Delta-Neutral Rebalancing: Basics for Investors

How to build and maintain delta-neutral option positions, manage Greeks, set rebalancing rules, and control costs.

Delta-neutral rebalancing is a method to reduce the impact of small price movements on your portfolio by offsetting positive and negative deltas to create a net delta of zero. This strategy doesn't freeze portfolio value but minimizes sensitivity to short-term market fluctuations. Here's what you need to know:

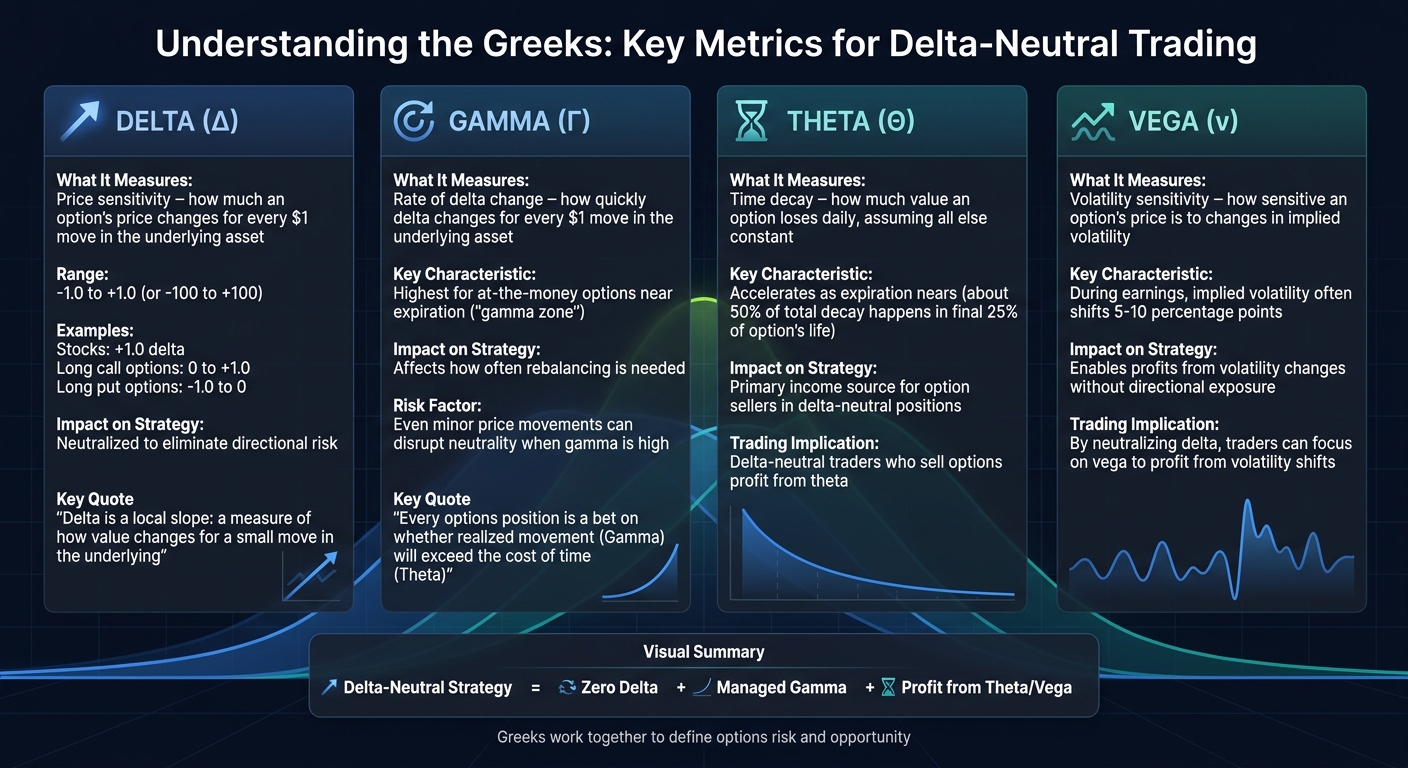

- Delta measures how much an option's price changes with a $1 move in the underlying asset. Stocks have a delta of +1.0, while options vary between -1.0 and +1.0.

- Delta-neutral positions balance opposing deltas. For example, owning 100 shares (+100 delta) can be offset by two at-the-money put options (-100 delta).

- It's useful for managing short-term volatility without selling long-term holdings.

- Other Greeks like gamma (rate of delta change), theta (time decay), and vega (volatility sensitivity) also influence delta-neutral strategies.

While delta-neutral trading can help manage risk and capture income from time decay or volatility shifts, it requires regular monitoring. Delta changes with price, time, and volatility, so rebalancing is essential but can incur costs. Tools like ThetaEdge simplify tracking and adjustments, ensuring your portfolio stays aligned with your goals.

Core Concepts of Delta-Neutral Strategies

Options Greeks Guide: Delta, Gamma, Theta, and Vega Explained

Understanding Delta and Its Function

Delta measures how much an option's price is expected to change for every $1 move in the underlying asset. Think of it as a gauge for how sensitive your position is to price changes.

Delta values range from -1.0 to +1.0 (sometimes expressed as -100 to 100). For instance, a long call option has a positive delta between 0 and +1.0, meaning it gains value when the stock price rises. On the other hand, a long put option has a negative delta ranging from -1.0 to 0, benefiting when the stock price falls. For stocks, each share has a delta of +1.0, as it moves in lockstep with the price.

Delta also acts as a hedge ratio. For example, if you own an at-the-money call with a delta of 0.5, you'd need two such contracts to neutralize the directional risk of holding 100 shares of stock. To calculate the total position delta, multiply the delta of an option by the number of contracts and then by 100. For example, holding 5 contracts with a delta of 0.30 results in a total position delta of 150.

It’s crucial to remember that delta is not fixed. As Sara Toshi from Cube Exchange puts it:

"Delta is not magic and it is not a promise. It is a local slope: a measure of how the value of a position changes for a small move in the underlying around the current point".

Once delta is understood, the next step is to explore how other Greeks - gamma, theta, and vega - affect delta-neutral strategies.

Other Greeks to Track: Gamma, Theta, and Vega

Delta-neutral trading becomes more nuanced when you consider the roles of other Greeks. These metrics help fine-tune risk management and adapt to market dynamics.

Gamma reflects how quickly delta changes for every $1 move in the underlying asset. Even minor price movements can disrupt neutrality, especially when gamma is high. This is particularly evident in at-the-money options close to expiration, where gamma can swing delta dramatically with just a $1 stock move. Such extreme gamma conditions, often referred to as the "gamma zone", highlight the balancing act traders face. As the StrikeWatch EA Research Team explains:

"Every options position is fundamentally a bet on whether realized movement (Gamma) will exceed the cost of time (Theta)".

Theta represents time decay, or how much value an option loses daily, assuming all else stays constant. For delta-neutral traders who sell options, theta often serves as the primary income source. However, time decay accelerates as expiration nears, with about half of the total decay happening in the final 25% of an option's life.

Vega measures how sensitive an option's price is to changes in implied volatility. By neutralizing delta, traders can focus on vega to profit from shifts in volatility rather than price direction. For example, during earnings announcements, implied volatility often shifts by 5–10 percentage points, potentially impacting option prices more than the stock’s actual movement.

| Greek | What It Measures | Impact on Delta-Neutral Strategy |

|---|---|---|

| Delta | Price sensitivity | Neutralized to eliminate directional risk |

| Gamma | Rate of delta change | Affects how often rebalancing is needed |

| Theta | Time decay | Key income driver for option sellers |

| Vega | Volatility sensitivity | Enables profits from volatility changes without directional exposure |

sbb-itb-a9ac3c2

How to Build and Maintain Delta-Neutral Positions

Setting Up Delta-Neutral Positions

Start by calculating your delta exposure. For example, if you own 200 shares of a stock priced at $100, your delta is +200 because each share has a delta of 1. To neutralize this, you need to add positions that create a net delta of –200.

One common way to achieve this is by using at-the-money (ATM) options. These typically have deltas of around 0.5 for calls and –0.5 for puts. To offset the share exposure, you could buy 4 ATM put contracts. Since each contract covers 100 shares, the calculation looks like this: 4 × 100 × –0.5 = –200 delta. This adjustment would bring your portfolio's net delta to zero.

Another option is constructing a long straddle, which involves purchasing equal amounts of ATM calls and puts. Other strategies, like short straddles, iron condors, or calendar spreads, can also help minimize directional risk while targeting profits from volatility or time decay. Each approach suits different market conditions but shares the goal of reducing directional exposure.

Once your position is set up, keeping an eye on delta changes is crucial so you can adjust as needed to maintain neutrality.

When to Rebalance for Neutrality

Maintaining a delta-neutral position isn’t a one-and-done task. Market movements cause delta to shift, making periodic rebalancing essential. There are three main triggers for rebalancing: fixed intervals (like daily or weekly), price-percentage thresholds (e.g., a 10% change in the underlying stock), or delta bands (adjusting when the net delta drifts beyond a set range).

Studies show that regular rebalancing can significantly reduce losses compared to leaving positions unadjusted. However, rebalancing too often isn’t always the best choice. While it can help manage volatility and protect against trending markets, frequent adjustments increase transaction costs and might cause you to miss out on gains during mean-reversion periods.

"A common mistake is to set up a delta neutral position and not rebalance it, leading to the position becoming directionally exposed as delta inevitably shifts." - Explain Options

Positions with high gamma, such as ATM options nearing expiration, require closer monitoring because even small price movements can cause significant delta changes. During times of increased volatility, it may make sense to rebalance more frequently. Conversely, in calmer markets, using wider thresholds can be more efficient. Always consider the impact of commissions and slippage to ensure rebalancing adds value rather than eroding your returns.

Managing Risk and Position Sizing

Calculating Delta and Portfolio Exposure

Delta is a key metric when managing risk in options trading. For stocks, the delta is straightforward: ±1.0. For options, it's calculated by multiplying the option's delta by the number of contracts and then by 100. For instance, holding three call contracts with a delta of 0.75 would result in a delta exposure of 225 (3 × 0.75 × 100).

To understand your overall portfolio exposure, sum up the deltas of all individual positions. This single figure indicates how much your portfolio's value will shift for every $1 move in the underlying asset. When managing a mix of stocks or ETFs, beta-weighting is useful. It aligns all positions to a common benchmark, like the S&P 500. For example, a beta-weighted delta of 7 means your portfolio value changes by about $7 for every $1 move in the S&P 500.

"Portfolio delta takes all of your position deltas and the betas of the underlying securities and relates them into a single market position." - Option Alpha

Delta is also crucial for hedging. To neutralize a long stock position with options, divide the number of shares by the option's delta. For example, if you own 100 shares and use puts with a delta of -0.50, you’d need two contracts to hedge effectively (100 ÷ 0.50 = 2). However, delta isn't static; it shifts with market movements, a phenomenon measured by gamma. As a result, regular monitoring and adjustments are necessary to maintain neutrality.

Once you’ve calculated your delta exposure, set clear risk limits to prepare for inevitable market changes.

Setting Risk Limits

Establishing risk limits is essential for managing delta neutrality in a dynamic market. Aiming for a perfect zero delta at all times is unrealistic and expensive. Instead, define a delta range that allows for some flexibility before rebalancing. For instance, you might permit your portfolio delta to vary between -10 and +10 before taking action. This approach minimizes transaction costs while keeping your directional exposure under control.

Keep in mind the impact of gamma. Significant price swings can alter your delta unexpectedly, even if you started neutral. Monitoring secondary Greeks like gamma, theta, and vega is important to address risks beyond delta. Also, factor in transaction costs - frequent rebalancing can erode profits quickly.

Adjust your rebalancing schedule based on your strategy. High-gamma positions near expiration might require daily adjustments, while lower gamma exposures could be managed on a weekly or monthly basis. For larger portfolios, focus on rebalancing less liquid positions first to reduce market impact costs. Remember, delta-neutral strategies protect against small price movements but won’t shield you from large, sudden market shifts without proper gamma management. Continuously review your risk limits and monitor secondary Greeks to stay prepared.

Tools for Delta-Neutral Portfolio Management

Using ThetaEdge for Portfolio Analysis

ThetaEdge simplifies managing delta-neutral positions by connecting securely to over 80 brokerages, including Schwab, Fidelity, Interactive Brokers, and Robinhood. This connection is read-only, ensuring your portfolio is analyzed without the risk of unauthorized trades.

What sets ThetaEdge apart is its portfolio-aware analysis. Instead of relying on generic ticker symbols, it focuses on your actual holdings and cost basis to identify tailored opportunities. Whether you're exploring covered calls, protective puts, or multi-leg strategies, the platform provides detailed insights, including full Greek metrics and assignment probabilities.

If your portfolio's delta drifts outside your target range, ThetaEdge's roll management tools step in with suggestions. These tools offer credit/debit analysis alongside updated assignment probabilities, helping you make informed adjustments.

"I worried I'd have to move all my investments or learn complicated trading tools. But here, I keep my accounts where they are, and everything's explained in plain language." - Sarah C., Marketing Director

ThetaEdge offers a 14-day free trial that doesn’t require a credit card, allowing you to explore features like scenario modeling and "what-if" analysis before making portfolio adjustments. Its integrated tools also include real-time Greek tracking, ensuring your delta-neutral strategy stays on course.

Tracking Portfolio Greeks

ThetaEdge makes monitoring Greek exposures straightforward and essential for maintaining delta neutrality. Its unified dashboard consolidates your portfolio's total delta, gamma, theta, and vega exposure, offering a clear view of your risk profile. This helps you spot concentrated risks, ensuring no single position skews your portfolio's directional bias.

Custom alerts can be set to notify you when key thresholds are crossed. For example, significant changes in delta or volatility can trigger alerts, ensuring you're ready to rebalance when necessary.

The platform’s Thetix AI assistant simplifies complex Greek data into actionable insights. Using live market feeds and your portfolio data, it explains risk trade-offs without pushing specific trades. It continuously updates based on market conditions, supporting your delta management decisions in real time.

For those managing portfolios across multiple accounts, ThetaEdge’s multi-brokerage integration is invaluable. It consolidates your holdings into a single interface, allowing you to track beta-weighted delta against benchmarks like the S&P 500. This eliminates the need for tedious spreadsheet updates, making delta-neutral strategy management more efficient and streamlined.

Key Takeaways

Delta-neutral rebalancing offers a way to manage investments without predicting market direction. By balancing positive and negative deltas to achieve net-zero exposure, investors can focus on profiting from time decay (theta) or changes in volatility (vega) rather than relying on price movements.

However, maintaining this balance requires constant attention. Investors need to monitor gamma - the rate at which delta shifts - because significant market moves can quickly disrupt neutrality. Setting clear rebalancing thresholds, such as +/- 30 delta, can help manage costs while ensuring effective hedging remains intact.

For self-directed investors, delta-neutral strategies provide a way to safeguard short-term profits without liquidating long-term positions. These strategies tend to work well in markets that are trading within a range or during periods of heightened volatility around major events. That said, sudden market swings can still result in losses due to gamma risk.

Specialized tools can make managing these strategies more efficient. For instance, ThetaEdge simplifies delta-neutral management by offering portfolio-specific insights, real-time tracking of Greeks, and recommendations for adjustments when delta strays from target levels. Its unified dashboard highlights exposures to delta, gamma, theta, and vega, helping investors identify risks and maintain neutrality across multiple accounts with ease.

FAQs

How do I choose a good delta range before rebalancing?

To choose an effective delta range, focus on keeping your net delta close to zero by offsetting positive and negative deltas. Many traders use a range, such as -10 to +10, and adjust their positions whenever the delta moves outside this boundary. This strategy helps you stay near-neutral, minimizes directional risk, and provides room to adapt to market fluctuations - all while staying aligned with your overall risk management objectives.

What risks remain after I’m delta-neutral?

Even with a delta-neutral position, there are still risks lurking beneath the surface. These include volatility changes, gamma risk, and unexpected market movements that can alter your portfolio's delta. On top of that, sharp price swings or inaccuracies in your pricing model can lead to losses. Keeping an eye on these factors and fine-tuning your strategy as conditions evolve is crucial to maintaining balance.

How do I hedge a stock position with options using delta?

To manage risk in a stock position using delta, the goal is to build a delta-neutral portfolio. This means balancing positive and negative deltas to minimize exposure to price changes in the underlying stock.

- Calculate the stock's delta: Each share of stock carries a delta of +1. Multiply this by the number of shares you own to find the total delta for your position.

- Use options for balance: Incorporate options with opposing deltas to offset the stock's delta. For example, buying puts with a delta of -0.5 can help neutralize the positive delta from your shares.

- Monitor and adjust: As market prices fluctuate, delta values shift. Regularly rebalance your portfolio to maintain a neutral stance and stay aligned with your risk management goals.

Delta-neutral strategies require ongoing attention, but they can effectively reduce directional risk in your portfolio.