Strike Price Selection: Complete Guide for Covered Calls

Choose the right covered call strike: compare ITM, ATM, OTM trade-offs and use delta, IV, and expiration to align income, risk, and growth.

Covered calls are a popular way to generate income from stocks you already own. The key to success? Choosing the right strike price. Here’s what you need to know:

- What is a covered call? You sell a call option on 100 shares you own, collect a premium, and limit your upside if the stock rises above the strike price.

- Why does the strike price matter? It affects your income, risk of assignment, and potential stock gains.

- Three strike price options:

- In-the-money (ITM): Highest premiums, best downside protection, but high chance of assignment.

- At-the-money (ATM): Balanced premiums and assignment risk; ideal for steady stocks.

- Out-of-the-money (OTM): Lower premiums but allows stock appreciation; best for bullish outlooks.

- Factors to consider:

- Implied volatility (IV): Higher IV = higher premiums but more price swings.

- Time to expiration: 30–45 days is optimal for faster premium decay.

- Delta: Guides assignment probability (e.g., 0.30 delta = ~30% chance of assignment).

Pro Tip: Always ensure the strike price plus premium exceeds your stock’s cost basis to avoid losses. Tools like ThetaEdge can simplify the process by providing real-time analytics and recommendations.

Covered calls offer steady income but require careful planning. Choose a strike price that aligns with your goals - whether it’s maximizing income, protecting your stock, or balancing both.

Factors That Affect Strike Price Selection

When deciding on a strike price, three key variables come into play: implied volatility, time to expiration, and strike distance. These elements directly influence the premium you earn, the risk of assignment, and your overall returns. Understanding how these factors work together allows you to tailor your covered call strategy to your investment goals. Let’s break them down.

Implied Volatility and Option Premiums

Implied volatility (IV) reflects the market’s expectations for future price movements. When uncertainty spikes - due to events like earnings reports, Federal Reserve announcements, or geopolitical developments - IV rises, and option premiums increase.

"Higher Implied Volatility leads directly to higher option premiums. For a covered call writer, this means that periods of market fear are often the most profitable times to sell calls." - StrikePrice.app

During high IV periods, covered call writers can benefit by selecting strike prices further out-of-the-money (OTM) and still earning premiums comparable to at-the-money (ATM) strikes in calmer markets. This approach reduces assignment risk while taking advantage of elevated premiums.

However, higher IV also signals greater expected price swings, which raises the chance of the stock reaching the strike price. For stocks with strong upward momentum, writing in-the-money (ITM) or ATM calls during high IV periods increases the likelihood of losing your shares.

Timing is key. Selling covered calls just before known events - like earnings announcements, FDA rulings, or economic data releases - can help you capture higher premiums. Be sure to calculate your breakeven price (strike price plus premium received) to understand the total exit price if your shares are assigned.

Time to Expiration and Theta Decay

Theta measures how an option’s value erodes as it approaches expiration. This decay speeds up significantly in the final 30 to 45 days of an option’s life. For covered call writers, this rapid time decay can be a major advantage.

"As an option seller, this accelerated decay is your best friend. You want the option you sold to expire worthless, and Theta is the engine that gets you there." - John Clarke, StrikePrice.app

Options with around 45 days to expiration often hit the sweet spot. They offer the steepest time decay while still providing enough value to generate meaningful premiums. Longer expirations (90 days to six months) yield higher premiums and allow for OTM strikes, but they also increase the chances of the stock moving beyond the strike price, which raises assignment risk.

For example, a study of the Russell 2000 index (2003–2018) showed that selling monthly calls 2% OTM outperformed the index, but this advantage disappeared with two-month expirations. Additionally, the Cboe S&P 500 BuyWrite Index captured about 61% of the S&P 500’s gains during bull markets from 1986 to 2023, highlighting the trade-off between income and upside potential in covered call strategies.

Your expiration choice depends on how actively you want to manage your positions. Short-term expirations (60 days or less) require frequent adjustments, while intermediate-term expirations (90 days to six months) are better suited for a more hands-off approach. For dividend-paying stocks, keep in mind that ITM calls are more likely to be assigned early, especially around the ex-dividend date.

Strike Price Distance from Current Stock Price

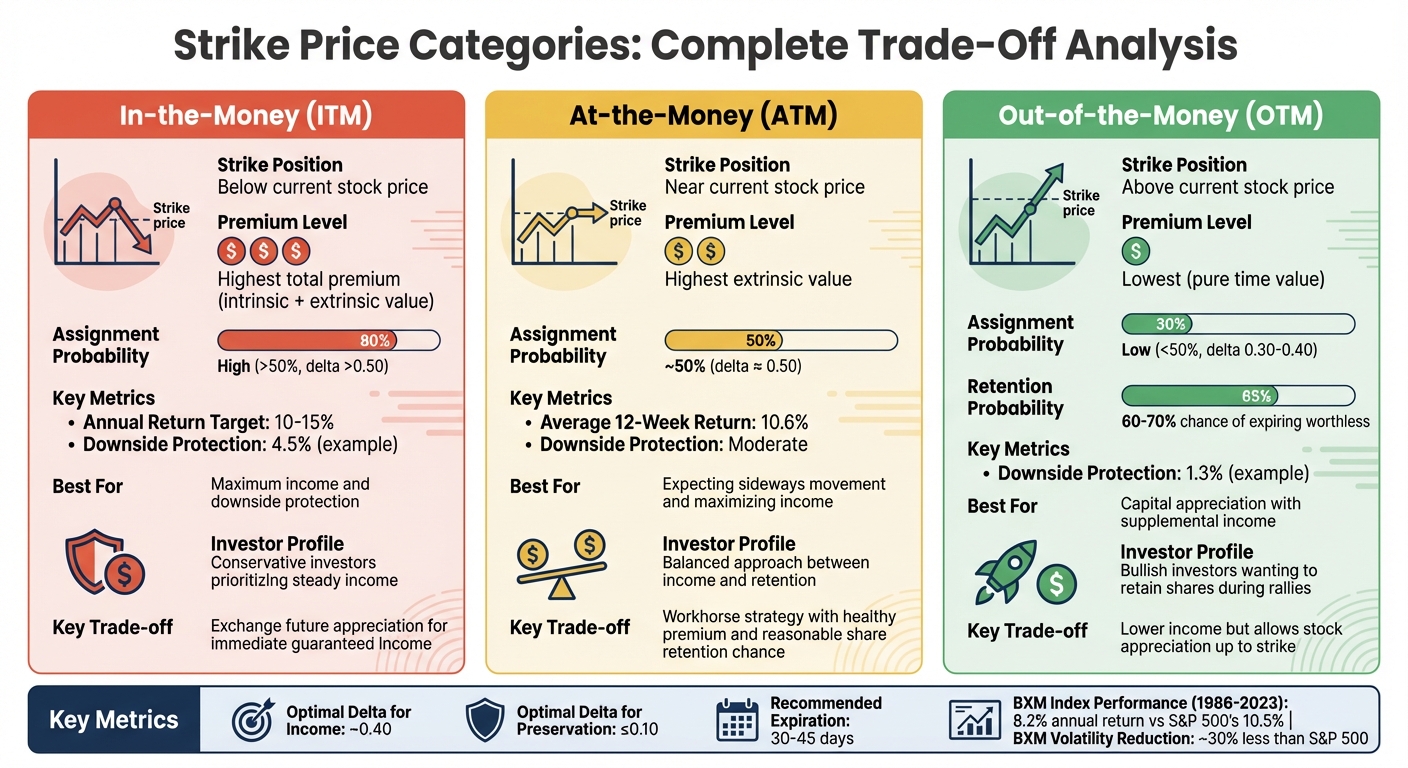

The relationship between the strike price and the current stock price is another critical factor. It determines the premium level and assignment risk and typically falls into three categories: in-the-money (ITM), at-the-money (ATM), and out-of-the-money (OTM).

- In-the-Money (ITM): Strike prices below the current stock price offer the highest premiums and the most downside protection but come with a high risk of assignment. With deltas approaching 1.0, ITM calls mostly capture intrinsic value rather than time value.

- At-the-Money (ATM): Strike prices near the stock price maximize the extrinsic value in the premium and have about a 50% chance of assignment. Research shows ATM strategies often deliver the highest average returns, with one study reporting 10.6% over 12-week periods, compared to 5.6% for OTM and 6.4% for ITM strategies.

"An ATM strike is the workhorse of many covered call strategies. It aims to provide a healthy premium while still offering a reasonable chance for the stock to remain yours at expiration." - StrikePrice.app

- Out-of-the-Money (OTM): Strike prices above the current stock price generate lower premiums but allow you to benefit from stock appreciation up to the strike price. Many investors target options with deltas between 0.30 and 0.40, which have a 60% to 70% likelihood of expiring worthless. This strikes a balance between income generation and retaining your shares.

| Strike Category | Strike vs. Stock Price | Premium Level | Assignment Risk | Best For |

|---|---|---|---|---|

| In-the-Money (ITM) | Below current price | Highest | High | Maximum income and downside protection |

| At-the-Money (ATM) | Near current price | Moderate-High | ~50% | Balancing income with share retention |

| Out-of-the-Money (OTM) | Above current price | Lowest | Low | Capital appreciation with supplemental income |

To estimate assignment probability, use delta as a guide - a 0.30 delta call has roughly a 30% chance of assignment, while a 0.70 delta call has about a 70% chance. If your stock nears the strike price and you want to avoid assignment, consider "rolling" the position by buying back the current call and selling a new one at a later date or higher strike.

3 Strike Price Categories and Their Trade-Offs

Covered Call Strike Price Comparison: ITM vs ATM vs OTM

Let’s break down the trade-offs of the three main strike price categories: in-the-money (ITM), at-the-money (ATM), and out-of-the-money (OTM). Your choice here directly impacts your income potential, the likelihood of assignment, and your ability to benefit from stock price increases.

At-the-Money Strikes

ATM strikes match the current stock price, making them a popular choice for generating high extrinsic premiums. These premiums decay as expiration approaches, and with a delta near 0.50, they carry about a 50% assignment probability.

"An ATM strike is the workhorse of many covered call strategies. It aims to provide a healthy premium while still offering a reasonable chance for the stock to remain yours at expiration." – Strike Price

ATM strategies tend to deliver solid returns, especially when you expect the stock to trade sideways. They strike a balance between collecting premiums and retaining shares. However, there’s a catch: your stock’s upside potential is capped at the strike price. During volatile periods, ATM premiums can spike - for example, SPY ATM calls surged to $781 during a U.S. election, compared to just $218–$246 in calmer times. While higher premiums are appealing, they come with increased assignment risk.

Out-of-the-Money Strikes

OTM strikes are set above the current stock price, resulting in lower premiums but reduced assignment risk. These options are purely made up of time value and typically have deltas below 0.50. Many traders prefer OTM strikes with deltas between 0.30 and 0.40, which means there’s a 60% to 70% chance they’ll expire worthless.

This approach works well when you’re optimistic about your stock’s future. You can still enjoy price appreciation up to the strike level while pocketing the premium as a bonus. The Cboe S&P 500 BuyWrite Index (BXM), which uses slightly OTM calls, is a great example. From 1986 to 2023, the BXM delivered an annual return of 8.2% compared to the S&P 500’s 10.5%. However, the BXM showed about 30% less volatility and a smaller maximum decline - 35.8% versus the S&P 500’s 51% drop.

OTM strikes are ideal when you’re bullish on your stock and want to retain long-term holdings while enjoying some added income.

In-the-Money Strikes

ITM strikes are set below the current stock price, offering the highest total premiums by combining intrinsic and extrinsic value. These strikes provide strong downside protection but come with high assignment risk due to deltas above 0.50. Conservative investors often favor ITM strikes, aiming for steady returns (around 10% to 15% annually) with less volatility.

"The primary trade-off is clear: you are exchanging potential future stock appreciation for immediate, guaranteed income." – John Clarke

For instance, if a stock is trading at $92.79, an ITM strike at $90 might yield a $4.20 premium, providing about 4.5% downside protection. If the stock drops to $88.59, you’d break even instead of taking a loss. However, any gains above the $90 strike price go to the option buyer.

ITM strikes are best suited for investors who prioritize income and protection over growth. They’re particularly useful when you’re neutral to slightly bearish on a stock you own but aren’t ready to sell.

| Strike Category | Strike vs. Stock Price | Premium Amount | Assignment Probability | Best Used When |

|---|---|---|---|---|

| At-the-Money (ATM) | Near current price | Highest extrinsic value | ~50% (delta ≈ 0.50) | Expecting sideways movement and aiming for maximum income |

| Out-of-the-Money (OTM) | Above current price | Lowest | Low (<50%, delta 0.30–0.40) | Being bullish and wanting to retain shares during rallies |

| In-the-Money (ITM) | Below current price | Highest total premium | High (>50%, delta >0.50) | Prioritizing downside protection and seeking consistent income |

Matching Strike Price to Your Investment Goals

Let’s dive deeper into how to select the right strike price to align with your investment goals. Whether you’re aiming for higher income, protecting your stock position, or finding a balance between the two, your strike price choice plays a key role.

Maximizing Premium Income

If your main goal is to generate cash flow, focus on strikes that deliver higher premiums while managing the risk of assignment. A delta of around 0.40 is often the sweet spot for income-focused investors. This delta captures a good chunk of the option’s time value while offering a reasonable chance of retaining your shares.

"If you are aiming for explosive cash flow, lean towards the 0.4 Delta strike, accepting the higher risk of assignment." – Ben T., OraniaTech

Here’s an example: In October 2025, an investor holding AT&T (T) shares at $29.57 sold a $30 strike call with a 0.426 delta. This strategy yielded an impressive annualized return of 37.3%. While there was a 42.6% chance of assignment, the premium earned made it an attractive choice for those prioritizing cash flow.

At-the-money (ATM) strikes are particularly effective at maximizing time value. Historical data shows that over 12-week periods, ATM covered call strategies delivered average returns of 10.6%, compared to 6.4% for in-the-money (ITM) calls and 5.6% for out-of-the-money (OTM) calls. Keep in mind, though, ATM strategies come with a 50% assignment probability, so you need to be prepared to sell your shares at the strike price.

Protecting Your Stock Position

When your priority shifts to safeguarding your stock holdings, ITM strikes offer the best buffer against potential price drops. The premium collected reduces your effective cost basis, providing a cushion against losses.

To calculate your downside protection, subtract the premium from the stock’s current price. For instance, if Apple is trading at $92.79, selling a $90 ITM strike call might offer 4.5% downside protection, compared to only 1.3% for a $96 OTM strike. Historical data from the 1987 market crash also highlights that ITM covered calls outperformed simply holding the stock, with returns 3.0% to 6.6% higher.

Here’s a real-world scenario: In November 2025, an investor holding Apple shares at $200 (with a $180 cost basis) sold a $195 ITM call expiring in 30 days for an $8 premium ($800 total). If the stock price remained above $195, the investor’s total profit reached $2,300, including capital gains. If the stock dropped to $194, they kept the shares and the $800 premium, effectively lowering their cost basis to $172.

"The core trade-off with an in-the-money covered call is simple: you sacrifice the potential for large gains in exchange for a higher probability of profit and greater downside protection from the premium collected." – John Clarke, StrikePrice.app

For those who want to keep their stocks with minimal risk, OTM strikes with low deltas are a safer bet. For example, in October 2025, an investor holding Johnson & Johnson shares at $160 sold a $170 strike call with a 0.05 delta, earning a $0.40 premium. This approach had only a 5% chance of assignment, allowing the investor to collect extra income while retaining the stock for long-term growth.

Using Delta and Probability Metrics

Delta is a powerful tool for aligning your strike price with your investment goals. It acts as both a probability indicator and a measure of how much the option price will move for every $1 change in the stock.

"Delta is more than just a Greek letter - it's a probability engine that helps you choose the right strike price based on your goals." – Ben T., Investment Strategist, OraniaTech

Here’s how delta can guide your strategy:

| Strategy Goal | Target Delta | Assignment Risk | Primary Benefit |

|---|---|---|---|

| Maximize Income | ~0.40 | Moderate (40–45%) | High time value premiums |

| Balanced Income | ~0.50 (ATM) | Moderate (~50%) | Maximum time value |

| Preserve Stock | ≤0.10 | Very Low | Minimal assignment risk |

Pairing your delta choice with a 30 to 45-day expiration window can further enhance results. This timeframe leverages theta decay, which accelerates in the final 30 days, allowing you to collect premiums while the option’s time value erodes.

For even more accuracy, tools like Fidelity’s probability calculator can help estimate the likelihood of a stock trading above, below, or between specific price targets by the expiration date. By integrating these metrics, you can fine-tune your strike price strategy to fit seamlessly into your broader investment plan.

sbb-itb-a9ac3c2

Using ThetaEdge for Strike Price Analysis

ThetaEdge makes choosing strike prices easier by using advanced analytics. It empowers self-directed investors to analyze covered call opportunities with precision, turning theoretical strategies into actionable steps. This tool builds on the risk/reward concepts introduced earlier, offering a seamless way to evaluate trades.

Risk/Reward Metrics and Assignment Probabilities

With ThetaEdge, you get Risk/Reward Opportunity Cards for every potential covered call trade. These cards break down the risk profiles, profit potential, and assignment probabilities for each strike price. Instead of manually calculating whether a $95 or $100 strike price is better, the platform instantly shows the likelihood of assignment and the premium you’d earn. If a position moves against you, ThetaEdge suggests optimal rolling strategies, complete with detailed credit and debit analysis. Everything is presented in clear dollar amounts and probability metrics, making decision-making straightforward.

Portfolio Greeks and Multi-Broker Integration

ThetaEdge goes beyond individual trades by integrating your entire portfolio for real-time analysis. Managing multiple covered call positions requires a clear understanding of your overall exposure. ThetaEdge calculates portfolio-wide Greeks - Delta, Gamma, Theta, and Vega - so you can see how factors like time decay (Theta) or directional exposure (Delta) align with your goals. For example, you can quickly determine if your daily Theta matches your income targets or if your Delta exposure could lead to trouble during market shifts.

The platform connects securely to over 80 brokerages with read-only access, consolidating all your positions into one unified dashboard.

"Running the hedge fund, I created institutional tools that could analyze thousands of scenarios in real-time... ThetaEdge empowers [self-directed investors] to do it with the same tools the elite have always used." – Maxim Khailo, Founder & CEO, ThetaEdge

Thetix AI for Personalized Recommendations

Thetix AI takes personalization to the next level by offering tailored strike recommendations based on your portfolio. You can ask simple questions like, “Which strike offers optimal income with minimal assignment risk?” and receive Thetix Cards with clear, actionable advice.

The AI also sends daily action plans directly to your inbox, highlighting the best covered call opportunities, suggesting strikes with specific expiration dates, and notifying you when a position needs attention. For instance, when deciding between a 0.30 Delta and a 0.40 Delta strike, Thetix stress-tests both options, showing how each would impact your portfolio's overall risk profile. By simplifying complex metrics into easy-to-understand insights, ThetaEdge ensures your decisions are well-informed and aligned with your strategy.

"With Thetix you can ask trading questions in plain language... It responds with clear, actionable cards so your decisions are always informed, confident, and under your control." – ThetaEdge

Currently in beta, ThetaEdge offers early users the chance to secure founder pricing for its full suite of tools and services.

Common Strike Price Selection Mistakes to Avoid

Even seasoned investors can make errors when picking strike prices for covered calls. Recognizing these pitfalls can help protect your portfolio and improve your returns. Here are some mistakes to steer clear of.

Ignoring Volatility Changes

Implied volatility (IV) measures the market's expectations of future price swings, and overlooking it can impact your profits. When IV is low, option premiums shrink because the market perceives less risk. This means you earn less for taking on the same obligation. Many investors mistakenly choose strike prices too close to the stock's current price during these low-volatility periods, which increases the likelihood of assignment.

On the other hand, higher IV allows you to select strike prices further out-of-the-money while still collecting solid premiums. This creates a larger margin of safety. To make informed decisions, check the IV rank or IV percentile, which compares current IV to its 52-week range. Selling covered calls becomes more attractive when the IV rank is above 50.

"Higher IV leads to higher extrinsic value, while lower IV results in lower extrinsic value." – Investopedia

Be cautious of a "volatility crush", which occurs when IV drops sharply after events like earnings announcements. In such cases, the extrinsic value of your option can plummet, even if the stock price remains steady. Avoid selling calls right before earnings unless you're prepared to handle sudden price movements. Also, ensure your strike price accounts for your cost basis to avoid unfavorable outcomes.

Forgetting Your Cost Basis

Another common mistake is setting a strike price that, combined with the premium, results in a realized loss. Always calculate the total exit price - strike price plus premium received - and confirm it exceeds your original purchase price. For instance, if you bought shares at $105 and sell a $100 strike call for a $2 premium, your total exit price is $102. This would leave you with a $3 per share loss if assigned.

"The total sale price of the stock is calculated by adding the strike price of the call to the premium received." – Fidelity

To avoid losses, ensure the exit price exceeds your cost basis. If you own shares with a very low cost basis and want to avoid selling, pick strike prices with a low chance of assignment. Have a plan to "buy to close" the option if the stock price nears the strike.

Not Planning for Rolling Positions

Strike price selection is just one part of the equation - managing the position is equally important. Many traders fail to plan for situations where the stock moves against their expectations. Rolling - closing your current position and opening a new one with a different strike or expiration - lets you adjust to market shifts and potentially earn more premium. Having a rolling strategy in place can help you avoid forced assignments or missed opportunities.

For example, if a stock is nearing your strike price and you want to hold onto your shares, you can "roll up and out." This involves buying back the current call and selling another at a higher strike with a later expiration. This approach not only provides more room for the stock to move but also allows you to collect additional premium.

Conclusion

Choosing the right strike price for covered calls is all about finding the balance between premium income, downside protection, and potential for growth. There’s no one-size-fits-all solution - your decision should align with your specific goals. For instance, if you’re focused on generating immediate cash flow and are okay with the possibility of selling your shares, in-the-money strikes offer higher premiums and a buffer against price drops. On the other hand, if your priority is holding onto your shares for long-term growth while earning some extra yield, out-of-the-money strikes with deltas between 0.30 and 0.40 provide a solid 60% to 70% chance of retaining your stock.

Timing also matters. Selling covered calls during periods of high implied volatility (IV) helps you capture higher premiums, compensating for the capped upside. And always ensure that the strike price, combined with the premium, exceeds your cost basis to avoid locking in a loss. For expiration dates, aiming for a 30–45 day window allows you to take advantage of faster time decay. Using delta metrics and accelerated theta decay can help fine-tune your strategy even further.

"The core trade-off is straightforward: you exchange potential large gains for a higher probability of profit and greater downside protection from the premium collected."

It’s also smart to plan ahead for situations where the stock price nears your strike. If you want to avoid assignment and keep your shares, decide in advance whether to buy back the call and roll it to a later expiration or higher strike.

ThetaEdge simplifies this process by providing the tools you need to make informed decisions. With features like multi-broker integration and Thetix AI for tailored recommendations, it offers self-directed investors professional-level insights while keeping you firmly in control. By sticking to these strategies and leveraging the right tools, you can ensure your covered call approach aligns with your financial objectives.

FAQs

How does implied volatility affect choosing strike prices for covered calls?

Implied volatility is a crucial factor when deciding on strike prices for covered calls, as it directly influences option premiums and the trade's risk-reward dynamics. When implied volatility is high, option premiums rise because the market expects larger price swings in the underlying stock. This allows investors to aim for higher strike prices, collecting more substantial premiums while reducing the chances of the stock being called away.

In contrast, low implied volatility leads to smaller premiums. In these situations, investors often select strike prices closer to the stock's current price to maximize income potential.

High implied volatility also increases the likelihood of significant price movements, meaning the stock could surpass the strike price. While this adds some risk, it also provides the opportunity for better premium income. On the flip side, lower volatility indicates a steadier market, making it easier to align strike prices with conservative income goals or risk management preferences. By understanding implied volatility, investors can better balance premium income with the risk of selling their stock at the strike price.

What role does delta play in predicting the likelihood of assignment for an option?

Delta is an important metric that helps gauge the likelihood of an option expiring in-the-money, which plays a direct role in the chances of assignment. A higher delta (closer to 1) means there's a stronger probability the option will be assigned, while a lower delta (closer to 0) reflects a smaller chance.

Grasping delta allows investors to evaluate the risks and possible results of their covered call strategies more effectively, ensuring these strategies align with their overall investment objectives.

How can I use ThetaEdge to improve my covered call strategy?

ThetaEdge offers advanced options analysis tools designed to align with your portfolio and investment goals. Whether you're looking to boost income or manage downside risk, the platform provides clear insights into risk/reward scenarios and delivers real-time market data to help shape your decisions.

For example, choosing strike prices just above the current stock price can increase premium income while still leaving room for potential capital gains. ThetaEdge also keeps an eye on market conditions and volatility in real time, enabling you to adjust your strategy as needed. With these tools, you can confidently strike a balance between generating income and managing risks in your covered call strategy.