Portfolio Greeks and Covered Calls

Portfolio Greeks expose covered-call risks and income—use delta, theta, vega, and gamma to manage exposure and premium.

Portfolio Greeks give you a complete view of your portfolio's risk and income potential by analyzing key metrics like Delta, Theta, and Vega across all positions. For covered call strategies, this means understanding how your stock exposure, time decay, and volatility risks interact.

Key Takeaways:

- Delta: Measures market exposure. Selling calls reduces your stock's Delta, balancing risk and income.

- Theta: Tracks daily income from time decay. Covered calls benefit from positive Theta.

- Vega: Indicates volatility risk. Rising volatility can hurt short calls.

Covered calls balance premium income with capped upside. Tools like ThetaEdge simplify tracking Greeks, helping you monitor risks and optimize your strategy effectively.

Portfolio Greeks Guide for Covered Call Strategies

How Greeks Affect Covered Call Positions

Delta, Theta, Vega, and Gamma each play a role in shaping the performance of a covered call. Understanding how these factors interact helps you make informed decisions about strike prices, expiration dates, and overall risk management.

Delta: Stock Exposure and Call Offsets

Delta measures how sensitive your position is to stock price changes. Owning 100 shares gives you a Delta of +100. Selling a call with a Delta of -0.40 reduces your net Delta to +60, shifting your stance from fully bullish to moderately bullish. This adjustment offers limited downside protection while capping your maximum profit at the strike price plus the premium you collect.

Choosing the right strike price depends on your market outlook. Out-of-the-money (OTM) strikes provide smaller premiums but allow for capital gains up to the strike price. In-the-money (ITM) strikes, on the other hand, offer higher premiums and some downside protection but leave little room for price appreciation. Many investors choose a strike price that aligns with their target exit level for the stock.

"This horizontal line that represents potential loss can be elevated closer to the zero line by instituting appropriate exit strategies, selecting the best strike prices, factoring in market tone and equity technicals." - Alan Ellman, President, The Blue Collar Investor

Once you've adjusted your directional exposure with Delta, Theta takes center stage as it governs the income potential from time decay.

Theta: Time Decay and Premium Income

Theta reflects how much an option's value erodes daily due to time decay. For covered call writers, this works to your advantage. As the call option loses value over time, you keep the premium as profit, assuming the stock remains below the strike price.

Options with 20–45 days to expiration (DTE) are often ideal for capturing Theta. The BXM index, which tracks a hypothetical buy-write strategy on the S&P 500, has shown long-term returns comparable to the S&P 500 but with lower volatility. To strike a balance, many traders sell calls at 45 DTE and either close or roll them around 21 DTE to avoid the sharp Gamma effects that occur in the final week.

Vega and Gamma: Volatility and Delta Changes

Volatility adds another layer of complexity to covered calls, influencing both risks and opportunities.

Vega measures how a 1% change in implied volatility (IV) impacts the option's price. Selling covered calls creates a short Vega position, meaning rising IV increases the cost of buying back the call, which can hurt your profitability. To mitigate this, selling calls when IV is high allows you to benefit from an "IV crush" when volatility decreases.

Gamma, on the other hand, tracks how quickly Delta changes as the stock price moves. Covered calls are short Gamma trades, meaning your Delta shifts more dramatically during rapid price swings. This effect is most pronounced for at-the-money (ATM) options nearing expiration.

"Gamma risk is the danger associated with being Short Gamma (typically from selling options). Because Gamma is the rate of change of Delta, being short Gamma means that if the stock moves sharply against you, your negative Delta exposure will accelerate rapidly." - QuantStrategy.io Team

To manage Gamma risk in volatile markets, many traders prefer OTM strikes. These have lower Gamma, which helps keep Delta more stable and preserves profit potential even when stock prices fluctuate.

Each of these Greek factors contributes to a broader portfolio strategy, tying into the risk management tools and techniques discussed in later sections.

sbb-itb-a9ac3c2

Calculating Portfolio-Level Greeks

Understanding the Greeks at the portfolio level helps you uncover hidden risks and make smarter adjustments to your covered call strategies. By combining the metrics from individual positions, you create a broader view of your portfolio's risk profile, allowing for more informed decisions.

Net Delta for Portfolio Balance

Net delta represents how your portfolio reacts to a 1% market move, calculated by summing up the deltas of all your positions. For example, if you hold 100 shares of a stock (delta of +100) and sell a call option with a delta of -0.35, your net delta becomes +65. To better understand the dollar risk, multiply each position's delta by the stock price.

Traders often aim for a net delta within a range of -0.3 to +0.3 to minimize directional risk. If your delta drifts too far, say to +80, you might rebalance by selling additional calls or purchasing protective puts.

"Net portfolio delta is the single most important aggregate Greek because directional moves are the biggest source of P&L swings." - AInvest Options Pilot Research

Total Theta for Income Estimates

Total theta reveals your portfolio's daily income from time decay. For instance, if your portfolio theta is +$11, this means you're earning $11 per day - assuming prices and volatility don’t change. Covered call writers typically maintain a positive theta since they collect premium. A negative theta, however, signals that losses from long positions are outweighing the income from short calls. Keeping an eye on this metric ensures your strategy remains aligned with your goals.

Vega and Sector Diversification

Volatility risk is another key factor to consider when managing your portfolio. Portfolio vega measures how much your portfolio's value changes for every one-percentage-point shift in implied volatility. Covered call sellers generally have negative vega, meaning a spike in volatility could erase weeks of premium income.

Even if you sell calls across various stocks, true diversification may still elude you during market turbulence. As one analysis pointed out:

"Selling premium on 8 different underlyings in a low-vol environment feels diversified. But when VIX spikes, all of those positions lose money simultaneously. You're not diversified against volatility events."

To manage this, consider spreading your positions across different sectors and regularly monitoring your total vega to better prepare for volatility-driven risks.

Managing Risk with Portfolio Greeks

Once you've aggregated your position Greeks, the real challenge begins: actively managing risk and planning for potential market scenarios. Portfolio Greeks give you a big-picture view, but staying on top of them requires consistent monitoring and timely adjustments. Markets are unpredictable, and what seems balanced today could quickly tilt into a risky position tomorrow.

Daily Delta Monitoring and Adjustments

Keeping an eye on your portfolio's net delta every day is crucial because directional market moves can heavily impact your profits and losses (P&L). For instance, you might start with a neutral delta close to zero, but if it drifts to +80, your portfolio suddenly faces significant downside risk. Even a diversified strategy like covered calls can unintentionally expose you to concentrated directional risk if a specific sector starts trending.

"Individual position Greeks tell you about individual risk. Portfolio Greeks tell you whether your entire book is about to get wrecked by a single market move." - AInvest Options Pilot Research

When your delta strays too far from your target, you can rebalance using tools like protective puts, additional calls, or by closing overly bullish positions. It's also important to use dollar-weighted delta for accuracy. For example, a +50 delta on a $500 stock carries much more risk than the same delta on a $25 stock.

In addition to delta, keeping tabs on theta is equally important to ensure your income goals stay on track.

Tracking Theta Decay for Income Targets

Theta represents the daily income your portfolio earns from time decay. If your portfolio's theta dips below your income targets or even turns negative, you may need to make adjustments. Selling calls with 30-45 days to expiration (DTE) and rolling positions around 21 DTE can help maintain your income flow.

But managing Greeks isn't just about day-to-day tweaks. You also need to prepare for unexpected market events.

Scenario Analysis: Market Events and Responses

Portfolio Greeks are invaluable for stress-testing your portfolio against potential market shocks. For example, a 10-point spike in the VIX can cause negative vega positions to lose value rapidly, wiping out weeks' worth of theta income in a single day. Similarly, a 3% to 5% market move can significantly amplify your delta exposure, especially if your portfolio has high negative gamma.

Run stress tests for scenarios like a 5% market drop or a sharp increase in implied volatility (IV). Remember, during periods of market stress, stock correlations often rise toward 1.0. This means that even if your portfolio seems diversified, it might behave like a single directional trade under extreme conditions.

To navigate these shifts, consider rolling calls to higher strikes or adding protective puts to manage delta and vega risks during volatile periods. Additionally, pay close attention to gamma near expiration; even small price movements can cause large swings in delta, requiring quick adjustments.

Using Portfolio Greeks with ThetaEdge

ThetaEdge simplifies the challenge of managing portfolio Greeks, particularly for covered call strategies. Tracking Greeks manually can be both tedious and prone to mistakes. By linking with over 80 brokerages - including Schwab, Fidelity, Interactive Brokers, and Robinhood - ThetaEdge consolidates your holdings and instantly calculates key portfolio-level Greeks like delta, gamma, theta, and vega.

ThetaEdge simplifies the challenge of managing portfolio Greeks, particularly for covered call strategies. Tracking Greeks manually can be both tedious and prone to mistakes. By linking with over 80 brokerages - including Schwab, Fidelity, Interactive Brokers, and Robinhood - ThetaEdge consolidates your holdings and instantly calculates key portfolio-level Greeks like delta, gamma, theta, and vega.

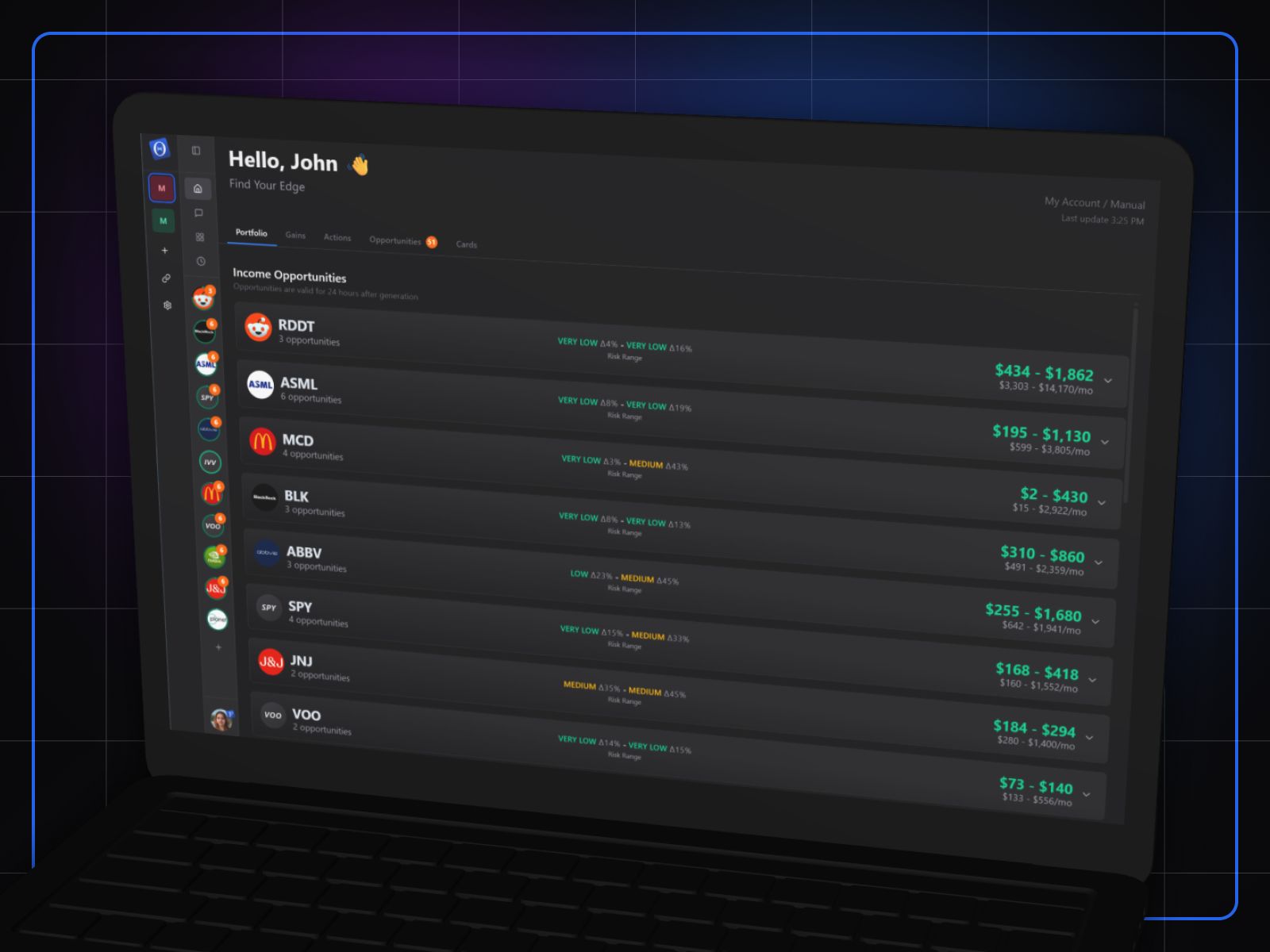

Portfolio Greeks Dashboard

The dashboard provides a clear view of your portfolio's key metrics, including net delta and total theta across all positions. It highlights your net delta and theta income, ensuring you have an accurate snapshot of your portfolio's performance. Additionally, it monitors Greeks, volume, open interest, and price momentum during times of peak liquidity. If your net delta drifts far from your target or your total theta falls below your income objectives, the dashboard flags these deviations, enabling you to address them promptly. This tool acts as a foundation for more detailed analysis using Thetix AI.

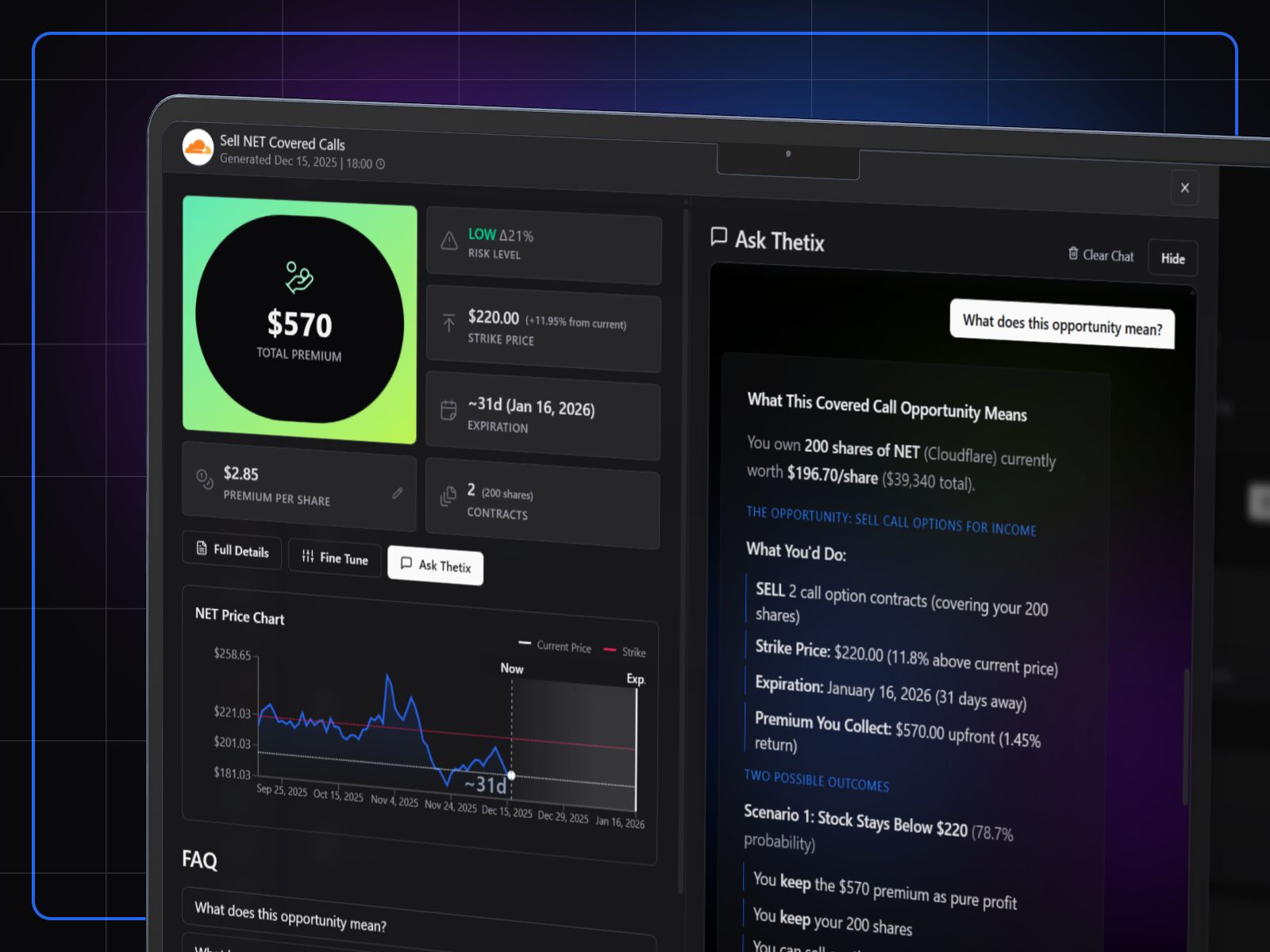

Opportunity Analysis and Thetix AI

ThetaEdge's analysis engine evaluates countless covered call setups, filtering them based on your specific risk preferences. For instance, a conservative investor might focus on setups with an assignment risk near 15%. The Thetix AI assistant provides clarity by explaining the trade-offs of various choices, answering questions about specific Greeks, and running "what-if" scenarios to show how market changes could impact your overall exposure. As ThetaEdge emphasizes:

"All analysis is presented as trade-offs to evaluate, never as instructions to follow. ThetaEdge surfaces what's happening in your portfolio. You decide what to do about it."

Income Tracking and Position Management

ThetaEdge offers real-time profit and loss tracking, factoring in theta decay. It alerts you when positions reach preset profit targets, typically around 35% of the maximum premium. Additionally, it provides automated roll signals with detailed credit and debit analysis when risks escalate. This ongoing monitoring ensures your covered call strategy remains aligned with both your income goals and risk tolerance.

Conclusion

Applying these principles allows portfolio Greeks to elevate covered call investing into a data-informed approach. By keeping an eye on net delta, you can avoid unintended directional risks, while tracking total theta offers insight into daily income potential. Meanwhile, monitoring vega and gamma helps you anticipate volatility shifts. Since 1986, covered call strategies have produced returns similar to buy-and-hold investments but with about two-thirds of the volatility.

The real hurdle is calculating Greeks across a variety of positions, strike prices, and expiration dates. Doing this manually is not only time-consuming but also prone to errors, especially for investors juggling multiple holdings across different platforms.

This is where ThetaEdge simplifies the process. The platform connects to over 80 brokerages through read-only access, instantly calculating portfolio-level Greeks and converting complex data into practical, actionable insights. So far, it has analyzed more than $300 million in assets, with an average portfolio size of $350,000, helping investors generate $6.3 million in premiums.

"More people want to make their own destiny, and ThetaEdge empowers them to do it with the same tools the elite have always used".

That’s how Maxim Khailo, Founder & CEO, describes the platform’s mission. It provides clarity about your portfolio’s performance - while leaving the decisions in your hands.

Keep a close watch on your net delta, rebalance when theta dips into negative territory, and stress-test your Greeks regularly. With the right tools, managing portfolio Greeks becomes a manageable and effective part of your strategy. Before you begin, review a covered call checklist to ensure your trades are properly sized and risk-managed.

FAQs

What’s a good net delta target for a covered call portfolio?

A net delta target of +20 to +30 is often considered a solid benchmark for a covered call portfolio. This range strikes a balance between generating income and keeping directional risk at a level that works for most investors.

When should I roll a covered call to manage gamma risk?

When gamma exposure gets too intense or market signals suggest a big move in the underlying asset, it might be time to roll your covered call. Adjusting the strike price or expiration date can help smooth out dramatic shifts in delta, keeping your position more in line with your desired balance of risk and reward.

How can I reduce vega risk when implied volatility spikes?

To manage vega risk during periods of rising implied volatility, you might want to tweak your approach. Adjusting strike prices, choosing shorter expiration dates, or rolling your calls are practical ways to handle the situation. These strategies can reduce the influence of volatility on your covered call positions, helping you maintain a balance between risk and potential reward.