How Option Assignment Works: Case Studies

Real-case breakdown of option assignment: how exercises, early assignments, and rolling strategies affect risk, cost basis, and returns.

Option assignment occurs when an option buyer exercises their right, requiring the seller to fulfill the contract terms. For call options, this means selling 100 shares at the strike price; for put options, it involves buying 100 shares at the strike price. The Options Clearing Corporation (OCC) facilitates this process, assigning exercises to brokers who allocate them to individual accounts. Understanding how assignment works helps traders manage risks, capital, and strategies effectively.

Key points:

- Assignment triggers: Options are exercised when in-the-money (ITM) - calls when the stock price exceeds the strike price, and puts when it's below.

- Automatic exercise: At expiration, options ITM by at least $0.01 are automatically exercised unless a "Do Not Exercise" (DNE) instruction is submitted.

- American vs. European options: American options allow exercise anytime before expiration, increasing the risk of early assignment. European options can only be exercised at expiration.

- Assignment stats: About 8–10% of options are exercised, 60% are closed early, and 30% expire worthless.

Case Study Highlights:

- Call assignment at expiration: Selling a covered call on Micron Technology resulted in locked gains but capped upside beyond the strike price.

- Put assignment below strike: A trader mitigated losses from a short put assignment by selling covered calls, lowering the cost basis and turning a loss into a small profit.

- Early assignment before ex-dividend: Early call assignment occurred due to low time value compared to an upcoming dividend, leading to unexpected share loss.

Managing Assignment:

- Risk management: Maintain sufficient capital to handle assignments and avoid margin calls.

- Strategies: Use covered calls or rolling strategies to reduce cost basis or manage positions.

- Tools: Platforms like ThetaEdge provide assignment probabilities and portfolio risk insights to help traders make informed decisions.

Assignment is a normal part of options trading. With proper planning, it can be managed effectively to align with your financial goals.

How Option Assignment Works

Let’s dive into how option style, clearing processes, and automatic exercise influence the outcomes in options trading.

American vs. European Options

The timing of assignment hinges on the option's style. American-style options, which apply to most individual stocks and ETFs, can be exercised at any point between purchase and expiration. This flexibility means there’s always the chance of early assignment, making it a factor to consider on any trading day.

On the other hand, European-style options, typically used for broad-market indices, can only be exercised at expiration. This removes the risk of early assignment and simplifies planning for capital needs. These differences play a key role in shaping how you manage risk and strategize your trades with portfolio intelligence.

The Options Clearing Corporation (OCC)

The OCC acts as the backbone of U.S. equity options trading, ensuring every contract is honored - even if one party defaults. Through a process called novation, the OCC steps in as the intermediary, replacing the original buyer-seller agreement with two new contracts. Essentially, the OCC becomes the buyer for every seller and the seller for every buyer.

"The OCC steps into the middle, becoming the buyer to every seller and the seller to every buyer." - Options Clearing Corporation (OCC)

When an option is exercised, the holder's broker notifies the OCC. The OCC then restructures the contract and assigns the exercise to a clearing member firm. This process underscores the OCC’s critical role in maintaining the integrity of the options market.

Automatic Exercise at Expiration

Beyond the OCC’s assignment process, expiration rules also shape how assignments play out. The OCC uses an exercise-by-exception rule to simplify the process: any option that’s at least $0.01 in-the-money is automatically exercised unless the holder submits a "Do Not Exercise" (DNE) instruction. The cutoff for submitting a DNE is 5:30 PM Eastern Time on expiration day, but many brokers enforce earlier deadlines.

A DNE request can make sense if transaction costs outweigh potential profits. Statistics show that about 10% of options are exercised, 60% are closed before expiration, and 30% expire worthless. It’s also worth noting that assignments can occur until 4:30 PM Eastern Time, which is 30 minutes after the market closes.

Understanding these mechanisms can help you navigate the nuances of assignment and make more informed trading decisions.

sbb-itb-a9ac3c2

Case Studies of Option Assignment

These examples showcase how option assignments play out in practice, highlighting their financial outcomes. Factors like timing and whether an option is in-the-money play a big role, and these scenarios illustrate how different market conditions can lead to varied results.

Case Study 1: Call Option Assignment at Expiration

In February 2026, an investor owned 100 shares of Micron Technology (MU) with a cost basis of $414.00 per share. On February 20, they sold a February 27 call option with a $435 strike price, earning a premium of $12.27 per share ($1,227 total). By the expiration date, MU's stock price had climbed to $439.00, making the option $4.00 in-the-money.

The OCC's automatic exercise rule kicked in, and the option was exercised. The investor's shares were called away at $435, resulting in a total profit of $3,327. This included a $2,100 stock gain plus the $1,227 premium. However, they missed out on an additional $400 they could have gained if the shares hadn't been capped at the strike price.

Takeaway: When an option finishes in-the-money, assignment at expiration is almost guaranteed. While the investor locked in gains and kept the premium, they sacrificed any upside beyond the strike price. To avoid last-minute decisions, consider closing short positions before the market closes on expiration day, especially if the stock price is close to the strike.

Case Study 2: Put Option Assignment Below Strike Price

Between October 2018 and April 2019, a trader dealt with a short put assignment involving XLE (Energy Select Sector SPDR Fund). On November 9, 2018, the trader was assigned 100 shares at a $73 strike price. At the time, XLE's price had dropped to $66, resulting in an immediate unrealized loss of $700 ($7.00 per share × 100 shares).

Rather than selling the shares at a loss, the trader opted to sell covered calls on the assigned shares over the next five months, collecting $7.55 per share in credits. This strategy reduced the effective cost basis from $73 to $65.45. When the position was finally closed on April 5, 2019, at $65.63, the trader managed to turn a small profit of $18 instead of facing a potential $1,300 loss.

"The key is to do the mechanics right, stick to the rules of position sizing, and manage your portfolio balance and total capital allocation." - Kirk Du Plessis, Founder, Option Alpha

Takeaway: Being assigned on a put means you must buy shares at the strike price, so having enough buying power is critical. Recalculate your breakeven immediately (strike price minus the premium collected), and consider selling covered calls to lower your cost basis. This tactic, often part of a strategy called "the Wheel", can turn a losing situation into a manageable one.

Case Study 3: Early Call Assignment Before Ex-Dividend

Early assignments can happen when a stock is about to pay a dividend, especially if the remaining time value of a call option is less than the dividend amount. A 2024 example from Option Alpha described a stock trading at $188.38 with a $0.72 dividend coming up. A $180 strike call had very little time value left, while the corresponding put option was priced at $0.44.

In this case, the call holder spotted an arbitrage opportunity. By exercising the call and simultaneously buying the put for $0.44, they could secure a $0.28 profit per contract from the $0.72 dividend. For the call seller, this resulted in an unexpected early assignment, meaning they lost the dividend they would have received had they held the shares past the ex-dividend date.

Takeaway: Keep an eye on the time value of your short calls as ex-dividend dates approach. If the time value is less than the dividend, early assignment becomes likely. This can lead to losing shares sooner than anticipated, along with potential margin calls or tax implications.

Managing Assignment Risk with ThetaEdge

ThetaEdge provides tools designed to help investors navigate the challenges of option assignments, which can quickly affect a portfolio. By offering detailed insights and proactive features, the platform equips users to manage these risks effectively.

Probability of Assignment Metrics

ThetaEdge highlights key data for every covered call and cash-secured put opportunities, including a delta-based assignment probability, premium, and breakeven information. For those prioritizing lower risk, the platform includes three adjustable risk profiles. For instance, the conservative profile automatically filters opportunities to aim for an assignment risk of around 15%.

"ThetaEdge surfaces what's happening in your portfolio. You decide what to do about it." - ThetaEdge

The platform’s interface allows users to compare strike prices, expiration dates, premiums, and assignment probabilities side by side. This streamlined layout eliminates the need to juggle multiple tools, enabling faster, more informed decisions. Additionally, ThetaEdge tracks portfolio Greeks to provide a deeper understanding of risk.

Portfolio Greeks and Risk Assessment

ThetaEdge’s analysis engine keeps tabs on Greeks, volume, open interest, and price momentum for all active positions. This daily monitoring offers a clear picture of overall exposure, particularly when multiple positions face assignment risk near the same expiration date. The platform also flags adverse market movements and rising assignment risks, ensuring investors can act on potential issues, such as impending ex-dividend dates. These insights are particularly useful when evaluating rolling strategies.

Roll Strategy Tools and Thetix AI

As positions approach expiration or hit profit targets - often set at 35% of maximum premium within ThetaEdge’s strategy profiles - the platform assesses roll opportunities. It provides credit/debit comparisons and tailored scenarios using Thetix AI. Thetix delivers concise, real-time recommendations and retains session context, allowing users to explore different options without re-entering data.

"Thetix... computes answers from your actual portfolio data and live market feeds. Verified numbers, clear explanations, not generated guesses." - ThetaEdge

ThetaEdge connects securely with over 80 U.S. brokerages via read-only OAuth 2.0 access. While it analyzes risk and highlights opportunities, it does not execute trades or move funds, leaving all decision-making entirely in the investor’s hands.

Key Takeaways and Conclusion

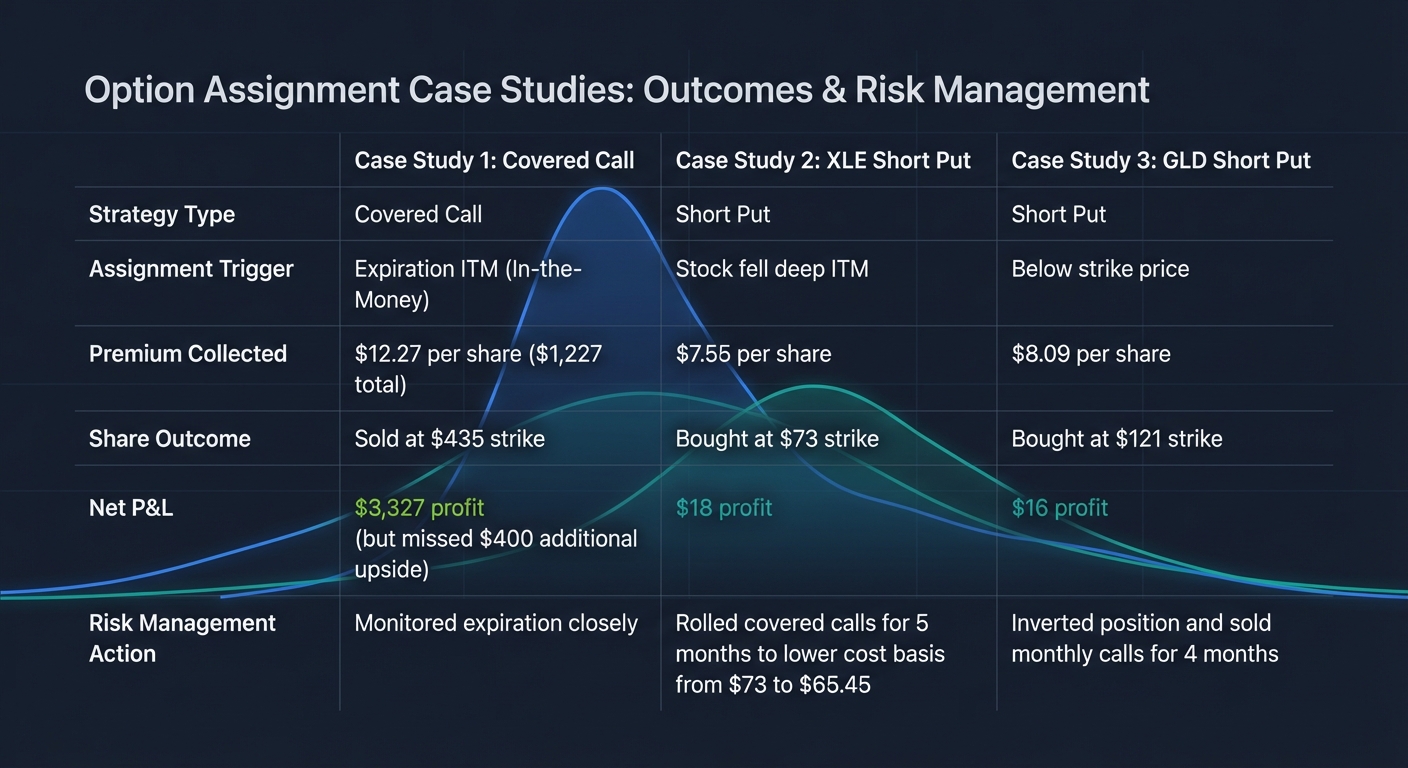

Option Assignment Case Studies Comparison: Outcomes and Risk Management Strategies

Comparing Assignment Scenarios

The case studies highlight how assignment outcomes vary depending on the strategy and market conditions. Here's a breakdown:

| Case Study | Strategy Type | Trigger | Premium Collected | Share Outcome | Net P&L | Risk Management Action |

|---|---|---|---|---|---|---|

| 1 | Covered Call | Expiration ITM | Premium retained | Sold at strike | Profit from premium + capital gains | Monitored expiration closely |

| 2 (XLE) | Short Put | Stock fell deep ITM | $7.55 | Bought at $73 | $18 | Rolled covered calls for 5 months to lower cost basis |

| 3 (GLD) | Short Put | Below strike price | $8.09 | Bought at $121 | $16 | Inverted position and sold monthly calls for 4 months |

In the XLE example, Kirk Du Plessis adjusted the position over five months, using covered calls to reduce the cost basis from $73 to $65.45. This approach prevented a potential $1,300 loss, ending with a slight profit when closing at $65.63. Similarly, the GLD trade turned an unrealized $748 loss into a $16 gain by selling monthly calls over four months. Both cases emphasize how disciplined adjustments can turn challenging assignments into profitable outcomes.

Final Thoughts

The case studies underscore that assignment is not inherently a setback but a part of options trading that can be managed effectively. Proper position sizing is critical to ensure your account can handle assignments without triggering margin calls. For short put assignments, selling covered calls can help reduce the break-even point.

"If you have enough patience and fortitude to stick with it and reduce the cost basis... you can turn it all the way back around."

- Kirk Du Plessis, Founder, Option Alpha

Understanding assignment mechanics is essential for managing your positions effectively. For instance, to avoid pin risk - the uncertainty of weekend assignment when a stock closes near your strike - close spreads before the market closes on expiration Friday. Tools like ThetaEdge offer assignment probability metrics and portfolio Greeks tracking, providing valuable insights to help you decide whether to roll, close, or hold positions through expiration.

FAQs

Will my option be automatically exercised at expiration?

Your option will automatically be exercised at expiration if it’s in-the-money by at least $0.01, unless you file a “Do Not Exercise” request with your broker before 3:00 PM (EST) on expiration day. It's a good idea to verify the exact deadlines and processes with your brokerage.

Why can I get assigned early on a short call before a dividend?

American-style options come with a unique feature: they can be exercised at any point before expiration. This opens the door to early assignment on a short call, especially when specific conditions align.

One key scenario to watch for is around ex-dividend dates. If your short call is in-the-money, the holder might choose to exercise it early to capture the dividend payout. Additionally, corporate actions can also prompt early exercises, creating another layer of risk.

When trading options near dividend events, it's crucial to stay alert to these possibilities. Early assignment can impact your strategy, so factor this risk into your decision-making process.

How much cash or margin do I need to handle assignment safely?

When managing assignment, it's crucial to have the resources to handle the obligations tied to your options contracts. Make sure you have enough cash or margin available to buy or sell 100 shares per contract at the strike price. Beyond that, keep additional funds on hand to meet any margin requirements. This extra cushion helps you avoid margin calls, which can occur if the stock price moves unfavorably against your position.