500 posted annual returns below 10% - as seen in years like 2011 and 2015 - the BXM outperformed by an average of 3.7 percentage points. Here, the premium income effectively turns into excess return since the underlying stock price doesn’t move much.

In bear markets, the strategy offers some protection, though it’s limited. During the downturns of 2008 and 2022, the BXM reduced losses by an average of 7.5 percentage points compared to the S&P 500. However, this cushion often feels modest when markets fall sharply.

V-shaped recoveries - where markets quickly rebound after a steep drop - pose a unique challenge. A striking example is 2020: while the S&P 500 surged 18.4%, the BXM fell 2.8%, creating a 21.2 percentage point gap, the largest underperformance in the index’s history.

Performance During Major Market Downturns

Historical downturns provide valuable lessons about the limits of covered calls. Take the 2008 financial crisis: from December 2007 (when the Invesco S&P 500 BuyWrite ETF, PBP, launched) to the market bottom in March 2009, SPY lost 52%, while PBP declined 39%. That’s a meaningful 13-point cushion. However, as Dan Hallett of HighView Financial Group pointed out:

"The upside that covered calls gave up was much larger than the downside cushion on the way down."

The COVID-19 market cycle in 2020 highlights this same imbalance. Between February 14 and March 20, the S&P 500 fell about 32%, while the BXM dropped 29%, offering a slight improvement. But during the recovery through August 7, the S&P 500 returned to its pre-crash level, while the BXM remained down roughly 13% because of its capped upside. The strategy softened the blow during the crash but missed out on the recovery gains.

Beyond general market trends, factors like implied volatility also play a key role in shaping the income potential of covered calls.

Implied Volatility and Premium Income

Implied volatility (IV) is a major factor in determining premium income. When IV is high, option prices rise, allowing covered call writers to collect more attractive premiums. Conversely, when IV is low, premiums shrink, sometimes to the point where they barely offset the capped upside.

Historically, covered call strategies outperform buy-and-hold approaches by 5–15% when IV is above the 50th percentile. A good example is the 2022 bear market: elevated volatility pushed premiums higher, enabling a 4% out-of-the-money SPY covered call strategy to generate 11.05% in annual option income, which helped offset capital losses.

That said, there’s a notable detail to consider: volatility skew. Institutional demand for downside protection inflates put option IV compared to call IV, meaning covered call premiums are often 10–20% lower than equivalent cash-secured put premiums. While higher IV helps, it doesn’t completely bridge this gap.

Understanding these dynamics allows investors to better evaluate the trade-offs of using covered calls. Analytical tools like ThetaEdge can provide deeper insights for those navigating these complexities.

Risk Profile and Trade-Offs of Covered Calls

Covered calls don't just affect your overall returns - they change how those returns are distributed. Grasping this shift is essential when deciding if this strategy aligns with your investment objectives.

How Covered Calls Reduce Volatility

One notable advantage of writing covered calls is the reduction in portfolio volatility. Data from the CBOE BuyWrite Index (BXM) over a 40-year span (1986 to 2026) shows 10.7% annualized volatility, compared to 15.2% for the S&P 500 - a drop of roughly 30%. The monthly premium income cushions the effects of market swings and minimizes volatility drag, which refers to the compounding penalty caused by large price fluctuations. For example, lowering volatility from 20% to 13% can add about 1.2% annually in compounding benefits. This reduced volatility helps stabilize returns, providing a smoother ride for investors.

The Upside Cap and Return Distribution

The trade-off? You give up the chance for significant gains during strong market rallies. If the stock or index surges past your strike price, those extra gains go to the option buyer. Historically, the S&P 500 has seen monthly gains exceeding 5% around 15–17% of the time, and covered calls miss out on those high-reward moments.

This creates what analysts call negative skewness in returns. In simpler terms, covered calls deliver steady, smaller profits but limit your ability to benefit from big market rallies, all while leaving you exposed to substantial losses during downturns. This balance of risks and rewards is reflected in key performance metrics that highlight the strategy's overall profile.

Key Risk Metrics to Know

To understand the long-term balance between risk and return, here’s a comparison of key metrics:

| Metric (1986–2026) | CBOE BXM (Covered Call) | S&P 500 Index |

|---|---|---|

| Annualized Return | 8.5% | 11.1% |

| Volatility | 10.7% | 15.2% |

| Max Drawdown | -35.8% | -50.9% |

| Sharpe Ratio | 0.55 | 0.56 |

Source: ThetaLoop Research

The maximum drawdown metric is especially revealing. A backtest of an at-the-money (ATM) covered call strategy on SPY showed a max drawdown of -36.62% over 21 years, compared to -55.20% for SPY alone. However, the Sharpe ratio - a measure of return per unit of risk - remains nearly identical (0.55 for covered calls vs. 0.56 for SPY), indicating that reduced volatility doesn't necessarily mean higher risk-adjusted returns at the index level.

A practical insight: out-of-the-money (OTM) covered calls often deliver better risk-adjusted outcomes than ATM calls. OTM calls allow for some upside participation, making them a better choice for investors seeking income rather than maximizing premium. Slightly OTM strikes can strike the right balance between income generation and capital appreciation potential.

Key Takeaways for Self-Directed Investors

Building an Effective Covered Call Strategy

One of the most critical choices in a covered call strategy is setting the strike price. Research suggests that selling out-of-the-money (OTM) calls - around 4% above the current stock price - tends to deliver better risk-adjusted results by preserving more potential upside. For instance, using a 4% OTM approach on SPY generated a median monthly income of 0.21%, but during the volatile 2022 market, this surged to an impressive 11.05%. This highlights how OTM strategies can still yield attractive premiums when market volatility rises.

Timing is equally important. AQR Capital Management emphasizes:

"If you have no view on implied volatility, there is no reason to sell options."

In practical terms, this means selling calls during periods of elevated implied volatility (IV), ideally when IV Rank exceeds 50, as this typically results in higher premiums. In contrast, low-IV environments may not provide enough incentive to justify the trade.

Balancing Income and Growth Goals

It's a common misconception that option premiums are straightforward income. As Larry Swedroe points out:

"The problem is that the premium is not income. Instead, it is a risk premium for shorting market volatility - an important distinction."

Historical data supports this perspective. A strategy targeting a 6% annualized yield on S&P 500 options from 1999 to 2023 actually resulted in an annualized loss of 0.60%. Pushing for a 12% yield fared even worse, with a 1.08% annualized loss. This pattern underscores how chasing higher premiums can erode overall returns.

To align your strike selection with your goals, consider the following approaches:

- For long-term growth, selling 10-delta calls (roughly a 10% chance of assignment) with 30 days to expiration allows for meaningful upside while still generating income.

- If you're more focused on income and risk reduction, selling closer to at-the-money calls can provide a higher premium buffer but significantly limits your upside.

Neither approach is inherently better - it all depends on your portfolio's objectives. These choices form the foundation for using tools that simplify the analysis process.

How ThetaEdge Supports Covered Call Analysis

Manually evaluating strike prices, monitoring IV conditions, and tracking risk metrics can be overwhelming. This is where ThetaEdge steps in, offering a tailored solution for self-directed investors.

The platform integrates with over 80 brokerages via secure, read-only access, presenting pre-screened covered call opportunities tailored to your holdings. Each opportunity includes detailed risk metrics, such as strike price, expiration, premium, assignment probability, breakeven level, and maximum potential outcome. Additionally, the Thetix AI assistant provides real-time answers to your questions using live market data and delivers a daily digest of new opportunities. Importantly, all trading decisions remain in your hands - ThetaEdge does not execute trades or offer investment advice.

Conclusion: Weighing the Pros and Cons of Covered Calls

Looking at the data, one thing is clear: covered calls are all about balance. Over the past 40 years, the CBOE BuyWrite Index (BXM) has provided annualized returns of 8.5% while reducing volatility by 30% compared to the S&P 500. To put that into perspective, a $10,000 investment in the BXM would have grown to about $19,200, whereas the same amount in the S&P 500 would have reached roughly $39,800. The trade-off? A smoother, less bumpy ride, but at the cost of significant long-term wealth accumulation.

The strategy's biggest shortfall becomes evident in strong bull markets. On average, the BXM underperforms by 13.3 percentage points during these periods. As ThetaLoop Research aptly states:

"Covered calls are not broken, but they are structurally disadvantaged in trending bull markets."

For those prioritizing capital preservation or steady income, however, covered calls can shine. Over the same 40 years, the BXM's maximum drawdown was –35.8%, offering a buffer compared to the S&P 500's –50.9%. This makes the strategy particularly appealing to retirees or investors managing concentrated positions they can't easily sell.

Here's a snapshot of how covered calls stack up against a buy-and-hold approach under different market conditions:

| Market Condition | Covered Call Result | Buy & Hold Result |

|---|---|---|

| Strong Bull Run | Capped gains; underperforms | Full participation; wins |

| Flat/Sideways | Premium adds alpha; wins | Minimal gains; loses |

| Bear Market | Premium cushions loss; wins | Full drawdown; loses |

| V-Shaped Recovery | Misses bounce; loses | Full participation; wins |

| High Volatility | Fat premiums; wins | Choppy returns; loses |

This table underscores the importance of understanding when covered calls align with your goals.

At their core, covered calls offer reduced volatility and consistent income, but they come with a trade-off: sacrificing the potential for outsized market gains. The key to success lies in choosing strikes and expirations that match your comfort with risk. Done thoughtfully, covered calls can be a valuable tool for those looking to prioritize stability over aggressive growth.

FAQs

What strike and expiration should I use for covered calls?

Selecting a strike price and expiration date comes down to balancing your comfort with risk and your view of the market. Research indicates that selling out-of-the-money (OTM) calls - like lower-delta options (e.g., 10-delta) - can provide a good mix of income potential and lower chances of assignment.

Some traders also incorporate Gamma Exposure (GEX) into their strategy. By aligning strike prices with levels where institutional investors might resist significant price moves, you can reduce the likelihood of assignment while keeping your portfolio adaptable. This approach adds another layer of precision to strike selection.

When does selling covered calls make the most sense?

Selling covered calls tends to shine in neutral to slightly bullish markets, where you're okay with limiting your upside in exchange for premium income. The strategy becomes even more appealing when implied volatility is elevated since higher volatility translates to larger premiums. It's especially effective in flat or sideways markets, as options often expire worthless, allowing you to pocket the premium. Additionally, during market downturns, the collected premiums can act as a cushion, helping to offset potential losses.

How do covered call ETF yields differ from total return?

The yield on covered call ETFs comes primarily from selling options, which generates income upfront. However, this income often comes at a cost - a potential loss when the options are settled. In contrast, total return reflects a broader picture, encompassing price changes, dividends, and distributions.

It's important to note that high yields can sometimes obscure an underlying issue: NAV erosion, or the decline in the ETF's share price. This happens because the strategy of selling options limits upside potential, effectively capping gains when the underlying asset performs well.

For investors, focusing solely on yield can lead to a "yield trap", where the high distributions come at the expense of reducing the ETF's principal value. To make informed decisions, it's crucial to evaluate total return rather than yield alone, ensuring a more accurate assessment of long-term performance.