Gamma vs Delta: Key Differences Explained

Compare Delta and Gamma in options trading: what each measures, how gamma alters delta, and practical tips for managing positive and negative gamma.

When trading options, Delta and Gamma are two critical metrics that help you understand how your position reacts to price changes:

- Delta measures how much an option's price changes for every $1 move in the stock. It also estimates the probability of the option expiring in-the-money.

- Gamma measures how much Delta changes for every $1 move in the stock, showing how quickly your position's sensitivity evolves.

Key Points:

- Delta ranges from 0 to 1 for calls and -1 to 0 for puts. It reflects your position's price sensitivity.

- Gamma is highest for at-the-money options and increases as expiration approaches, making Delta more reactive.

- Positive Gamma (buying options) amplifies gains and cushions losses, while Negative Gamma (selling options) increases risk as prices move.

Quick Comparison:

| Metric | Delta (Δ) | Gamma (Γ) |

|---|---|---|

| What It Measures | Price sensitivity (speed) | Delta sensitivity (acceleration) |

| Range (Calls) | 0 to +1.0 | Always positive for long positions |

| Range (Puts) | -1.0 to 0 | Always positive for long positions |

| Peak Condition | Deep in-the-money | At-the-money |

| Impact of Time | Becomes more binary near expiry | Increases sharply near expiry |

Understanding these metrics helps you manage risk and position effectively, whether you're buying or selling options. Using an options strategy planner can further help you visualize how these Greeks impact your overall portfolio.

Delta vs Gamma in Options Trading: Key Differences and Characteristics

What Is Delta?

Delta Definition and Basics

Delta (Δ) is a key metric in options trading, showing how much an option's price is expected to change when the underlying stock moves by $1.00. In simple terms, it measures how sensitive an option is to the stock's price changes.

"Delta is perhaps the most fundamental of all the Greeks. It measures the rate of change in an option's price relative to a $1.00 change in the underlying asset's price." - ImpliedOptions Research

Call options have delta values between 0 and 1.00, while put options range from -1.00 to 0. For instance, a call option with a delta of 0.60 would increase in value by $0.60 if the stock price rises by $1.00. Similarly, a put option with a delta of -0.40 would gain $0.40 if the stock drops by $1.00.

Delta serves three main purposes:

- Sensitivity: It shows how much the option's price reacts to stock price changes.

- Probability Estimate: A delta of 0.30 suggests roughly a 30% chance the option will expire in-the-money.

- Share Equivalency: A delta of 0.50 means the option behaves like owning 50 shares of the stock.

This foundational understanding of delta sets the stage for exploring how it shifts depending on factors like moneyness and position size.

How Delta Varies by Position and Moneyness

Delta behaves differently depending on whether an option is in-the-money, at-the-money, or out-of-the-money. At-the-money options usually have a delta around 0.50 for calls and -0.50 for puts. Deep in-the-money options approach a delta of 1.00 (calls) or -1.00 (puts), while out-of-the-money options have deltas closer to 0, meaning their prices are less sensitive to small stock movements.

For directional trades, experienced traders often prefer options with deltas between 0.40 and 0.60. This range strikes a balance between affordability and responsiveness. On the other hand, premium sellers - those focused on income strategies - frequently choose options with deltas between 0.15 and 0.30. These deltas align with a theoretical 70% to 85% chance of profit.

The sign of delta also varies with position type:

- Buying a call: Positive delta, benefiting from rising stock prices.

- Selling a call: Negative delta, profiting if the stock price falls.

- Buying a put: Negative delta, gaining value when the stock price drops.

- Selling a put: Positive delta, earning if the stock price rises.

It's worth noting that delta isn't fixed. It fluctuates as the stock price moves, time passes, and market volatility changes. Understanding these shifts is crucial, especially when considering how gamma - another Greek - affects delta and overall option behavior.

sbb-itb-a9ac3c2

What Is Gamma?

Gamma Definition and Basics

Gamma (Γ) measures how much an option's delta changes when the underlying stock price moves by $1.00. Think of it as the rate of change for delta. While delta shows how sensitive an option is to price movements, gamma reveals how quickly that sensitivity shifts.

"If Delta is your speedometer, Gamma is your acceleration pedal - it tells you how quickly your speed (Delta) is increasing or decreasing." – StrikeWatch EA Research Team

When you buy options - whether they’re calls or puts - you’re dealing with positive gamma. This means your delta improves as the stock price moves in your favor. On the flip side, selling options gives you negative gamma, which works against you as price movements intensify. You can use AI-powered portfolio analysis to monitor how these shifts impact your overall risk.

Gamma also explains the concept of convexity. This is why gains can snowball when the trade goes your way, while losses slow down when the market moves against you. To fully grasp gamma’s role, it’s important to understand how it behaves based on moneyness and time until expiration.

How Gamma Changes with Moneyness and Time

Gamma peaks for at-the-money options because there’s the most uncertainty about whether they’ll expire in or out of the money. Even small price movements can cause significant shifts in delta for these options. However, as options move deeper in- or further out-of-the-money, gamma shrinks. That’s because delta approaches its limits - either 1.0 or 0 - leaving less room for change.

Time also plays a major role. An at-the-money option with just 7 days left until expiration can have nearly three times the gamma of one with 60 days remaining. The last few days before expiration - often referred to as the "gamma zone" - can see gamma spike dramatically. For instance, an at-the-money AAPL $200 call might see its gamma climb from 0.012 with 45 days left to over 0.50 as expiration approaches.

This surge happens because the option is rapidly approaching a definitive outcome: either becoming worthless (delta near 0) or fully in-the-money (delta nearing 1.0). Additionally, when implied volatility is low, gamma for at-the-money options tends to increase, making delta even more reactive to price changes in a calmer market.

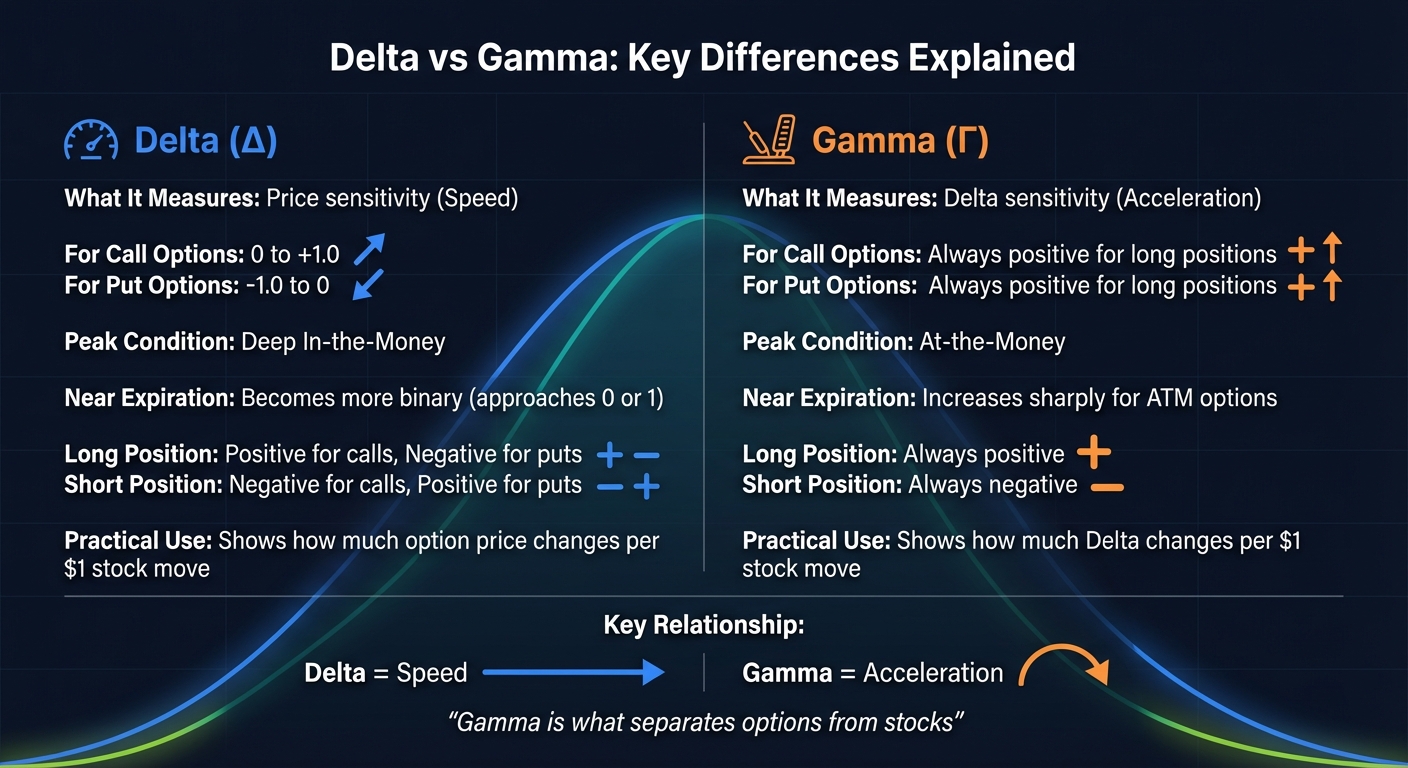

Gamma vs Delta: Key Differences

Delta and gamma each play distinct roles in options trading. Let's explore how they differ and how gamma influences delta during active trades.

Comparison Table: Delta vs Gamma

Delta and gamma measure how options react to price changes, but they focus on different aspects. Delta reflects how much the option's price will move with a $1 change in the underlying asset, while gamma tracks how delta itself evolves as prices shift. Think of delta as the speed of price movement and gamma as the acceleration behind it.

| Feature | Delta (Δ) | Gamma (Γ) |

|---|---|---|

| Primary Measure | Price sensitivity (Speed) | Delta sensitivity (Acceleration) |

| Range (Calls) | 0 to +1.0 | Always positive for long positions |

| Range (Puts) | -1.0 to 0 | Always positive for long positions |

| Peak Condition | Deep In-the-Money | At-the-Money |

| Impact of Time | Becomes more "binary" (0 or 1) near expiry | Increases sharply for ATM options near expiry |

| Short Position | Negative for calls; Positive for puts | Always negative |

This breakdown highlights how delta and gamma operate differently, laying the groundwork for understanding their interplay during price changes.

How Gamma Affects Delta During Price Movements

Gamma doesn’t just tweak delta - it reshapes how your position responds to market shifts. Gamma introduces a nonlinear element, making options behave unlike stocks. When gamma is positive, your profits can grow faster as the underlying asset moves in your favor, while losses slow down when the price moves against you. This dynamic occurs because gamma continually adjusts delta as prices change.

Take this example: Imagine holding an AAPL call option with a delta of 0.50 and gamma of 0.05. After a $1 increase in AAPL's price, delta rises to 0.55. With another $1 move, delta climbs to 0.60. The second dollar of movement generates more profit than the first, thanks to gamma's influence.

For short positions, the effect flips - losses accelerate, and gains slow down. This heightened risk often leads experienced premium sellers to close their trades roughly 21 days before expiration to avoid the extreme gamma exposure that can develop.

"Gamma is what separates options from stocks." - StrikeWatch EA Research Team

Managing Gamma and Delta in Your Trades

Managing gamma and delta effectively is what often separates successful traders from the rest. The tactics you use will depend on whether you're dealing with positive or negative gamma positions, as each comes with its own set of challenges and opportunities.

Positive Gamma Positions

When you buy calls or puts, you're working with positive gamma. This means delta adjusts in your favor - rising when the stock moves your way and shrinking when it moves against you. Essentially, positive gamma helps cushion losses during adverse moves while amplifying gains during favorable ones.

However, this benefit comes at a cost: theta decay. A general guideline among experienced traders is to keep an eye on the daily theta cost. If it exceeds 30% of the option's price over your planned holding period, it might be time to consider a spread strategy to offset that expense. Positive gamma positions tend to perform well in volatile markets, where actual price swings surpass the cost of holding the option.

To get the most out of positive gamma, many traders focus on at-the-money (ATM) options with 30–45 days to expiration (DTE). For instance, an ATM option at 45 DTE might have a gamma of 0.012, offering meaningful delta adjustments without the extreme swings seen closer to expiration. If your trade moves deeply in-the-money, gamma decreases, and delta approaches 1.0. At that point, rolling into a new ATM option can help reset your gamma exposure and unlock further profit potential , a technique often used when you generate monthly income with covered calls. This approach ensures you stay in control and ready to adapt as market conditions evolve.

Negative Gamma Positions

Short gamma positions, on the other hand, require a completely different mindset. Selling options - whether it's puts, calls, or credit spreads - creates negative gamma. Here, delta works against you as the stock price moves, and losses can escalate quickly in unfavorable conditions. The trade-off? You collect premium and benefit from theta decay, which works best in markets that stay within a predictable range.

"Selling options for premium? Gamma is your enemy." - John Manley, DMS

Managing negative gamma demands precision and discipline. The final days before expiration - the so-called "gamma zone" - are where time decay and gamma risk skyrocket. For example, an ATM option at 7 DTE might have a gamma of 0.045, but as expiration approaches, that number can jump to 0.50 or more. This means delta could shift by 0.50 for every $1 move in the stock, making the position far more volatile. To mitigate this risk, many professional traders exit around 21 DTE or after capturing 50% of the maximum profit.

Staying on top of your gamma and delta exposure is crucial. Tools like ThetaEdge can provide detailed insights into these dynamics, helping you identify the best moments to enter and exit trades. For income strategies like covered calls or cash-secured puts, this kind of analysis can be a game-changer, allowing you to manage risks effectively while capitalizing on time decay. The key takeaway? While short gamma positions can deliver consistent income, they require constant vigilance - one sharp market move can turn a manageable trade into a costly mistake.

Conclusion: Understanding Gamma and Delta

Grasping both gamma and delta is key to navigating the complexities of options trading. These metrics help you anticipate how your positions will respond to market movements. Delta measures your position's current exposure to price changes, while gamma shows how quickly that exposure can shift.

"Gamma is what separates options from stocks. A stock position has constant exposure... An option position has changing exposure because of Gamma."

– StrikeWatch EA Research Team

This interplay creates the convexity that makes options trading unique. Long gamma positions can amplify gains while cushioning losses. In practical terms, aiming for a delta range of 0.40–0.60 for directional trades and selecting options with 30–45 days to expiration when selling premium can help you balance responsiveness with controlled gamma risk. It's wise to avoid holding positions into the final week before expiration, as at-the-money options experience sharp gamma spikes, turning small price moves into significant swings in profit and loss. Adapting your strategies to these dynamics is crucial as market conditions evolve.

For precise management of covered calls and income strategies, tools like ThetaEdge provide real-time analysis. Ultimately, delta and gamma are two sides of the same coin - understanding both ensures you're trading with clarity and control.

FAQs

How do I use Delta to size an options position?

Delta represents how much an option's price shifts with a $1 change in the underlying stock's price. For instance, if an option has a Delta of 0.50, its price will increase by $0.50 for every $1 rise in the stock.

When determining your position size, focus on the total Delta exposure you aim for. To find the number of contracts to trade, divide your desired Delta by the Delta of the option. This approach helps you align your position with your risk preferences.

Why does Gamma spike near expiration?

As an option approaches its expiration date, Gamma increases sharply. This happens because Delta - the measure of an option's sensitivity to price changes in the underlying asset - starts shifting at a much faster rate. With this heightened sensitivity, even small movements in the underlying asset's price can cause dramatic changes in the option's Delta, leading to a noticeable spike in Gamma during this critical period.

What’s the safest way to manage negative Gamma risk?

Managing negative Gamma risk effectively requires strategies that help balance exposure and limit potential losses from sharp price swings. One such method is gamma hedging, which includes using delta-gamma neutral spreads. This involves adjusting your positions to offset gamma exposure, ensuring your portfolio remains more stable even during significant market moves. By doing this, you can better safeguard against steep losses while keeping control over your investments.