Protective Puts vs. Collars: Dividend Stock Strategies

Protect downside without selling: choose protective puts for unlimited upside or collars to cut costs while capping gains.

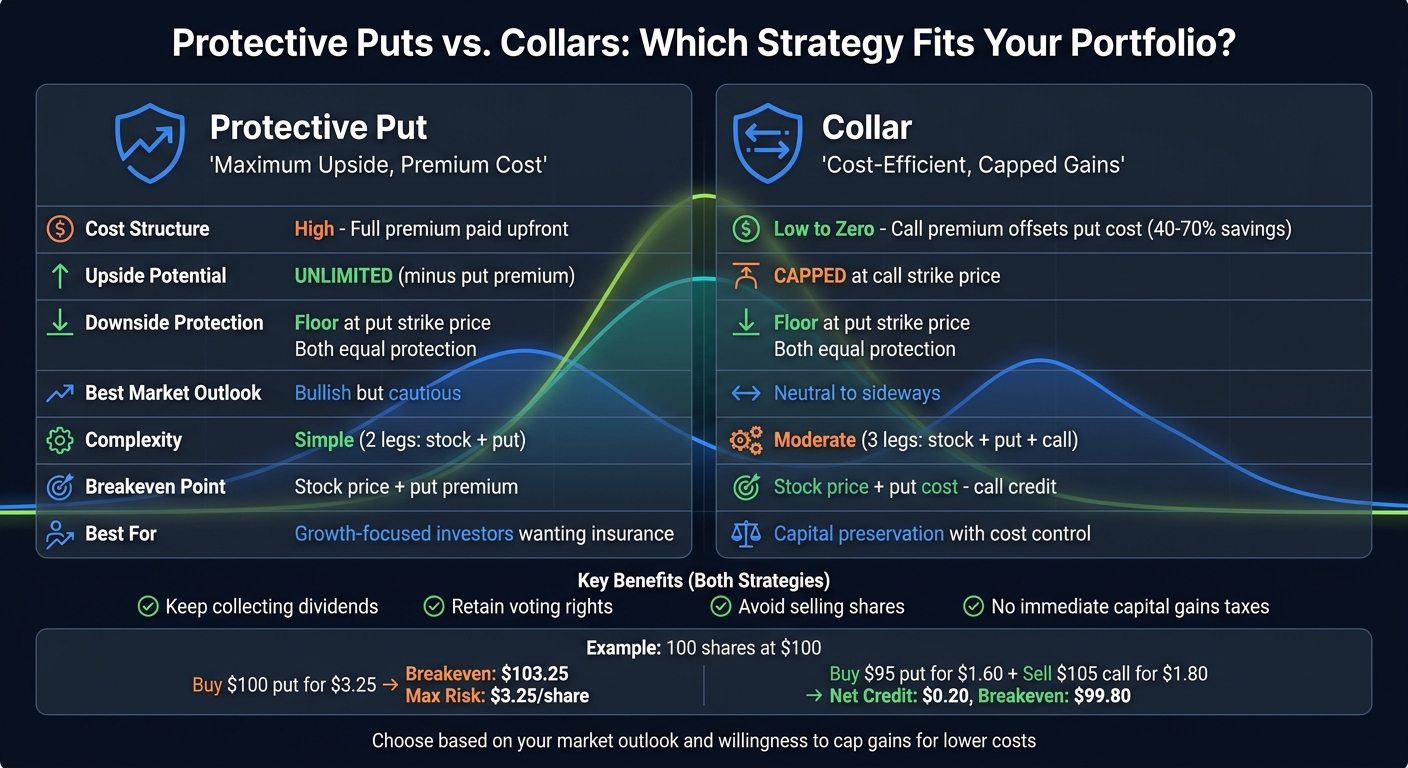

Protecting your dividend stock portfolio doesn’t have to mean sacrificing growth or taking on unnecessary costs. Two common options strategies - protective puts and collars - offer ways to limit downside risk while keeping your shares intact. Here’s the key difference:

- Protective Puts: You pay a premium to set a minimum price for your stock, ensuring downside protection while leaving your upside potential open. Best for investors expecting growth but wanting insurance.

- Collars: You combine a protective put with a covered call, reducing or even eliminating the cost of protection. However, your upside is capped at the call’s strike price. Ideal for those prioritizing cost control over unlimited gains.

Both strategies let you continue collecting dividends and avoid selling your shares outright. Your choice depends on your goals, market outlook, and risk tolerance.

Quick Comparison

| Factor | Protective Put | Collar |

|---|---|---|

| Cost | High (full premium paid) | Low to zero (call offsets put cost) |

| Upside Potential | Unlimited (minus put cost) | Capped at call strike price |

| Downside Protection | Floor at put strike | Floor at put strike |

| Market View | Bullish but cautious | Neutral to sideways |

| Complexity | Simple (2 legs) | Moderate (3 legs) |

This article explains how each strategy works, their pros and cons, and when to use them effectively.

Protective Puts vs Collars: Side-by-Side Strategy Comparison for Dividend Investors

How Protective Puts Work

This section explains the mechanics behind protective puts, a strategy often used by dividend stock investors to safeguard their investments.

What Is a Protective Put?

A protective put acts like an insurance policy for your dividend-paying stocks. Here's how it works: you own shares of a dividend stock and purchase a put option for those same shares. This strategy, sometimes called a "married put", grants you the right to sell your stock at a predetermined strike price, regardless of how much the market price might decline. By doing this, you establish a minimum exit price while continuing to enjoy dividends and maintain voting rights.

The beauty of this approach is that it doesn't limit your potential gains. If the stock price rises, you can still benefit fully from the appreciation. The only trade-off is the cost of the put premium. Investors can tailor their level of protection by choosing between at-the-money (ATM) puts for maximum coverage or out-of-the-money (OTM) puts, which lower the premium cost but allow for a small predefined loss (e.g., 5–10%) before the protection kicks in.

Next, let's look at how premiums and strike price selection affect your floor price and breakeven point.

Cost and Breakeven Points

The cost of a protective put is influenced by three key factors: how close the strike price is to the current market price, the time left until the option's expiration, and the stock's implied volatility. For instance, puts with strike prices 3–5% below the current market price are more expensive than those struck 10–15% lower.

Your effective floor price is calculated by subtracting the premium paid from the put's strike price. Meanwhile, the breakeven point is your stock's purchase price plus the premium. For example, if you purchase a $170 put for $4.50 per share, your effective floor price becomes $165.50, and the stock must rise by at least $4.50 for you to break even.

For long-term dividend investors, the cost of this protection can add up over time. Rolling short-term puts in volatile markets can consume anywhere from 25% to 74% of the position's value annually. Alternatively, longer-term options like LEAPS may offer more economical protection, costing around 13% annually on average.

"The put gives you the right to sell, not the obligation. You control the timing through expiration. That control is what the premium buys." - Chris Butler, Founder, projectoption

Pros and Cons of Protective Puts

Once you understand the costs, it’s important to weigh the advantages and disadvantages of using protective puts.

Advantages:

- Limits downside risk to the strike price while allowing for unlimited upside potential.

- Lets you retain full ownership of your shares, so you continue to collect dividends and keep voting rights.

- Unlike stop-loss orders, which can trigger during short-term market dips, protective puts give you the flexibility to decide if and when to sell, helping you navigate temporary volatility.

Disadvantages:

- Premium costs can be high, especially in volatile markets, potentially reducing overall returns if the stock price remains stable.

- Overusing protective puts or selecting strike prices too close to the current stock price can trigger IRS "constructive sale" rules, which might lead to unexpected taxable events.

- This strategy is often better suited for short-term protection during high-risk periods, such as earnings announcements or macroeconomic uncertainty, rather than as a permanent hedge.

sbb-itb-a9ac3c2

How Collar Strategies Work

Collar strategies provide a practical way to manage risk while keeping costs in check, offering a middle ground compared to the often expensive protective put.

What Is a Collar?

A collar strategy combines three elements: owning dividend-paying stock, buying an out-of-the-money protective put, and selling an out-of-the-money covered call. Together, these components create a defined range of possible outcomes by limiting both potential losses and gains. The put acts as a safety net if the stock price falls, while the call generates income that offsets much (or all) of the cost of the put. Importantly, you maintain ownership of your shares, allowing you to continue receiving dividends and retain voting rights.

Reducing Cost with Call Premiums

The premium from selling the call significantly reduces the overall cost of the hedge - often by 40% to 70% compared to buying a protective put on its own. In some cases, the collar can be structured so that the call premium fully covers the cost of the put, creating a zero-cost hedge. Alternatively, you can sell a call that generates more premium than the put costs, resulting in a net-credit collar. While this approach puts money in your pocket upfront, it typically comes with trade-offs, such as a lower cap on potential gains or reduced downside protection.

Once the cost efficiency is clear, it’s important to weigh the benefits and limitations of using collars.

Pros and Cons of Collars

Collars are attractive because they provide downside protection with little to no upfront cost and help stabilize portfolio performance by setting clear boundaries for potential outcomes.

That said, there are trade-offs. Your upside is capped at the call’s strike price, which means you could miss out on significant gains if the stock rallies sharply. Early assignment is another risk - this can happen just before the ex-dividend date or during expiration week, forcing you to sell your shares prematurely.

Taxes are another consideration. If the collar is structured too tightly - such as setting both the put and call strikes within 5% of the stock’s current price - the IRS may treat it as a "constructive sale", triggering immediate capital gains taxes even though you still hold the shares. To avoid this, many investors opt for a wider range, typically using a 10% floor and a 10–15% ceiling as safer limits.

Protective Puts vs. Collars: Side-by-Side Comparison

Let’s break down the key differences between protective puts and collars to help you decide which approach aligns better with your goals for protecting dividend stocks.

Cost and Structure Differences

With protective puts, you pay the full premium upfront, which increases your cost basis. On the other hand, collars offset hedging costs by using call premiums, sometimes even creating a net credit that reduces your breakeven price. For instance, if you purchase 100 shares of XYZ at $100 and buy a 100-strike put for $3.25, your breakeven rises to $103.25, and your maximum risk is $3.25 per share. However, if you sell a covered call alongside the put, you can cut hedging costs significantly - often by 40% to 70% compared to just buying the put. Using the same XYZ example, buying 100 shares at $100, selling a 105 call for $1.80, and buying a 95 put for $1.60 results in a $0.20 net credit, lowering your breakeven to $99.80.

The trade-off? Protective puts allow unlimited upside (minus the cost of the put), while collars cap your gains at the call strike price.

| Factor | Protective Put | Collar |

|---|---|---|

| Net Cost | High | Low/Zero |

| Upside Potential | Unlimited (minus put cost) | Capped at call strike |

| Downside Protection | Floor at put strike | Floor at put strike |

| Breakeven | Stock price + put premium | Stock price + put cost - call credit |

| Complexity | Simple (2 legs) | Moderate (3 legs) |

Now that the cost and structure differences are clear, let’s compare how these strategies handle risk and reward in different scenarios.

Risk and Reward Comparison

Both strategies limit your downside to the put strike price, but how they handle profits is where they diverge. With a protective put, your maximum loss equals the put premium plus any drop between your purchase price and the put strike. However, your profit potential remains uncapped as the stock rises, aside from the cost of the put.

Collars, by contrast, define a specific range of outcomes. Your profit is capped at the call strike, adjusted for any net credit or debit, while your maximum loss is the difference between your stock price and the put strike, also adjusted for the net options cost. For example, with the April 2024 Apple collar at $176.55, a $185 call and $170 put would yield a $9,415 profit if AAPL rose to $187. If it fell to $165, your profit would drop to $7,915 - sacrificing $285 in potential upside but saving $415 in a downturn.

While these are static comparisons, the market environment often dictates which strategy performs better.

Performance in Different Market Scenarios

In strong rallies, protective puts let you capture all the upside (minus the premium). With collars, any gains beyond the call strike are forfeited once that level is reached.

In flat or mildly declining markets, protective puts can be costly since you’re paying for insurance that might not be needed. Collars shine here, especially in zero-cost or net-credit setups, as the call premium offsets the put cost. This allows you to keep collecting dividends while maintaining a stable position.

In sharp declines, both strategies provide a safety net at the put strike. However, collars are more cost-efficient, often delivering protection for much less - or even at a credit. It’s also worth noting that protective puts avoid the risk of early assignment, which can be a concern with collars, particularly around ex-dividend dates when you might be forced to sell your shares prematurely.

"A sideways or slightly declining market is sometimes the best scenario for protective collar options." – SoFi

Your choice should depend on your market outlook. Protective puts are ideal if you’re optimistic about the stock but want disaster protection. Collars, on the other hand, are better suited for those focused on minimizing costs and preserving capital.

Which Strategy Fits Your Goals?

Deciding between protective puts and collars comes down to your investment goals. Are you looking for unlimited upside with some insurance, or are you focused on preserving capital while keeping costs low? Your market outlook and how much you're willing to spend on protection will shape your choice.

When to Use Protective Puts

Protective puts are ideal if you're optimistic about growth but want to guard against potential losses. By paying the full premium, you secure unlimited upside while capping your downside risk. For instance, if you own a concentrated position in a reliable dividend-paying stock with strong growth potential, this strategy allows you to stay fully invested without limiting your profit. It’s a straightforward way to balance confidence in your stock with a safety net.

When to Use Collars

Collars are a better fit if protecting your capital is your top priority and you're okay with sacrificing some upside to reduce costs. This approach works best in markets that are neutral or slightly declining. By selling a covered call, you offset the cost of the protective put, sometimes even achieving a zero-cost setup or earning a small credit.

"The collar wins when your primary goal is protection and you are willing to trade upside for lower cost." – AInvest Options Pilot

Collars are particularly useful for managing large, appreciated positions. For example, if you bought Apple shares at $90 and they now trade at $176, a collar can lock in your gains while minimizing tax implications. Wider strike spacing (at least 10%) can help avoid triggering constructive sale rules.

Strategy Comparison Table

| Factor | Protective Put | Collar |

|---|---|---|

| Best For | Strongly bullish investors seeking unlimited upside | Investors focused on capital preservation |

| Upfront Cost | High (full premium is paid) | Low to zero (covered call offsets the put cost) |

| Upside Potential | Unlimited (minus the cost of the put) | Capped at the call strike |

| Market View | Bullish but cautious | Neutral to sideways |

| Complexity | Simple (single transaction) | Moderate (involves two transactions) |

| Tax Considerations | Straightforward | May trigger constructive sale rules |

Using ThetaEdge for Protective Strategies

Evaluating protective strategies on your own can be a daunting task. You’d need to sift through complex option chains, calculate breakeven points, and fine-tune strategies to fit your portfolio. ThetaEdge simplifies this process by analyzing your holdings and identifying protective opportunities that align with your investments. It even takes things a step further by allowing you to integrate your brokerage account for real-time assessments.

How ThetaEdge Analyzes Protective Strategies

What sets ThetaEdge apart is its focus on your positions, not just generic stock tickers. For instance, if you own 156 shares of a dividend stock with a $90 cost basis, ThetaEdge tailors its analysis to your exact situation. It calculates protective put and collar strategies, presenting key details like strike prices, expiration dates, premiums, assignment probabilities, and breakeven points - all in one clear view.

The platform’s Thetix AI tool makes it even easier to explore hedging scenarios. You can ask straightforward questions like, "What’s the cost difference between a protective put and a collar for my Apple position?" Using live market data and your actual cost basis, the tool provides accurate numbers and clear explanations.

ThetaEdge doesn’t stop at analysis - it keeps an eye on your portfolio over time. It monitors real-time profit and loss, sending alerts when you hit profit targets or when rolling a position becomes cost-effective.

By combining thorough analysis with secure brokerage integration, ThetaEdge ensures your strategies are both precise and ready for action.

Brokerage Integration

ThetaEdge doesn’t just analyze your portfolio; it connects directly to over 80 brokerages, including major names like Schwab, Fidelity, Interactive Brokers, and Robinhood. This connection means you don’t have to manually input your positions or transfer accounts. Using 256-bit encryption and OAuth 2.0 protocols, the platform keeps your brokerage credentials secure while ensuring that no trades are executed without your consent.

Once your brokerage is linked, ThetaEdge goes to work, filtering and ranking protective opportunities based on your holdings, cost basis, and share quantities. To date, the platform has analyzed over $300 million in assets, with an average portfolio size of $350,000 per member. Collectively, users have earned $6.3 million in premiums by leveraging its insights. Prefer not to link your brokerage? You can manually input your positions and still receive tailored analysis.

Conclusion

Deciding between protective puts and collars comes down to a choice between unlimited upside and managing costs. Protective puts let you enjoy unlimited gains while securing a downside floor, but they require paying the full premium upfront. Collars, on the other hand, cut that cost by 40% to 70% by selling a call option to offset the put's expense - though this limits your potential gains to the call's strike price.

Both options allow you to retain dividend-paying shares and avoid triggering capital gains taxes, which is a major benefit compared to selling the stock outright. Protective puts are ideal if you're optimistic about the stock but want a safety net for downturns. Collars, meanwhile, are better suited for investors focused on preserving capital and willing to trade some upside for reduced costs.

Market conditions heavily influence these strategies. When implied volatility is high, call premiums increase, making zero-cost collars easier to set up. In contrast, during periods of low volatility, protective puts may require a higher upfront cost, making collars a more budget-friendly choice.

Comparing strike prices, breakevens, and risk scenarios manually can feel overwhelming. That’s where ThetaEdge steps in. It simplifies the process by analyzing your actual holdings and offering side-by-side comparisons of protective puts and collars. With risk metrics and integration across more than 80 brokerages, ThetaEdge helps streamline decisions for your portfolio.

The key is to match your strategy to your goals, risk tolerance, and market conditions. Tools like ThetaEdge provide the insights you need to protect your dividend stocks while continuing to reap the benefits of dividends.

FAQs

How do I pick the right put strike and expiration for my dividend stock?

When deciding on a put strike and expiration, it's important to weigh factors like your risk appetite, market expectations, and investment objectives. A strike price closer to the stock's current value provides stronger protection but comes with a higher cost. On the other hand, a lower strike is more affordable but offers less downside coverage.

For expiration dates, shorter durations (1-3 months) are typically better for short-term hedging needs, while longer durations (6-12 months) offer extended protection, albeit at a higher premium. Make sure your choices align with the stock's volatility and any significant upcoming events that could impact its price.

Will a collar get my shares called away before the ex-dividend date?

Yes, your shares could be called away before the ex-dividend date when using a collar strategy. This occurs if the stock price rises above the strike price of the call option you sold. In such cases, the buyer of the call option has the right to exercise it at any time before expiration, including before the ex-dividend date.

Can protective puts or collars trigger a taxable “constructive sale”?

Protective puts and collars are generally not considered a taxable "constructive sale." This is because they are viewed as hedging strategies rather than outright sales of the underlying stock. Their purpose is to manage risk while maintaining ownership of the stock.