Rolling Returns vs. Cumulative Returns

Compare cumulative and rolling returns: total growth vs consistency, formulas, examples, pros/cons, and when to use each.

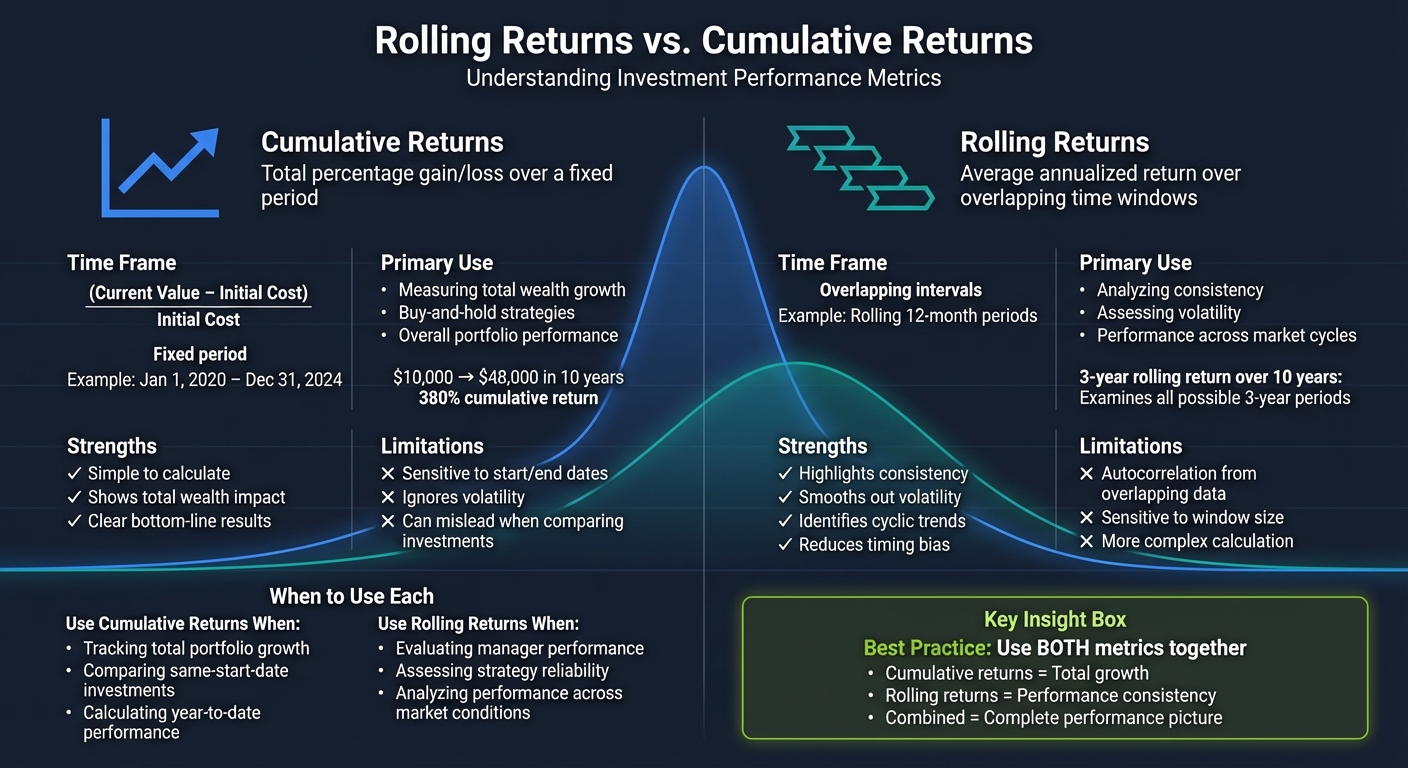

Rolling returns and cumulative returns are two ways to measure investment performance, each serving a different purpose. Cumulative returns show the total percentage growth or decline of an investment over a fixed period, answering the question: How much has my investment grown overall? Rolling returns, on the other hand, analyze performance across overlapping time frames, offering insights into consistency and trends.

Key Takeaways:

- Cumulative Returns: Ideal for evaluating total portfolio growth between two dates. Example: If a $10,000 investment grows to $48,000 in 10 years, the cumulative return is 380%.

- Rolling Returns: Useful for assessing how returns vary over time, showing performance across different market conditions. Example: A 3-year rolling return for a 10-year investment examines all possible 3-year periods.

Quick Comparison:

| Feature | Cumulative Returns | Rolling Returns |

|---|---|---|

| Definition | Total percentage gain/loss over a period | Average annualized return over overlapping windows |

| Time Frame | Fixed (e.g., Jan 1, 2020 – Dec 31, 2024) | Overlapping intervals (e.g., rolling 12 months) |

| Primary Use | Measuring total wealth growth | Analyzing consistency and volatility |

| Potential Bias | Sensitive to start/end dates | Affected by overlapping data points |

By combining both metrics, you can evaluate not only how much your investments have grown but also how reliably they perform over time.

Rolling Returns vs Cumulative Returns: Key Differences and Use Cases

What Are Cumulative Returns?

Definition and Formula

Cumulative return measures the total percentage change in an investment's value over a specific period, reflecting overall growth without adjusting for annualized effects. It’s a straightforward way to see how much an investment has grown from start to finish.

The most precise way to calculate cumulative returns is through geometric chaining, which factors in compounding over multiple periods. The formula looks like this: Rc = (1 + R1)(1 + R2)...(1 + Rn) - 1, where each "R" is the return for a specific time period. For a single period, the simpler formula is: (Current Value - Initial Cost) / Initial Cost.

If you're calculating cumulative returns for assets like dividend-paying stocks or interest-bearing bonds, it’s crucial to use the adjusted closing price. This ensures that dividends, payouts, and stock splits are included in your calculation.

Example Calculation

Imagine you bought a stock for $40 and later sold it for $100. The cumulative return would be 150%, calculated as ($100 - $40) / $40.

For a more dramatic example, consider Amazon. From its IPO in 1997 to 2020, the company achieved a cumulative return exceeding 100,000% - a staggering figure.

The importance of geometric chaining becomes clear when looking at the SPY (S&P 500 ETF) from January 3, 2007, to December 7, 2020. Using the geometric method, SPY’s cumulative return was 245.16%. By comparison, simply adding up the returns (arithmetic chaining) would have resulted in only 153% - a significant underestimation.

When to Use Cumulative Returns

Cumulative returns are most useful for analyzing overall portfolio growth between two specific points in time. They’re particularly effective for evaluating buy-and-hold strategies, as they show the total percentage gain an investor would achieve by holding an asset for the entire period.

This metric is also helpful for comparing investments, but only when the investments share the same start date or are evaluated over identical timeframes. Otherwise, older funds may appear to perform better simply because they’ve had more time to grow.

When reviewing cumulative returns in mutual fund or ETF "mountain graphs", check whether dividends and capital gains have been reinvested. These factors can significantly influence total returns. Additionally, don’t overlook expense ratios, management fees, and taxes, as these costs will reduce your actual cumulative return.

Next, we’ll look at rolling returns and how they provide an additional layer of insight alongside cumulative figures.

sbb-itb-a9ac3c2

What Are Rolling Returns?

Definition and Calculation Process

Rolling returns measure the annualized average returns over overlapping time periods. Unlike cumulative returns, which provide a single performance figure between two dates, rolling returns show how returns shift over time. For instance, a 5-year rolling return for 2015 would span January 1, 2011, to December 31, 2015. The next year's 5-year rolling return would cover January 1, 2012, to December 31, 2016.

"Rolling returns, also known as 'rolling period returns,' provide a smoothed annualized average of returns over multiple periods, ending with a specified year." - Investopedia

These returns are calculated using geometric compounding, which allows comparisons between windows of different lengths, such as a 6-month rolling period versus a 12-month one.

Example Calculation

To compute a 3-year rolling return over a 10-year span, start with the return for the first 36 months. Then, shift the starting point forward by one month and calculate the return for the next 36-month block. This process continues until the end of the period.

For example, in December 2025, analysts evaluated Apple Inc. (AAPL) using a 6-month rolling return approach. They applied a 126-period window with an annualization scale of 252 periods, covering data from January 1, 2020, to January 1, 2024. This method highlighted trends in 6-month annualized returns, making it easier to identify stock momentum and shifts in market behavior.

A similar rolling calculation is often used in corporate finance. For instance, Trailing 12-Month (TTM) revenue smooths seasonal fluctuations. GE’s Q1 2020 TTM revenue was adjusted from full-year figures to account for these seasonal patterns.

These examples demonstrate how rolling returns can uncover trends across various time frames.

When to Use Rolling Returns

Rolling returns are particularly helpful for evaluating how strategies perform under different market conditions. They can show if an investment consistently outperforms a benchmark or if success is limited to specific periods - something cumulative returns might not reveal. Shorter rolling periods, like 3 to 6 months, can highlight recent momentum or market shifts. Longer windows, such as 3 to 5 years, help smooth out short-term fluctuations and provide a clearer picture of long-term performance trends.

Additionally, the Global Investment Performance Standards (GIPS) often require rolling return disclosures because they offer insights into how investments behave across complete market cycles.

"Rolling returns show consistency, while trailing returns show cumulative performance. Investors who want to understand how an investment performs over varying conditions often prefer rolling returns for a more balanced and dynamic view." - SmartAsset

A high degree of variation across rolling windows suggests that performance depends heavily on timing, while low variability indicates steadier, more predictable results - qualities that appeal to investors focused on long-term growth.

Key Differences Between Rolling and Cumulative Returns

Comparison Table: Rolling vs. Cumulative Returns

When it comes to measuring investment performance, cumulative returns and rolling returns provide two distinct perspectives. Cumulative returns offer a single, straightforward figure - the total percentage gain or loss over a specific period. Rolling returns, on the other hand, break performance into overlapping time windows, offering insights into how returns fluctuate under varying market conditions.

| Feature | Cumulative Returns | Rolling Returns |

|---|---|---|

| Definition | Total percentage gain or loss over a defined period | Average annualized return over overlapping time windows |

| Calculation | (Price<sub>end</sub> / Price<sub>start</sub>) - 1 or through geometric chaining of periodic returns | Geometric mean of returns within each window, annualized |

| Time Frame | Fixed (e.g., Jan. 1, 2020, to Dec. 31, 2024) | Overlapping intervals (e.g., rolling 12-month periods) |

| Primary Use | Evaluating total wealth accumulation or "bottom line" results | Analyzing consistency, volatility, and performance across different market cycles |

| Potential Bias | Sensitive to specific start and end dates | Autocorrelation introduced by overlapping windows |

These distinctions highlight not only how the metrics are calculated but also how they influence portfolio analysis and decision-making.

How These Differences Affect Portfolio Analysis

The choice between cumulative and rolling returns can significantly impact how you interpret investment performance. Cumulative returns are ideal for assessing total outcomes, such as tracking the growth of your portfolio since inception or calculating year-to-date performance. However, this metric is heavily influenced by the specific start and end dates you choose, which can skew the results.

Rolling returns, by contrast, address this timing sensitivity by showing a range of potential outcomes based on different entry points. For example, in 2020, analysts examining the SPY (S&P 500 ETF) noted a stark contrast between cumulative return calculations: a 153% return using simple arithmetic chaining versus 245.16% when applying the correct geometric compounding method. Rolling returns eliminate such discrepancies by consistently using annualized geometric calculations across all windows.

When evaluating fund managers or strategies, rolling returns provide critical insights into performance consistency. A fund with high cumulative returns but erratic rolling returns may owe its success to favorable timing rather than sustained skill. Conversely, a fund with stable rolling returns demonstrates more dependable performance, regardless of market entry points. This makes rolling returns a valuable tool for assessing reliability over time.

Pros and Cons of Each Metric

Pros and Cons Table

When analyzing portfolios, both cumulative and rolling returns offer distinct insights. Knowing their strengths and weaknesses ensures you use the right metric for the right situation. Here's a breakdown of how they stack up:

| Metric | Pros | Cons | Best Use Case |

|---|---|---|---|

| Cumulative Returns | Simple to calculate; reflects total wealth impact; accounts for reinvestment effects. | Can mislead when comparing investments; ignores time and volatility; heavily influenced by start and end dates. | Tracking the total growth of an initial investment. |

| Rolling Returns | Highlights consistency; smooths out volatility; identifies cyclic trends. | Prone to autocorrelation bias; sensitive to window size; may lag in spotting turning points. | Assessing manager performance and strategy reliability over time. |

A Closer Look at Cumulative and Rolling Returns

Cumulative returns provide a straightforward way to measure total growth. They’re ideal for tracking how much your portfolio has grown since you started investing. However, this simplicity can be a double-edged sword. Since cumulative returns are tied to specific start and end dates, they can paint an overly rosy or bleak picture depending on market conditions during those periods. Volatility and timing are often overlooked, which makes comparisons tricky. As Investopedia explains:

"Cumulative returns often grow over time, making older stocks and funds appear more impressive. It follows that the cumulative return is not a good way to compare investments unless they launched at the same time".

Rolling returns, on the other hand, dig deeper into performance patterns. By smoothing out short-term fluctuations, they help reveal whether strong results stem from genuine skill or just favorable timing. This makes them especially valuable for assessing how a strategy holds up across different market cycles. But rolling returns aren't without flaws. Overlapping data points introduce autocorrelation, which can skew statistical analysis. Additionally, the choice of window size - whether it’s one year, three years, or longer - can significantly affect the conclusions you draw.

What This Means for Investors

Each metric serves a specific purpose. Cumulative returns are best when you need to calculate total performance over a fixed period, such as year-to-date gains or growth since inception. They answer the fundamental question: How much did I make?

Rolling returns, meanwhile, are indispensable for evaluating consistency and reliability. If you're analyzing strategies like covered calls or cash-secured puts, rolling returns can show whether the approach delivers steady results across various market conditions. To get a fuller picture, pair rolling returns with other metrics like the Sharpe Ratio or drawdown analysis.

In short, cumulative returns provide the big picture of overall growth, while rolling returns focus on performance stability. Together, they give you the tools to assess both the results and the dependability of your investments. Next, we'll explore how combining these metrics can take performance analysis to the next level.

Using Rolling and Cumulative Returns Together

How to Combine Both Metrics

Cumulative returns give you the big picture of an investment's overall performance, while rolling returns break it down into smaller, overlapping time periods to show consistency. Cumulative returns reflect the total percentage gain or loss of an investment over a set time, accounting for reinvestments, fees, and taxes. Rolling returns, on the other hand, smooth out performance over multiple periods, helping you spot patterns like frequent highs or lows.

By using both, you avoid being misled by a single-period snapshot. For example, an investment might show a steady 9% annualized return over a decade, but rolling returns could reveal dramatic swings - years with 35% gains and others with 17% losses. Similarly, while Amazon's cumulative return exceeded 100,000% from its 1997 IPO to 2020, this figure hides a period during 2000–2001 when the stock lost over 90% of its value. This highlights how cumulative returns can mask volatility that rolling returns bring to light.

Cumulative returns are ideal for gauging total wealth growth and the impact of external costs. Rolling returns, meanwhile, help identify periods of strong or weak performance and neutralize the effects of one-off market events, such as temporary demand spikes or cash flow changes. Together, these metrics provide a fuller picture, which is particularly useful in areas like options trading, where both profitability and consistency matter.

Application in Options Trading

In options strategies like covered calls, combining cumulative and rolling returns is essential. Cumulative returns track total premium income earned and reductions in cost basis over time, giving a broad view of profitability. Rolling returns, on the other hand, measure how consistently that income is generated across different market conditions - whether in bullish, bearish, or flat markets.

Rolling returns also help identify risks that might be hidden in cumulative data. For instance, during periods of high volatility or "gamma risk", short-term price spikes could lead to unwanted call assignments. This is especially relevant for covered calls. Research suggests the most effective rolls occur 14–21 days before expiration, when delta reaches 0.60–0.70. By monitoring rolling returns, you can see whether a strategy's success stems from consistent performance or a lucky streak during favorable market conditions.

When rolling, count each net credit as a reduction in cost basis and aim to roll short calls after achieving 50% of maximum profit. This approach locks in gains and supports long-term performance. Avoid rolling for a net debit unless you're defending against an unwanted assignment, as this increases the cost basis and can hurt cumulative returns.

ThetaEdge Tools for Performance Analysis

ThetaEdge offers tools that make tracking both cumulative and rolling returns straightforward. Its income tracking dashboard gives investors a clear view of total income (cumulative) alongside monthly cash flow consistency (rolling), helping you analyze performance across different options portfolios.

The platform includes features like historical profit-and-loss tracking, year-based filtering, and portfolio-level visualizations, making it easier to spot trends in your options income. With additional tools for portfolio Greeks and roll strategies, ThetaEdge helps you evaluate both overall profitability and the dependability of strategies like covered calls, cash-secured puts, and multi-leg trades. It connects to over 80 brokerages via read-only access, ensuring your performance data stays up-to-date without executing trades or offering investment advice.

Conclusion

Understanding rolling and cumulative returns provides a well-rounded view of your portfolio's performance. While cumulative returns highlight the total wealth generated over time, rolling returns focus on the consistency and reliability of those gains under varying market conditions. As SmartAsset explains, "Using both together gives investors a clearer understanding of performance trends and helps identify funds that can weather changing market conditions".

Relying solely on cumulative returns can be deceptive, as strong performance during a single period might mask underlying volatility. Rolling returns, on the other hand, reveal these fluctuations, helping you identify whether performance stems from consistent strategy or favorable timing.

For options traders, both metrics are equally valuable. Cumulative returns measure the overall success of a strategy, while rolling returns demonstrate whether that success is steady over time. This distinction is crucial in separating strategies that thrive on market timing from those built on enduring resilience.

ThetaEdge simplifies this process by offering tools that combine income tracking with visualizations, making it easier to analyze both long-term gains and short-term consistency. With connectivity to over 80 brokerages through read-only access, ThetaEdge keeps your data updated while allowing you to retain full control over your trades. This seamless integration ensures you can monitor both your strategy's profitability and its reliability.

FAQs

Should I annualize cumulative returns?

When deciding whether to annualize cumulative returns, it all comes down to what you're trying to achieve. Cumulative returns reveal the total growth over a specific period, but they don't factor in how long it took to achieve that growth. Annualizing, on the other hand, translates those returns into a yearly rate, which makes comparing performance across different timeframes much simpler.

That said, annualized returns come with a caveat: they assume consistent growth year over year. If the returns are volatile, this assumption may not accurately reflect the actual performance. So, annualizing is most useful when you're comparing different periods or assessing performance on a yearly basis.

What rolling-return window should I use?

A 12-month rolling-return window is a popular method for assessing portfolio performance over an entire year. This approach highlights trends in both consistency and cyclicality, providing useful insights for analyzing how a portfolio behaves over time.

Do rolling returns include dividends and fees?

Rolling returns typically focus on price changes and do not account for dividends or fees unless explicitly mentioned. They measure the average annualized return over a set period, offering insights into price performance rather than total returns.