Trailing Stops: Common Mistakes to Avoid

Avoid tight stops and emotional edits—use ATR/volatility-based trailing stops, automate exits, and pair with an initial hard stop.

Trailing stops are a powerful tool for locking in profits and managing risk, especially in options trading. However, many traders misuse them, leading to premature exits, emotional decisions, or poor outcomes. Here are the top mistakes to avoid and how to fix them:

- Setting Stops Too Tight: Stops placed too close to the current price often trigger unnecessarily due to normal market fluctuations. Use a volatility-based approach, such as a 2x ATR multiplier, to give trades room to develop.

- Manual Adjustments Driven by Emotions: Fear and greed can derail your strategy. Automate trailing stops to remove emotional interference and stick to your plan.

- Ignoring Market Volatility: Fixed-percentage stops fail in volatile markets. Adjust stops dynamically using ATR or market conditions to avoid premature exits.

- Overlooking Options-Specific Factors: Options involve complexities like time decay and delta sensitivity. Combine percentage trails with delta or time thresholds for better results.

- Skipping Initial Hard Stops: Trailing stops protect profits, but they don't limit initial losses. Always set a hard stop at the start of a trade to cap your risk.

Mistake 1: Setting Trailing Stops Too Tight

Using an options strategy planner to manage risk requires setting stops that can handle market fluctuations without cutting off potential gains. A common mistake is placing trailing stops too close to the price, leading to exits triggered by normal market movements. This issue is particularly problematic in options trading, where leverage and sensitivity to delta and implied volatility can magnify even small changes in the underlying asset. Such premature exits can force you out of a profitable position before it reaches your target.

"Tight stops get hit not because the trade idea was wrong but rather there was no breathing space for the trade to flourish."

While tight stops may seem like a way to minimize losses, they often result in frequent stop-outs, which can hurt the overall profitability of your strategy. For instance, using a 1x Average True Range (ATR) multiplier is generally considered too tight, often leading to premature exits.

How Tight Stops Impact Options Trading

The problem becomes even more pronounced in options trading due to the inherent volatility and leverage involved. Options are naturally more volatile than stocks, and setting a trailing stop too close assumes that the market won't retrace - a risky and often unrealistic assumption. Market pullbacks typically average around 6%, with some reaching as high as 8%, meaning tight stops are frequently triggered by routine volatility.

Delta sensitivity adds another layer of complexity. Even a minor move in the underlying asset can cause a disproportionately large change in the option's premium. As expiration nears, time decay (theta) further erodes the option's value, potentially triggering a tight stop even if the underlying asset remains relatively stable.

"The problem isn't your direction; it's your distance."

- Isabella Torres, Derivatives Analyst, FXNX

To avoid these issues, it's better to use a volatility-based approach for setting trailing stops.

Solution: Use ATR and Volatility-Based Adjustments

A more reliable approach involves using the Average True Range (ATR) of the underlying stock to calculate your trailing stop distance. ATR, typically measured over a 14-day period, reflects an asset's natural volatility. Since option prices are influenced by time decay and changes in implied volatility, it's best to calculate ATR using the underlying stock and then adjust the option's stop level accordingly.

For swing trading, a 2x ATR multiplier is often a balanced choice. It provides enough room for the trade to develop while still offering protection. Here's how it works for long positions:

Trailing Stop = Recent High - (ATR × Multiplier)

For example, if the stock's ATR is $2.50 and you're using a 2x multiplier, the trailing stop would be set $5.00 below the recent high.

| Multiplier | Trading Style | Trailing Distance | Pros | Cons |

|---|---|---|---|---|

| 1x ATR | Day trading, scalping | Tight | Limits loss per trade; quick exits | High stop-out rate; may miss reversals |

| 2x ATR | Swing trading | Moderate | Accommodates normal volatility | Potentially larger loss when triggered |

| 3x ATR | Position trading | Wide | Survives noise; captures big moves | Requires larger capital risk |

When implied volatility increases, consider widening your trailing stop to account for larger potential price swings. Conversely, during periods of low volatility, a tighter stop can help secure profits. Adjust your stop only when the underlying asset hits a new high, and avoid moving the stop to breakeven until your gains match your initial risk level.

sbb-itb-a9ac3c2

Mistake 2: Manually Adjusting Stops Based on Emotions

Even the most disciplined traders can fall into the trap of letting emotions dictate their decisions when adjusting trailing stops. This isn't just about making a poor choice - it’s about how stress impacts your brain. Watching a trade turn against you or seeing gains slip away can make emotional reactions overpower logical thinking.

"Algo Software allows you to build logic that will dynamically trail stops based on market conditions, rather than your emotions."

Why Emotional Adjustments Can Derail Your Plan

When fear or greed takes over, manual adjustments often pull you off course. For instance, if a trade comes close to hitting your target but reverses, it can trigger regret and frustration. This type of "what if" thinking often leads to impulsive decisions that deviate from your original strategy.

Consider this real-world example: In June 2024, a client of Power Trading Group was up $2,500, just $50 shy of his target. However, he was stopped out for only $200. The frustration of losing $2,300 in unrealized gains led to four revenge trades, ultimately costing him over $7,000 in a single hour.

Emotional adjustments also become more likely as your self-control wears down. A string of small losses can drain your ability to think rationally, leaving you more prone to impulsive decisions. Even success can be risky - winning streaks flood your brain with dopamine, which can cloud judgment and lead to overconfidence, prompting further manual interventions.

Sticking to your plan requires objectivity, and automating your stops is a key way to avoid emotional pitfalls.

Solution: Automate Trailing Stops

To counteract emotional interference, automation is your best ally. Automated trailing stops ensure decisions are based on objective market factors like price action, Average True Range (ATR), or delta changes, rather than fleeting emotions.

Platforms like ThetaEdge offer tools to activate trailing logic only after hitting a preset profit level. This prevents premature exits. For options traders, you can tie trailing stops to delta thresholds or a percentage of premium collected, keeping your stops aligned with the actual risk of your position.

To further safeguard your discipline, consider adding circuit breakers to your routine. For example, after two consecutive losses, take a mandatory 30-minute break. This pause gives you time to reset mentally before making another trade.

Mistake 3: Ignoring Volatility and Market Conditions

Overlooking market volatility can disrupt your trading strategy just as much as setting stops too tight or letting emotions take over. Many traders rely on fixed-percentage or dollar-based trailing stops - such as 2% or $500 - for all their trades. The problem? These static stops don’t account for the ever-changing nature of market volatility. In highly volatile markets, these stops can trigger too early, cutting off potential gains. On the flip side, in calmer markets, they might let too much profit slip away before activating.

How Volatility Impacts Trailing Stops

Option prices are influenced by complex factors like theta decay and implied volatility, making fixed-percentage stops unreliable. They often lead to premature exits.

"Fixed percentage stop losses ignore a critical reality: volatility changes across assets and over time."

Research by Snorrason and Yusupov highlights that trailing stops set between 15% and 20% performed better than buy-and-hold strategies during periods of high market volatility. The takeaway? Your stop distance needs to adapt to market conditions. When weekly volatility spikes to 150% above its average, standard stop settings often require wider adjustments or manual tweaks to remain effective.

Solution: Adjust Stops Dynamically

One effective way to account for market volatility is by using the Average True Range (ATR). ATR measures the average price range over a specified period (commonly 14 days), allowing stops to expand in turbulent markets and tighten during calmer times. For options, such as when executing a covered call strategy, base your ATR calculations on the underlying stock. For example, if the ATR is $2.00 and you use a 2x multiplier, your trailing stop would be set $4.00 below the most recent high.

Here’s a practical framework for adjusting stops based on market conditions:

| Market Volatility | ATR Multiplier | Trailing Distance | When to Use |

|---|---|---|---|

| Low Volatility | 1.5x – 2.0x | Tight | top stocks for covered calls; calm markets |

| Normal Volatility | 2.0x – 2.5x | Moderate | Standard swing trades; typical market conditions |

| High Volatility | 3.0x+ | Wide | Earnings season; major news events; high‑beta stocks |

This dynamic approach ensures your trades have enough room to breathe while still protecting your profits.

To keep your stops aligned with current conditions, update your ATR reading daily. During extreme volatility - when ATR exceeds its 90th percentile - some traders even cut their position sizes by 50% to maintain consistent risk, despite using wider stops.

Finally, ensure your trailing stop only moves in the trade's favor. Once adjusted, it should never retreat, even if volatility increases. This ratchet-like mechanism helps lock in profits while adapting to shifting market dynamics.

Mistake 4: Overlooking Options-Specific Factors

Using stock-style trailing stops for options is like trying to fix a watch with a sledgehammer - it’s the wrong tool for the job. Stocks are primarily influenced by price movement, but options bring additional complexities like time decay (theta), changing volatility (vega), and delta sensitivity into the mix. This means an option’s value can drop even if the underlying stock moves in your favor - something that doesn’t happen with stocks.

How Options Differ from Stocks in Stop Strategies

The key distinction? Options have an expiration date. Their value decreases over time, regardless of stock performance. Time decay accelerates as expiration approaches. For instance, an at-the-money option with 60 days left might lose $5 in value daily, but that same option with just one day to go could drop $80 per day. Relying on a trailing stop based solely on price ignores this time-sensitive erosion, often resulting in unnecessary exits that don’t reflect actual market conditions.

"Stop losses work well for stocks because price movement is the primary variable. In options trading, risk is multi-dimensional."

Liquidity adds another layer of complexity. Options generally have wider bid-ask spreads than stocks, and when trailing stops trigger market orders, the result can be significant slippage. This means your stop might execute at a far worse price than expected. Combine this with assignment risks, and it’s clear that percentage-based stops alone aren’t enough for managing options effectively.

These challenges call for a more nuanced approach to trailing stops.

Solution: Combine Percentage Trails with Delta or Time Thresholds

A better strategy blends percentage-based trails with metrics tailored to options. Delta serves as a useful indicator of the likelihood that an option will expire in-the-money. You can adjust your trailing stop dynamically - for example, tightening it as Delta moves from 0.30 to 0.50, signaling a higher probability of profit. This ensures your stops align with the option’s risk profile rather than just reacting to price changes.

Time-based exits are equally important. Many professional traders adopt a hard rule of exiting at 21 days to expiration, regardless of price action, to avoid the heightened gamma risk that comes in the final weeks of an option’s life. Adjusting your trailing stops based on implied volatility can also be valuable. For instance, you might widen your stop during a volatility spike to avoid being stopped out by short-term noise, and then tighten it when volatility drops to lock in gains. Tools like ThetaEdge can assist in monitoring these adjustments, helping you manage options with the precision they require instead of treating them like stocks.

Mistake 5: Over-Reliance on Trailing Stops Without Initial Hard Stops

Starting a trade without a hard stop in place leaves you exposed to significant risks. Trailing stops are designed to protect profits you’ve already made, but they don’t limit your initial losses. This gap in protection can leave you vulnerable to sharp market reversals, overnight gaps, or flash crashes that might devastate your position before the trailing stop even activates.

Why You Need Initial Hard Stops

A hard stop serves as your safety net from the moment you enter a trade. It sets a clear boundary for the maximum loss you’re willing to accept. Without this safeguard, you’re at the mercy of market volatility. For instance, if a gap occurs overnight or during a trading halt, your trailing stop won’t save you - it simply triggers a market order, which could execute much lower than your intended exit price.

"In futures trading, hope is not a strategy, and unprotected profits rarely survive."

- Kamil, Markets&Manners

Data backs this up. In E-mini S&P 500 futures day trading, fixed stops outperformed trailing stops in over 60% of tested strategies. The reason? Fixed stops provide immediate downside protection, ensuring that your losses are capped from the start. The takeaway is clear: establish your risk limits first, then focus on managing profits.

Combining Initial Stops with Trailing Stops

To address these risks, use both an initial hard stop and a trailing stop. Begin by setting a hard stop at 1–1.5x the Average True Range (ATR) below your entry price. This approach ties your maximum loss to market volatility rather than a random percentage. Once your trade moves in your favor - gaining 1.5–2x your initial risk - switch to a trailing stop. This gives the trade enough breathing room to develop without being prematurely closed by minor price movements.

For swing traders holding positions overnight, trailing stops performed better in about 70% of cases - but only when paired with an initial fixed stop to protect against gap risks. Tools like ThetaEdge can further refine this approach by offering portfolio-level risk analysis. These platforms monitor factors like Greeks, earnings risk, and assignment probability, which are critical for options traders. Since price-based stops alone can’t account for the multi-dimensional risks of options trading, such tools help ensure you’re managing your entire risk profile effectively.

Best Practices for Effective Trailing Stops

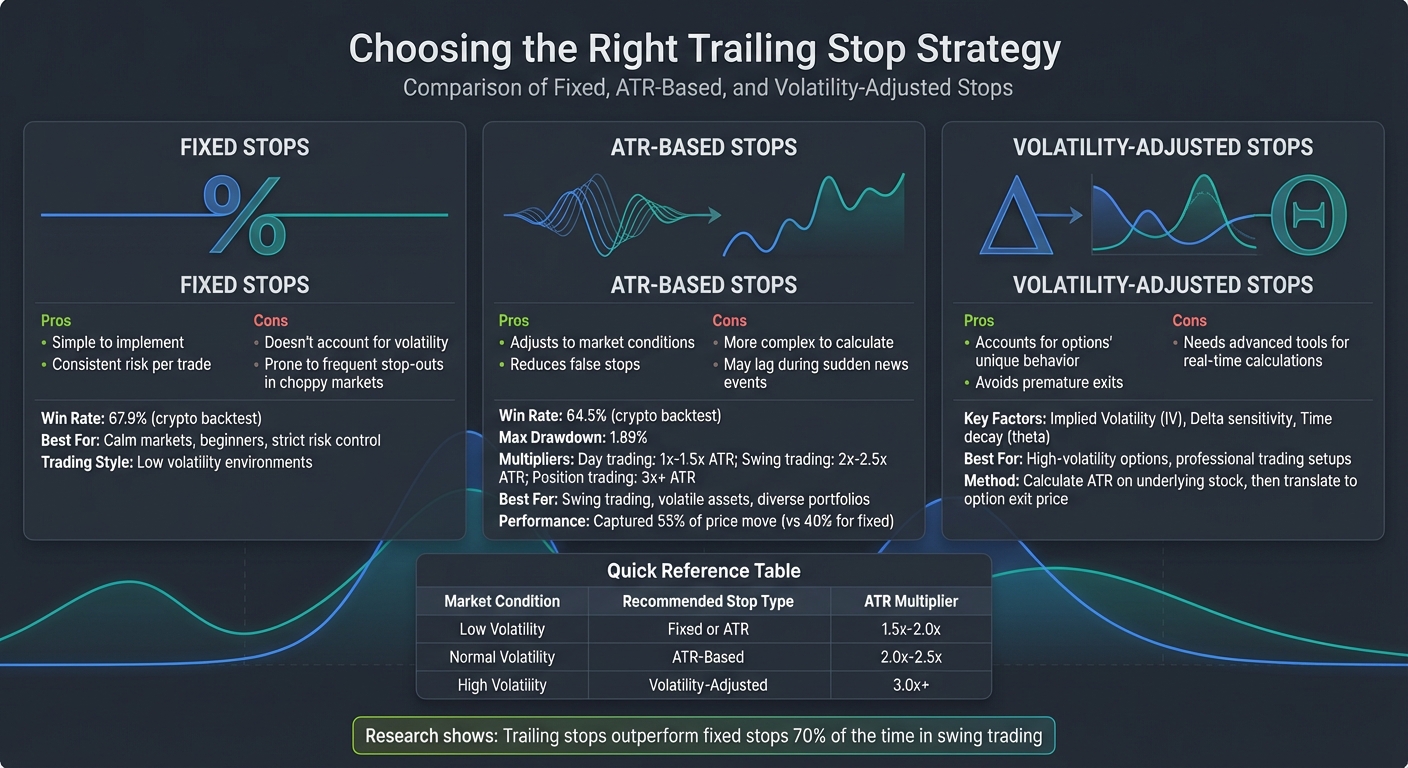

Trailing Stop Types Comparison: Fixed vs ATR-Based vs Volatility-Adjusted

Comparison of Fixed, ATR-Based, and Volatility-Adjusted Stops

Selecting the right type of trailing stop is key to refining your exit strategy. Fixed stops are straightforward and work well in stable, low-volatility markets. While they offer simplicity, they don’t adapt to changing market conditions. In highly volatile environments, they often lead to premature exits. For example, a backtest of over 10,000 crypto trades from 2024 to 2026 showed that a fixed -3.5% stop achieved a 67.9% win rate. However, a 3% trailing stop reduced that to 58.2% due to frequent whipsaws.

ATR-based stops are more dynamic, adjusting to market activity. These stops widen during high volatility and tighten when the market calms. Swing traders typically use a 2x to 2.5x ATR multiplier, while day traders stick to a tighter range of 1x to 1.5x to limit risk. In the same crypto backtest, an ATR-based stop with a 2x multiplier resulted in a 64.5% win rate and a maximum drawdown of just 1.89%. Similarly, in gold trading simulations, a fixed 30-pip trail captured only 40% of a price move, while an ATR 1.5x trail captured 55%.

Volatility-adjusted stops are tailored for options trading, where factors like Implied Volatility (IV) and Greeks play a significant role. Unlike stocks, options are influenced by time decay and delta shifts. To use this method, calculate the ATR-based stop based on the underlying stock price and then translate it into the option’s exit price. This approach minimizes distortions caused by options-specific factors. When IV increases, widen your trailing stop to avoid being stopped out by noise; when IV decreases, tighten it to secure profits.

Here’s a quick comparison of these trailing stop methods:

| Stop Type | Pros | Cons | Ideal Use Case |

|---|---|---|---|

| Fixed | Simple; consistent risk per trade | Doesn’t account for volatility; prone to frequent stop-outs in choppy markets | Best for calm markets, beginners, and strict risk control |

| ATR-Based | Adjusts to market conditions; reduces false stops | Requires more complexity; may lag during sudden news events | Ideal for swing trading, volatile assets, and diverse portfolios |

| Volatility-Adjusted | Accounts for options’ unique behavior; avoids premature exits | Needs advanced tools for real-time calculations | Best suited for high-volatility options and professional trading setups |

By tailoring your trailing stops to the asset type and market environment, you improve your ability to manage risk while maximizing returns.

Using Advanced Tools

Advanced tools can simplify the process of managing trailing stops, especially when dealing with complex calculations like ATR or IV. Manual calculations become cumbersome when managing multiple trades, but platforms like ThetaEdge can make this easier by offering portfolio-level risk analysis. This includes monitoring Greeks, earnings risk, and assignment probabilities - factors that simple price-based stops alone can’t address.

ThetaEdge provides AI-driven insights that align with your specific holdings, offering a clear breakdown of risks and potential trade-offs for each position. The platform also tracks portfolio Greeks, giving you a comprehensive view of your exposure. This is crucial when deciding how to adjust trailing stops across different trades. Additionally, the Thetix AI assistant integrates live market data and answers plain-language questions about your portfolio, allowing for real-time adjustments without the need to juggle multiple tools.

Conclusion

Trailing stops can safeguard your options profits - if used thoughtfully. However, common mistakes like setting stops too tight, making emotional tweaks, ignoring volatility, overlooking key options factors, or skipping initial hard stops can turn a protective tool into a costly misstep. To avoid these traps, consider strategies like using ATR-based or volatility-adjusted stops, automating your exit process for consistency, and pairing trailing stops with initial hard stops to limit losses effectively.

"In futures trading, hope is not a strategy, and unprotected profits rarely survive." - Kamil, Markets&Manners

Research backs the value of these methods. For instance, studies indicate that in swing trading, trailing stops outperform fixed stops about 70% of the time. This highlights the need to tailor your stop strategies to align with market conditions and the specific characteristics of your assets.

Discipline is key. Markets often retest entry points, and making emotional adjustments to your stops can undermine your entire strategy. Automating your exit process is a powerful way to avoid impulsive decisions and stick to a plan grounded in research, not gut feelings.

For traders managing multiple options positions, tools like ThetaEdge can simplify risk management and stop adjustments. This platform offers portfolio-level risk analysis, tracks Greeks, and provides AI-driven insights designed for your holdings. Its Thetix AI assistant even answers plain-language questions about your portfolio, helping you adjust stops in real time without needing to juggle multiple tools. By combining disciplined, volatility-aware strategies with ThetaEdge, you can better protect your gains while staying in control of your trades.

FAQs

What’s the best ATR setting for my trading style?

The right ATR (Average True Range) setting varies based on your trading time frame and the volatility of the market you're working in. Many traders default to a 14-period ATR, as it adapts to prevailing market conditions and can assist in determining appropriate trailing stop levels. However, it's worth testing various settings to ensure they align with your trading style and risk preferences.

Should my trailing stop be based on the option price or the underlying stock?

When setting a trailing stop, anchoring it to the underlying stock price is a smarter move. Here's why: the stock price directly influences the option's value. By focusing on the stock, your stop will adjust in line with market shifts, helping you lock in profits while managing risk effectively.

If you base your trailing stop on the option's price, you risk being thrown off by its volatility, which can fluctuate independently of the stock. Sticking to the stock price keeps your strategy more consistent and aligned with the market’s actual movement.

How do I avoid getting stopped out by options time decay?

To sidestep the challenges of time decay, aim to close positions around 21 days before expiration. This timing lets you take advantage of faster theta decay while steering clear of risks like assignment. A good rule of thumb is to lock in profits by capturing 50–75% of the premium or exit early to avoid the steep acceleration of time decay as expiration nears. These approaches balance income generation with a reduced impact from the erosion of extrinsic value.