Wash Sale Rules for Covered Calls

Wash sale rules can nullify covered-call losses, learn practical steps to avoid disallowed losses and protect tax basis.

Covered calls can generate income, but the IRS wash sale rule complicates tax planning when losses occur. This rule disallows claiming a loss if you repurchase a "substantially identical" security within 30 days before or after selling at a loss. For covered call traders, this includes stocks and options with similar terms. Disallowed losses are added to the cost basis of the new position, deferring the tax benefit. However, losses from taxable accounts repurchased in IRAs are permanently disallowed.

Key Points to Avoid Wash Sales:

- Wait 31 days before re-entering the same position.

- Change strike prices or expiration dates when rolling options.

- Avoid automatic reinvestments or trades across multiple accounts.

- Use AI tools to track positions and ensure compliance.

Understanding these rules helps you minimize tax issues while managing your covered call strategy effectively.

Wash Sale Rule Timeline and Avoidance Strategies for Covered Call Traders

What Is the Wash Sale Rule?

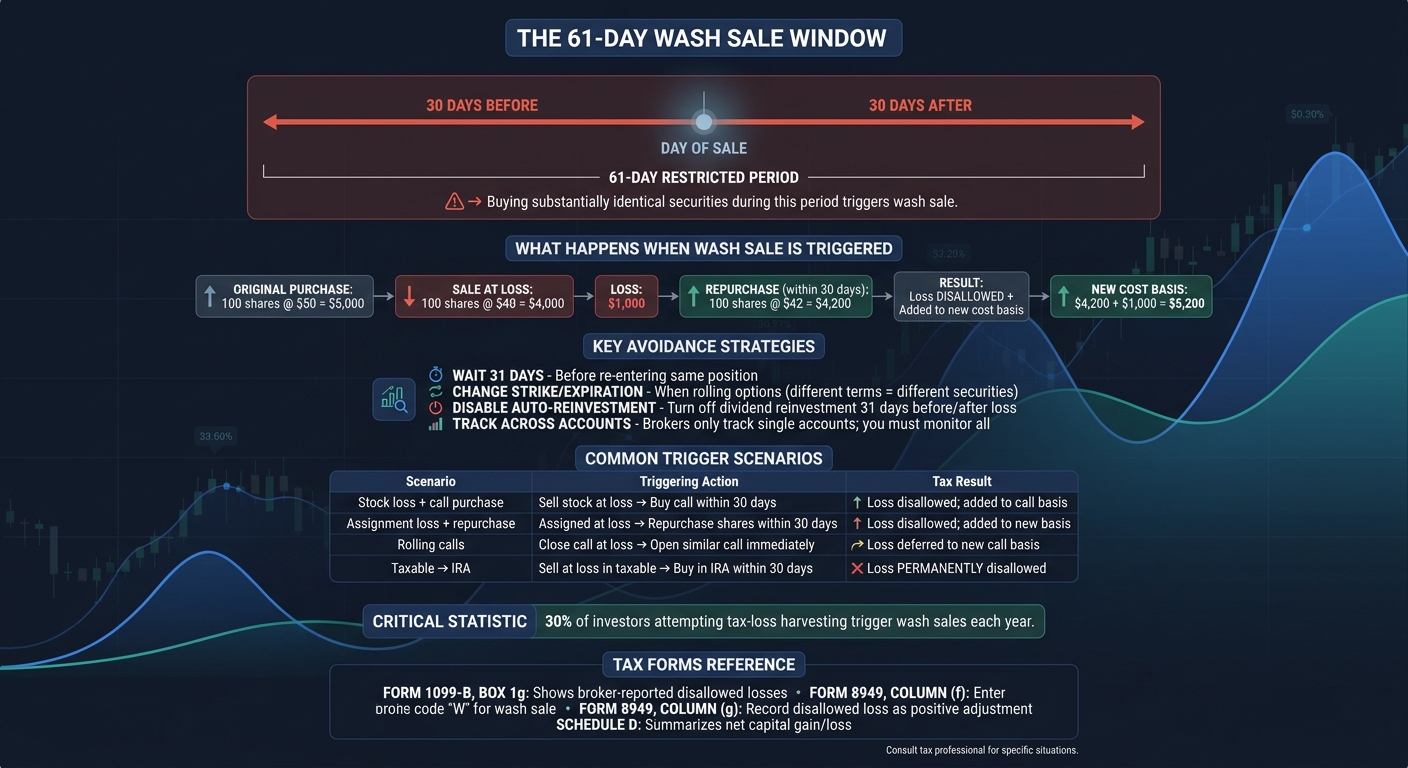

The wash sale rule stops investors from claiming tax losses if they quickly repurchase nearly identical securities. This rule applies when you sell a security at a loss and then buy a substantially identical one within a 61-day period - 30 days before the sale, the sale day itself, and 30 days after. For covered call traders, understanding this rule is especially important since the timing of repurchases in options strategies can unintentionally trigger it.

Here’s how it works: while the loss is disallowed for immediate tax purposes, it isn’t gone forever. Instead, it’s added to the cost basis of the new position, delaying the tax benefit until you eventually sell that replacement security. For example, let’s say you bought 100 shares of XYZ for $50 each (totaling $5,000), sold them at $40 each ($4,000), and then repurchased them at $42 each ($4,200) within 20 days. In this case, your $1,000 loss would be disallowed, and your new cost basis would jump to $5,200 ($4,200 purchase price plus the $1,000 deferred loss).

The IRS 30-Day Rule Explained

The wash sale rule operates within a 61-day window: 30 days before the sale, the sale day, and 30 days after. For instance, if you sold a stock at a loss on December 15 and then repurchased it on January 5, you’d fall within the restricted period, meaning you couldn’t claim the loss.

When a wash sale occurs, the disallowed loss gets added to the replacement security’s cost basis. This adjustment can reduce your taxable gain - or increase your loss - when you eventually sell. Additionally, the holding period from the original security transfers to the replacement. This can be helpful for qualifying sooner for long-term capital gains treatment.

However, there’s a key exception to note: if you sell a security at a loss in a taxable account and then repurchase it in an IRA within the 30-day window, the loss is permanently disallowed. It cannot be added to the IRA’s cost basis. Jacob Dayan, CEO of Community Tax, explains:

"If you sell a stock at a loss in a taxable brokerage account and repurchase it in your IRA within the 30-day window, the wash sale rule is triggered... the disallowed loss is permanently forfeited."

This principle also applies to options contracts, where timing rules for loss disallowance are similar.

How the Rule Applies to Options

The wash sale rule applies to options just as it does to stocks. The IRS generally considers options “substantially identical” if they share the same strike price and expiration date. For example, if you sell a covered call at a loss and then buy another call option with the same strike and expiration within 30 days, that would trigger a wash sale.

The rule can also come into play when mixing stocks and options. For instance, selling a stock at a loss and then buying a call option on the same stock within the 61-day window could trigger the rule, as the call option represents a contract to acquire the underlying shares. Evan Caldwell from OptionsTrading.org highlights this point:

"The Wash Sale Rule maintains that online options traders cannot claim losses on their taxes in the situation where they sell a security at a loss and buy an extremely similar security within 30 days before or after the sale."

One notable exception involves Section 1256 contracts, which include broad-based index options like SPX, RUT, and NDX. These are exempt from the wash sale rules. Since these contracts are marked-to-market at the end of the year, they simplify tax reporting for traders.

These specifics are essential for understanding how wash sales can affect covered call strategies - something we’ll dive into in the next section.

sbb-itb-a9ac3c2

Covered Call Scenarios That Trigger Wash Sales

Covered call traders need to be mindful of scenarios that can trigger wash sales. Recognizing these situations ahead of time can help you avoid unexpected tax complications.

When Covered Calls Get Assigned at a Loss

If your covered call is exercised, the IRS combines the call premium with the resulting stock sale into a single transaction. Your total proceeds are calculated as the strike price plus the premium. If this total is less than what you originally paid for the stock, you’ve incurred a loss. However, repurchasing the same stock within the wash sale period disallows the loss, which is then added to the cost basis of the new shares.

Here’s an example to clarify: say you bought 100 shares at $50 each (a $5,000 cost basis) and sold a $45 covered call for $2 per share, collecting a $200 premium. If the stock is assigned, your total proceeds would be $4,700 ($4,500 from the strike price plus $200 premium), leaving you with a $300 loss. If you then repurchase the stock at $44 within the wash sale window, the $300 loss is disallowed and added to the cost basis of the repurchased shares.

Next, let’s look at how rolling a call position can also lead to wash sales.

Rolling Covered Calls

Rolling a covered call at a loss and opening a new position could trigger a wash sale. The IRS may classify the two option contracts as "substantially identical". Unfortunately, the IRS doesn’t define precisely what makes two options different enough to avoid this rule. Even slight changes, like adjusting the strike price from $110 to $115, might not be enough.

Finance writer Gianluca Longinotti explains:

"If you choose to roll a losing call option position - for example, selling one option and immediately opening another with a similar strike or expiration - it could also be classified as a wash sale. The IRS may view this as repurchasing a nearly identical security."

In this scenario, the loss from the first call is deferred and added to the cost basis of the new call position.

Mixing Covered Calls with Other Options Strategies

Combining covered calls with other strategies can also trigger wash sale rules. For example, selling stock at a loss and then buying a call option on the same stock within 30 days could invoke the rule. Similarly, selling stock at a loss and then selling a deep-in-the-money (ITM) put may also create issues, as the IRS might interpret the put as an agreement to reacquire the stock.

Here’s a breakdown of common mixed-strategy triggers:

| Scenario | Triggering Action | Tax Result |

|---|---|---|

| Stock loss + call purchase | Sell stock at a loss, then buy a call within 30 days | Stock loss disallowed; loss added to call's basis |

| Stock loss + deep ITM put | Sell stock at a loss, then sell a deep ITM put within 30 days | IRS may view the put as a contract to repurchase stock |

| Assignment loss + stock repurchase | Being assigned at a loss then repurchasing shares within 30 days | Assignment loss disallowed; loss added to new basis |

| Call loss + similar call | Close a call at a loss and immediately open a similar call | Loss deferred into the new call's cost basis |

Using tools like ThetaEdge’s portfolio-aware analysis can help investors track their positions and avoid unintentionally triggering wash sales.

Understanding these scenarios is key before delving into strategies to navigate wash sale rules effectively.

How to Avoid Wash Sales with Covered Calls

You don't have to give up on covered calls to steer clear of wash sales. With some thoughtful tweaks, you can stay compliant with tax rules while continuing to generate income.

Once you understand what triggers wash sales, you can use these strategies to sidestep them effectively.

Adjust Strike Prices or Expiration Dates

When rolling a covered call at a loss, altering the strike price or expiration date can help you avoid triggering the wash sale rule. The IRS considers options with different terms as distinct securities, not "substantially identical."

Options expert Evan Caldwell from OptionsTrading.org puts it this way:

"Having different strike prices and expiration dates make the securities different enough that it wouldn't qualify as a wash sale."

For example, if you close a $50 call at a loss and roll into a $55 call - even with the same expiration date - the change in strike price typically avoids a wash sale. Similarly, rolling to a different expiration month while keeping the same strike price also works. These adjustments let you reposition without running afoul of tax rules.

Wait 30 Days Before Re-Entering

A straightforward but cautious method is to wait at least 31 days after closing a losing position before re-entering with the same strike and expiration. This ensures you're outside the 61-day window that could trigger a wash sale. While this approach guarantees compliance, it may delay your market re-entry and potential profits [8,1].

If waiting isn't a viable option, consider other strategies.

Trade Similar but Different Securities

To maintain market exposure without triggering wash sales, you can switch to a related but not identical security. For instance, you might trade a competitor's stock or choose an ETF that tracks a different index. If you're trading ETF options, sector ETFs or Section 1256 index options like SPX or XSP could be good alternatives [4,17].

Section 1256 index options, such as SPX or XSP, are entirely exempt from wash sale rules because of their mark-to-market tax treatment. If you're using covered calls on SPY, it might be worth exploring whether SPX or XSP options align better with your tax strategy.

Additionally, disable any automatic dividend reinvestment or rebalancing features for at least 31 days before and after harvesting a loss. This precaution helps prevent accidental wash sale triggers.

For those managing their own portfolios, advanced platforms like ThetaEdge can provide tools to monitor positions and suggest timely adjustments. These features allow you to refine your covered call strategy while staying compliant with tax regulations.

Tax Reporting and Record Keeping

Getting your tax reporting right for covered calls starts with keeping detailed records and ensuring they align with your broker's Form 1099-B and Form 8949.

What Your Broker Reports

At the end of the year, your broker provides Form 1099-B, which outlines your trading activity. Pay close attention to Box 1g - it lists any wash sale losses that have been disallowed. These disallowed amounts are also reflected on Form 8949, where you'll need to:

- Enter code "W" in Column (f) to indicate a wash sale adjustment.

- Record the disallowed loss as a positive adjustment in Column (g).

However, brokerage systems only track wash sales within a single account. They might miss wash sales involving "substantially identical" securities, such as selling stock at a loss and buying a deep-in-the-money call option.

| Form/Box | Purpose in Wash Sale Reporting |

|---|---|

| 1099-B, Box 1g | Shows losses disallowed by the broker due to a wash sale |

| Form 8949, Column (f) | Used to indicate a wash sale adjustment with code "W" |

| Form 8949, Column (g) | Records the disallowed loss as a positive adjustment |

| Schedule D | Summarizes totals from Form 8949 to calculate net capital gain or loss |

After reviewing the disallowed losses reported by your broker, you need to adjust the cost basis of your replacement securities accordingly.

Tracking Your Adjusted Cost Basis

For covered calls, monitoring cost basis adjustments is a must. When a loss is disallowed, it gets added to the cost basis of the replacement security, delaying the tax benefit until you sell it.

This process requires manual tracking. For example, if you sell stock at a loss and then write a new covered call within 30 days, or if you're frequently rolling calls, your broker won’t calculate these adjustments for you across different security types. You’ll need to handle it yourself.

The formula is simple: New Basis = Cost of Replacement + Disallowed Loss

If you repurchase fewer shares than you originally sold, only part of the loss is disallowed, proportional to the number of shares replaced.

How Wash Sales Affect Your Returns

Wash sales delay your ability to deduct losses, which can impact your taxable income. Disallowed losses reduce your current-year deductions, potentially increasing your tax bill now. However, these losses don’t disappear - they’re folded into the cost basis of your replacement security. This adjustment will lower your taxable gain (or increase your deductible loss) when you eventually sell the replacement.

Keeping thorough records of your trades - dates, quantities, and prices - is essential. This helps you understand your actual investment performance and prevents unpleasant surprises when tax season rolls around.

If you’re managing multiple covered call positions, tools like ThetaEdge can simplify the process by helping you stay on top of your holdings and track the details needed for accurate tax reporting.

Key Takeaways

The wash sale rule creates a 61-day window around any loss sale: 30 days before, the day of the sale, and 30 days after. During this period, buying substantially identical securities or options triggers the rule, disallowing your loss deduction. For covered call traders, this can occur in several ways: when stock is assigned at a loss and immediately repurchased, when rolling positions without changing the strike price or expiration date, or when dividend reinvestment plans automatically purchase shares. These scenarios highlight the importance of careful tax planning when using covered calls.

To avoid triggering the wash sale rule:

- Wait at least 31 calendar days before re-entering a position after a loss sale.

- When rolling covered calls, make sure to adjust either the strike price or the expiration date.

- Turn off automatic dividend reinvestment at least 31 days before and after a loss sale.

The impact of a wash sale depends on the account type. In taxable accounts, the disallowed loss is added to the cost basis of your replacement security, deferring the tax benefit until you sell. However, if the wash sale occurs due to purchasing shares in an IRA within 30 days of selling at a loss in a taxable account, the loss is permanently disallowed - there is no basis adjustment or future recovery.

Surprisingly, about 30% of investors attempting tax-loss harvesting trigger wash sales each year. Common missteps include forgetting about dividend reinvestment, trading the same stock across multiple accounts, and failing to coordinate with a spouse’s account. It’s worth noting that brokers only track wash sales within a single account for the same security, leaving you responsible for monitoring across all accounts.

If you manage multiple covered call positions across accounts, keeping detailed records is crucial. Track all trades with specifics like dates, quantities, prices, and account information to ensure compliance. By following these strategies, you can fine-tune your covered call approach while staying aligned with tax regulations.

FAQs

Are two covered calls “substantially identical” if only the strike or expiration changes?

Two covered calls are not classified as substantially identical if their only differences lie in the strike price or expiration date. The term "substantially identical securities" involves broader criteria, and such minor variations usually fall outside that definition.

Can rolling a covered call create a wash sale even if I never repurchase the stock?

Rolling a covered call won’t lead to a wash sale unless you purchase the same or a substantially identical stock within 30 days before or after the transaction. Adjusting the call position alone, without buying the underlying stock, doesn’t meet the wash sale criteria.

How do I track wash sales across taxable and IRA accounts when my broker doesn’t?

To keep track of wash sales manually, you’ll need to maintain thorough records of your trades. This includes noting purchase and sale dates, security identifiers, and the type of account involved (e.g., taxable or IRA). Pay close attention to whether you - or your spouse - purchased a substantially identical security within the 30-day window before or after selling at a loss. If this happens, adjust your tax reporting by adding the disallowed loss to the cost basis of the repurchased security, ensuring you stay in line with IRS regulations.