IV Expansion Explained: Impact on Options Pricing

How implied volatility spikes raise option premiums, alter the Greeks, and shape selling, hedging, and timing strategies to manage risk.

When implied volatility (IV) rises, options become more expensive, regardless of stock price movement. This increase in IV, often triggered by events like earnings reports or economic data, boosts options premiums for both calls and puts. Traders need to understand how IV expansion affects pricing, strategies, and risks to make informed decisions.

Key takeaways:

- Higher IV = Higher Premiums: A 1% IV increase can raise premiums by 0.15%-0.35%.

- Timing Matters: Buying options during high IV can lead to losses if IV drops (IV crush). Selling options during high IV allows you to collect inflated premiums.

- Metrics to Watch: Use tools like IV Rank (IVR) and IV Percentile (IVP) to gauge whether options are overpriced or underpriced.

- The Greeks: Rising IV impacts Vega (sensitivity to IV changes), Theta (time decay), and Gamma (delta sensitivity), influencing profit and loss dynamics.

Strategies:

- Sell during high IV: Use iron condors, credit spreads, or covered calls to capitalize on inflated premiums.

- Hedge with positive Vega: Protective puts or calendar spreads can reduce risk during market turbulence.

IV expansion isn't just about price movement; it's about understanding and managing volatility's impact on your trades.

How IV Expansion Affects Options Pricing

Rising IV Increases Options Premiums

When implied volatility (IV) rises, options premiums increase for both calls and puts, even if the stock price remains unchanged. This happens because IV directly impacts an option's extrinsic (time) value. Higher volatility translates to greater uncertainty, which statistically raises the likelihood that an option will end up in-the-money. The Black-Scholes model reflects this by treating IV as the only variable that's inferred from market prices. When traders drive up options prices due to expected volatility, the model adjusts by assuming a higher IV to justify those elevated premiums.

A 1% change in IV typically shifts premiums by 0.15% to 0.35%, depending on factors like moneyness and time to expiration. At-the-money options experience the strongest impact because they carry the highest extrinsic value. These options represent the greatest uncertainty about whether they'll expire profitable.

To see this in action, compare low and high IV scenarios. When IV ranges between 15% and 25%, premiums reflect relatively stable market expectations. But when IV climbs to 30% or higher, the added "volatility premium" becomes noticeable. For instance, on October 31, 2024, Apple traded at $228.84 with a 30-day IV of 18.2%. A November 22 $230 call was priced at $2.10. By October 17, ahead of earnings, IV jumped to 28.6%, causing that same call to rise to $4.35 - a 107% increase - despite no movement in Apple's stock price.

Why IV Expansion Matters for Your Trading

Understanding how rising IV affects premiums can help you make smarter trading decisions. Buying options during periods of high IV often means overpaying for inflated extrinsic value, which can work against you even if your directional prediction is correct. A drop in IV could offset any gains from the stock's movement.

On the other hand, selling options in high-IV environments allows you to collect inflated premiums that decay in your favor as uncertainty diminishes. This is why experienced traders often target IV percentiles above 75% for selling strategies like covered calls or credit spreads, while reserving buying strategies for IV percentiles below 25%. The key is knowing whether you're paying a reasonable price or risking losses by being on the wrong side of volatility's fluctuations.

What Causes IV Expansion

Events That Trigger IV Spikes

IV expansion happens when the market braces for a big price move but lacks clarity on the direction. Binary events - scheduled announcements with uncertain outcomes - are the usual suspects. These events include earnings reports, interest rate decisions, drug approvals, and major economic data releases.

"A binary event is a specific, known future announcement or development that is expected to cause a significant, immediate, and dramatic movement in a stock price." - Interactive Brokers

To manage the risks of sudden price swings, market makers increase option prices ahead of such events. This creates a risk premium, which shows up as higher implied volatility (IV). For instance, in January 2024, before the Federal Reserve's February 1 interest rate decision, the iShares 7-10 Year Treasury Bond ETF (IEF) saw its 30-day historical volatility at just 8%, while its implied volatility shot up to 22% - nearly tripling as the market prepared for the announcement.

Unscheduled news can cause even sharper IV spikes. On Friday, October 10, 2025, news about tariffs and trade risks led to a steep market selloff. The at-the-money IV for short-dated S&P 500 options more than doubled from 11% to over 23% within hours. Similarly, geopolitical conflicts, government shutdowns, and other unexpected events inject sudden uncertainty, driving rapid IV increases. Beyond these events, shifts in market demand also play a role in IV changes.

Supply and Demand in the Options Market

IV isn't just influenced by events - it also responds to the forces of supply and demand. Option prices drive the changes, with increased demand pushing IV higher. When more traders buy options than sell them, premiums rise, prompting the mathematical models that calculate IV to adjust upward. This imbalance becomes especially noticeable during periods of market stress, as investors rush to buy protective puts to hedge against potential losses.

"When demand for something goes up, its prices follow suit. Traders are basically willing to pay extra for the opportunity to capture these potential gains. That's why options often become more expensive leading up to binary events." - Interactive Brokers

Downside put options generally carry higher IV than upside calls due to stronger demand for protection against losses. This is known as "volatility skew" and reflects investors' readiness to pay a premium to hedge against downside risks. During moments of widespread fear - such as the March 12, 2020 COVID-19 market crash, when the VIX soared to 82.69 - IV across most large-cap stocks tripled as traders scrambled to secure protective options.

How IV Expansion Changes the Greeks

How the Options Greeks Respond to Low vs High IV Environments

Vega and IV Changes

Vega reflects how much an option's price changes for every 1% shift in implied volatility (IV). For example, an option with a vega of 0.10 would gain $0.10 for each 1% increase in IV. This makes vega a key factor in profit and loss during periods of IV expansion.

Holders of long options benefit from rising IV since it increases the option's extrinsic value, while short option sellers may incur losses even if the underlying stock price stays the same. At-the-money (ATM) options carry the highest vega, whereas in-the-money (ITM) and out-of-the-money (OTM) options are less affected by IV changes.

The effect of vega grows with longer expirations. For instance, a 7-day option with a vega of 0.08 would gain about $0.40 from a 5% IV increase, while a 180-day option with a vega of 0.42 would rise by approximately $2.10 under the same conditions. This makes longer-dated options behave more like bets on volatility.

"When volatility shifts, Vega reshapes every other Greek." - StrikeWatch EA Research Team

IV expansion also impacts theta, as higher extrinsic value leads to faster decay before expiration. Conversely, an IV crush - such as one following an earnings announcement where IV might drop by 10–30 percentage points in a single session - can severely hurt long vega positions. For this reason, selling premium is generally recommended only when IV Rank exceeds 50, ensuring adequate compensation for the risk of negative vega exposure.

Delta and Gamma During IV Expansion

IV expansion doesn’t just influence vega; it also changes delta and gamma. As IV rises, the expected price distribution widens, increasing the delta of OTM options. This reflects the higher probability of the underlying stock reaching distant strike prices, making those options more sensitive to price changes.

Gamma undergoes noticeable changes during IV expansion as well. In low-IV environments, gamma tends to peak around ATM strikes. However, as IV increases, this peak spreads out across a wider range of strikes, resulting in lower gamma per strike but a broader impact overall. This wider distribution increases the chance of significant price moves, often requiring more frequent adjustments to maintain delta neutrality.

Take the example of a trader who purchased NVIDIA (NVDA) call options with a 0.30 delta when the stock was at $265 in March 2023. As NVDA surged to $390 over two months, delta climbed from 0.30 to 0.92 due to gamma acceleration, turning a $4 option into a $125 option. This illustrates how gamma-driven changes in delta can amplify the effects of IV expansion.

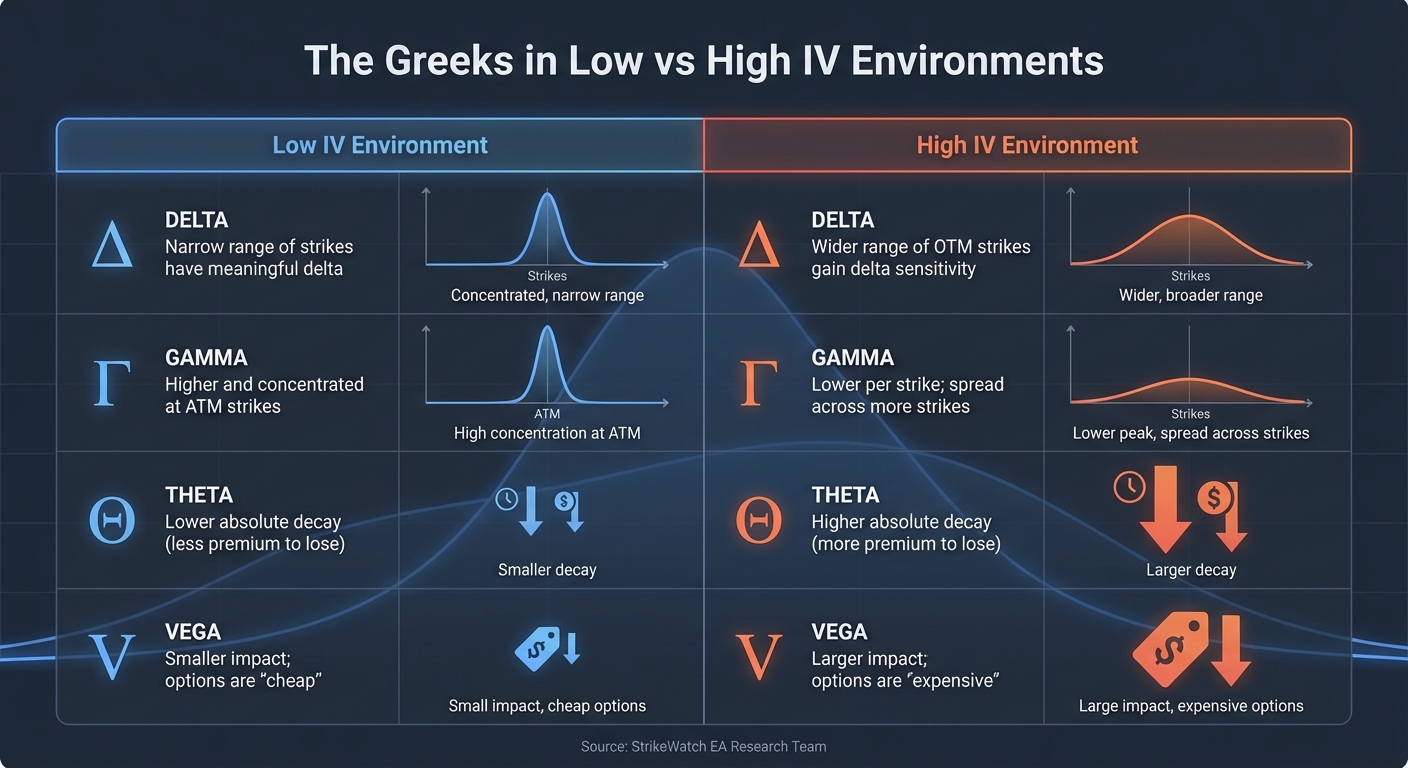

Here’s a comparison of how the Greeks behave in low versus high IV environments:

| Greek | Low IV Environment | High IV (Expanded) Environment |

|---|---|---|

| Delta | Narrow range of strikes have meaningful delta | Wider range of OTM strikes gain delta sensitivity |

| Gamma | Higher and concentrated at ATM strikes | Lower per strike; spread across more strikes |

| Theta | Lower absolute decay (less premium to lose) | Higher absolute decay (more premium to lose) |

| Vega | Smaller impact; options are "cheap" | Larger impact; options are "expensive" |

Source: StrikeWatch EA Research Team[12]

Experienced traders often close or roll short premium positions about 21 days before expiration to avoid the gamma spike that typically occurs as expiry nears. During high-IV periods, vega often dominates profit and loss calculations, sometimes offsetting directional gains or losses from delta. These dynamics highlight the importance of adapting options strategies to account for changing market conditions.

sbb-itb-a9ac3c2

Trading Strategies for IV Expansion

Selling Options During High IV

When implied volatility (IV) spikes, options premiums swell, creating opportunities for traders to capitalize on inflated prices. Defined-risk strategies like iron condors and iron butterflies are particularly effective in these conditions. These strategies allow traders to profit from expensive premiums while limiting the risk of large price swings or market gaps.

Timing is crucial in this approach. Selling options when the IV Rank is between 50% and 80% is often ideal. Below 50%, premiums tend to be too low to justify the risk, while above 80%, the likelihood of a volatility reversal increases significantly. For strike selection, targeting the 30-delta strike provides a balance, offering approximately a 70% probability that the options will expire worthless.

The choice of expiration dates also matters. For a balanced risk/reward, traders often aim for options with 30–45 days to expiration (DTE). For those seeking higher premiums with more risk, the 14–30 DTE range can be appealing, though it requires careful management.

"Timing is where the real edge lives. Miss the intersection of high IV and optimal DTE, and you're leaving 30-50% of potential premium on the table." – DaysToExpiry

Another way to generate income during IV expansion is by writing covered calls. Analytical tools like ThetaEdge can help traders identify opportunities that align with their portfolios, offering insights into risk/reward scenarios and alerts when positions reach a 50% profit threshold. This kind of data-driven approach can enhance trade management and improve overall returns.

Using IV Expansion for Hedging

While selling options takes advantage of high premiums, IV expansion can also be leveraged for portfolio protection. During periods of high volatility, protective puts gain value due to their positive vega, making them an effective form of insurance against market downturns. However, these puts are more cost-efficient when purchased in low-IV environments, allowing them to appreciate as volatility rises.

For portfolios with negative net vega (commonly referred to as "short volatility"), adding positions with positive vega can mitigate risk during market turbulence. For instance, when the VIX surges during extreme volatility spikes, traders might consider converting naked short positions into vertical spreads. This adjustment reduces negative vega exposure while capping potential losses.

Another hedging strategy involves calendar spreads, which are constructed by buying longer-dated options and selling shorter-term ones. This works particularly well when front-month IV is higher than back-month IV, allowing traders to take advantage of the disparity in volatility levels.

Measuring and Timing IV Expansion

Metrics for Tracking IV Levels

Understanding and identifying IV expansion involves more than just looking at raw volatility figures. One key metric is IV Rank (IVR), which places the current implied volatility (IV) within its 52-week range on a scale of 0–100. For instance, if NVDA’s IV is 45%, and its 52-week range spans from 30% to 90%, the IV Rank would be 25. However, a major drawback of IVR is its sensitivity to volatility spikes. A single extreme event can inflate the upper limit of the range, suppressing the IV Rank for months.

Another useful measure is IV Percentile (IVP), which calculates the percentage of the past 252 trading days during which the IV was lower than today’s level. For example, an IVP of 88 indicates that today’s IV is higher than 88% of the past year’s readings. Unlike IVR, IVP considers the entire distribution of IV, not just its extremes, making it a more balanced tool for strategy decisions. When IVR and IVP diverge by more than 30 points, it often indicates an irregular volatility history, suggesting that traders should manually review the data before making trades. Comparing IV to historical volatility can provide additional insights into option pricing.

"IV Percentile should be your primary volatility filter. It accounts for the full distribution of IV over the past year, not just the extremes." – Andy Crowder, The Option Premium

The IV vs. Historical Volatility (HV) spread is another critical comparison. This metric evaluates market expectations (IV) against actual past price movement (HV). If IV is at least 5 percentage points higher than HV, options are deemed "expensive", favoring premium-selling strategies. For short premium trades, traders often look for an IV Rank above 50 and an IV Percentile above 50 - ideally above 70. This dual-filter method has shown to improve success rates, with a win rate of 56.8% for iron condors, compared to 48.2% when IV filtering is not applied.

Using ThetaEdge for IV Analysis

Once you’ve identified key IV metrics, tools like ThetaEdge can help turn this data into actionable strategies. ThetaEdge offers advanced portfolio analytics, aggregating your total exposure across all positions. This allows you to see how IV expansion or contraction impacts your portfolio as a whole, rather than just individual trades. Its professional-grade analytics combine IV metrics with risk/reward scenarios, helping traders pinpoint opportunities like covered calls during periods of elevated volatility.

The platform’s Thetix AI assistant further simplifies decision-making by answering specific questions about your portfolio’s vega exposure and suggesting strategies tailored to current IV conditions. With daily AI-generated action plans, ThetaEdge helps traders time their entries and exits without requiring constant monitoring. When IV expansion creates opportunities to generate income on stocks you already own, ThetaEdge’s alerts ensure you capitalize on the moment when premiums are at their peak.

Key Takeaways

IV (Implied Volatility) expansion increases options premiums even if the stock price remains unchanged. On average, a 1% rise in IV boosts premiums by 0.15% to 0.35%. However, if IV collapses, even a correct directional trade can lose value. This highlights the need to monitor IV as closely as price movement.

The Greeks respond significantly to changes in IV. Vega measures how much an option's price changes with IV shifts, with at-the-money options being the most sensitive. As IV climbs, Theta accelerates time decay, which reduces the value of long options more quickly. Gamma also becomes more unpredictable near expiration, increasing the risk for short positions as Delta swings become harder to manage.

Context matters more than the raw IV number. A 35% IV reading is meaningless without understanding its relative position. Use IV Percentile as a key guide: when it's above 75%, options are expensive, favoring selling strategies like covered calls or credit spreads. When it's below 25%, options are cheap, making buying strategies more attractive. For instance, IV often spikes ahead of earnings due to volatility expectations, inflating premiums significantly.

Avoid buying short-dated options before major announcements. The post-event "IV crush" can wipe out directional gains. Instead, consider strategies like vertical spreads that minimize negative vega exposure or sell premium when IV Percentile is high (above 75%) to take advantage of inflated prices.

ThetaEdge simplifies IV management and portfolio adjustments. By combining IV data with portfolio-level risk insights, the platform tracks metrics like IV Rank and Percentile across all positions. It also aggregates Vega exposure and identifies high-premium opportunities during volatility spikes. The Thetix AI assistant provides tailored advice, answering questions about your portfolio's IV sensitivity and creating daily action plans to help you capture opportunities without constant manual tracking.

These insights emphasize the importance of timing and the value of tools like ThetaEdge for managing volatility effectively.

FAQs

How do I know if IV is “high” or “low” for a stock?

When evaluating whether a stock's implied volatility (IV) is "high" or "low", it's helpful to compare its current IV to its 52-week range. Tools like IV Rank and IV Percentile can simplify this process. A high IV Rank or Percentile indicates that the current IV is elevated compared to its historical levels, while a low value suggests it is subdued. These metrics offer a clear way to gauge how the current IV stacks up against the stock's past performance.

How can I avoid an IV crush around earnings?

To steer clear of an IV crush during earnings season, it's smart to adjust your options strategy ahead of the announcement. Steer clear of buying options too soon, especially when implied volatility (IV) is running high. After earnings, IV tends to drop sharply, which can erode the value of your options.

Instead, look at strategies that take advantage of this IV drop, such as selling options or spreads. Timing matters - enter your positions closer to the earnings release. This way, you limit your exposure to an IV collapse and keep potential losses in check.

Which options have the most vega risk during IV expansion?

At-the-money options with a longer time to expiration carry the highest vega risk during periods of implied volatility (IV) expansion. These options are particularly sensitive to changes in IV because vega is at its peak for them. As the expiration date extends further out, this sensitivity grows, amplifying their reaction to shifts in implied volatility.