Earnings Volatility: Whisper Numbers Explained

How whisper numbers drive earnings volatility, sway stock reactions more than consensus, and how options traders manage IV crush.

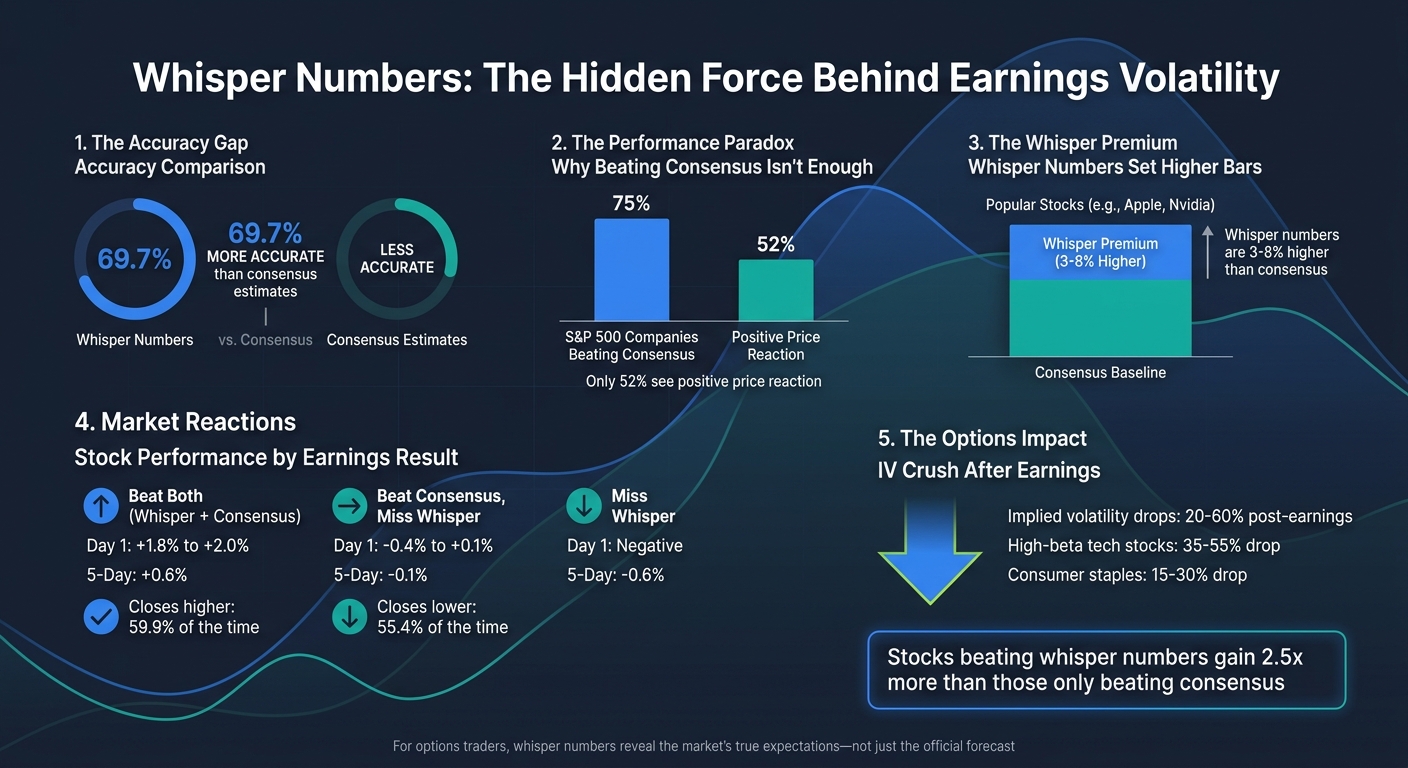

Whisper numbers - unofficial earnings forecasts shared among insiders and analysts - often dictate stock price movements more than consensus estimates. While about 75% of S&P 500 companies beat consensus expectations, only 52% see a positive price reaction. The reason? Whisper numbers set a higher bar, and failing to exceed them can lead to stock declines, even if official estimates are surpassed.

Key takeaways:

- Whisper numbers are often 3–8% higher than consensus estimates for popular stocks like Apple or Nvidia.

- Stocks beating both whisper and consensus numbers gain 2.5x more than those only beating the consensus.

- Whisper numbers are 69.7% more accurate than consensus estimates in predicting actual earnings.

- Options traders face IV crush (20–60% volatility drop) post-earnings, making understanding these numbers critical for strategy.

For options traders, whisper numbers provide vital context for timing trades and managing risks, especially during earnings season. Knowing the market's true expectations can help avoid costly surprises.

Whisper Numbers vs Consensus Estimates: Key Statistics and Market Impact

What Are Whisper Numbers?

Whisper numbers play a key role for options traders dealing with the unpredictable nature of earnings season. These are unofficial EPS (earnings per share) forecasts shared by insiders and market participants. Unlike the consensus estimates you see on platforms like Yahoo Finance or Bloomberg, whisper numbers reflect the real expectations of the market - the hurdle a company must clear to spark a positive price movement.

In the past, whisper numbers often came from sell-side analysts who had revised their internal models but hadn’t yet published updated reports. Per Afrell, a former UBS Warburg analyst, explained that these insider insights often differed from the official estimates, forming the basis of what we now call whisper numbers.

After regulations like the Sarbanes-Oxley Act were implemented, the way whisper numbers were generated shifted. Today, they rely heavily on portfolio intelligence - factors like supplier and customer surveys, management signals, competitor performance, and trends in the options market. Retail sentiment, particularly from social media and investment forums, has also become a growing influence. This evolution has made whisper numbers more dynamic and often more accurate than traditional estimates, creating a noticeable gap between official forecasts and actual market expectations.

For popular stocks such as Apple or Nvidia, whisper numbers are often 3% to 8% higher than the consensus estimates. This creates a two-layered system: the consensus estimate serves as the "floor", while the whisper number represents the real target. For instance, if a stock sees a 10% rally in the 20 days leading up to earnings without any change in official estimates, it’s a sign that the market is pricing in a whisper number well above the consensus.

Whisper Numbers vs. Consensus Estimates

The distinction between whisper numbers and consensus estimates isn’t just theoretical - it has a direct impact on stock price movements after earnings announcements. Consensus estimates are publicly available averages of forecasts from sell-side analysts at banks and investment firms. These are updated infrequently since analysts don’t revise their reports for every small adjustment to their models. Whisper numbers, on the other hand, are constantly updated through private discussions, proprietary data models, and real-time market activity.

As of June 2023, whisper numbers were more accurate than consensus estimates 69.7% of the time. Stocks that exceeded whisper numbers saw an average one-day gain of over 2%, while those that beat the consensus but missed the whisper only gained about 0.1%.

Take Yahoo! in July 2005 as an example. Analysts projected earnings of $0.13 per share, but the whisper number was $0.15. When Yahoo reported $0.13 - matching the official estimate - the stock still dropped 8% within five days because it fell short of the whisper. As WhisperNumber.com aptly puts it:

Traders know estimates don't move markets, expectations move markets.

Here’s a side-by-side comparison to clarify the differences between these two forecasting approaches:

| Feature | Official Consensus Estimate | Whisper Number |

|---|---|---|

| Source | Sell-side analysts (investment banks) | Buy-side traders and retail sentiment |

| Availability | Publicly available (e.g., Bloomberg, Yahoo Finance) | Unofficial, shared through private channels or specialized platforms |

| Accuracy | Lower (average miss rate: 44%) | Higher (average miss rate: 21%) |

| Market Role | Acts as the "official" benchmark for media | Serves as the "real" benchmark for institutional traders |

| Update Frequency | Infrequent (requires formal reports) | Constantly updated through real-time data and conversations |

The market tends to treat whisper numbers as the true benchmark. An estimated 20-25% of S&P 500 companies beat the official consensus but still see their stock prices decline because they fail to meet the whisper number. For options traders, this means that simply beating the consensus isn’t enough - clearing the whisper threshold is what truly drives positive market reactions.

sbb-itb-a9ac3c2

How Whisper Numbers Drive Earnings Volatility

Whisper numbers play a pivotal role in fueling earnings volatility because they act as the market's unofficial benchmark, often overshadowing the published consensus. When a stock climbs 10% in the 20 days leading up to an earnings report without any corresponding change in official estimates, it signals that investors are trading on expectations well above the consensus. This divergence is a key reason for the market's unpredictable behavior during earnings season.

This dynamic creates a two-tier system: beating the consensus isn't always enough. While most S&P 500 companies surpass consensus estimates, fewer manage to exceed the higher whisper number. The result? Stocks that beat the consensus but fall short of the whisper often experience flat or negative reactions, with an average decline of 0.1% over the next five days. Meanwhile, stocks that beat both the consensus and the whisper typically enjoy a stronger market response, gaining over 2% on the first trading day and often triggering larger price movements.

The volatility doesn't stop there. Post-Earnings Announcement Drift (PEAD) reveals that stocks exceeding the whisper number tend to gain roughly 0.6% over the next five days, while those missing it see a similar decline. These patterns of volatility set the stage for various options strategies, which capitalize on these swings.

Market Reactions to Whisper Beats and Misses

Market reactions to whisper numbers highlight the stark differences between beating and missing these unofficial benchmarks. Stocks that beat the whisper number close higher 59.9% of the time, with an average gain of 1.8%. On the flip side, stocks that beat the consensus but miss the whisper close lower 55.4% of the time, with an average daily loss of 0.4%.

Take Apple (AAPL) in July 2005 as an example. The consensus estimate for its earnings was $0.31 per share, while the whisper number was $0.33. Apple reported $0.37, exceeding both benchmarks. The stock surged from $38 to $43 within five days - a 13% jump - and hit $45 within 30 trading days. In contrast, Yahoo! (YHOO) in the same month had a consensus estimate of $0.13 and a whisper of $0.15. When Yahoo! reported $0.13, meeting only the consensus, its stock fell from about $37 to $34, an 8% drop in just five days.

Options markets further magnify this volatility through what’s known as IV Crush. Implied volatility often drops by 20% to 60% immediately after an earnings announcement as the uncertainty surrounding the whisper number dissipates. For high-beta tech stocks like Tesla or Nvidia, this drop can range from 35% to 55%, while consumer staples see a smaller reduction of 15% to 30%. This means that even if you correctly predict the direction of the earnings move, the sharp decline in implied volatility can still eat into the profitability of a long option position.

| Scenario | Average Day 1 Reaction | 5-Day Post-Earnings Drift |

|---|---|---|

| Beat Consensus + Beat Whisper | +1.8% to +2.0% | +0.6% |

| Beat consensus but miss whisper | −0.4% to +0.1% | −0.1% |

| Miss Whisper (General) | Negative | −0.6% |

Using Whisper Numbers in Options Trading

Grasping the concept of whisper numbers is one thing, but turning that understanding into profitable options trades requires a bit more finesse. The market often reacts to whisper numbers - unofficial earnings expectations - rather than the consensus estimates. For popular stocks like NVDA, TSLA, or AAPL, whisper numbers generally exceed consensus estimates by 3–8%. This gap can create opportunities for traders who can spot when a stock might react strongly to either exceeding or missing these whispered expectations.

One way to approach this is by identifying discrepancies where options pricing doesn’t align with historical earnings reactions. For instance, if a stock typically moves 4% on earnings but the options market is pricing in a 7% move, it could signal that traders are already anticipating a whisper-driven surprise. Another clue lies in pre-earnings momentum. If a stock climbs 8–15% in the 20 days before earnings without any changes to the official consensus, it may indicate that the market is pricing in a whisper beat. However, if the company only meets the whisper number and not exceeds it, the stock might experience a "sell the news" scenario, dropping even after beating the official consensus. Recognizing these patterns can help pinpoint stocks primed for whisper-driven moves.

Finding Stocks That React to Whisper Numbers

The best candidates for whisper-based trading tend to have high institutional ownership, strong analyst coverage, and a history of significant post-earnings moves. A useful tool for narrowing down options is the IV–RV spread, which measures the gap between implied volatility (IV) and realized volatility (RV). When IV is at least 40% higher than RV, it suggests the market is bracing for a big move.

Past performance also plays a role. Some stocks consistently need to exceed whisper numbers by a specific margin - say 8% or more - to generate positive price action, even if they beat the official consensus. Additionally, the term structure of implied volatility can provide insights. If near-term IV surpasses far-term IV (a condition called backwardation), it confirms that the market is pricing in a major earnings event. These metrics help traders zero in on stocks that are likely to react sharply to earnings.

| Sector | Typical IV Drop After Earnings | Example Tickers |

|---|---|---|

| Biotech | 40–70% | MRNA, BIIB, REGN |

| High-beta tech | 35–55% | TSLA, NVDA, AMD |

| Mega-cap tech | 30–50% | AAPL, MSFT, AMZN |

| Financials | 20–35% | JPM, GS, BAC |

| Consumer staples | 15–30% | WMT, COST, PG |

Once you’ve identified responsive stocks, you can employ tailored multi-leg strategies to make the most of earnings-driven volatility.

Using Multi-Leg Strategies for Earnings Events

Multi-leg options strategies - like straddles, strangles, iron condors, and calendar spreads - are designed to profit from the volatility swings whisper numbers often trigger. Each has its strengths, depending on your outlook and risk tolerance.

- Straddles are ideal when you expect a significant move but aren’t sure about the direction. By buying both an at-the-money call and put, you can profit if the stock moves sharply in either direction. For example, purchasing a straddle priced at $28.70 per share (or $2,870 per contract) on a stock trading at $575.50 would require the stock to move over 5% to cover costs and the typical IV drop. This strategy works well when whisper numbers and consensus estimates diverge widely, signaling high uncertainty.

- Strangles are a lower-cost alternative, involving out-of-the-money calls and puts. While cheaper upfront, they require a larger price move to turn profitable.

- Iron condors are suited for situations where you expect less movement than the market predicts. By selling out-of-the-money calls and puts while buying further out-of-the-money options to cap risk, you can profit from the post-earnings IV drop - especially when IV is 40% or more above RV. However, precision is essential, as losses can mount if the stock moves beyond your short strikes.

- Calendar spreads target IV differences between front- and back-month options. This involves selling the front-month option (expiring at earnings) and buying the back-month option. As front-month IV collapses post-earnings while back-month IV remains steady, the spread widens, benefiting your position. This strategy is great for traders who want to focus on volatility dynamics without taking on directional risk.

"IV crush means you can be right on direction and still lose money on a long options position. The stock moves 3% in your favor, but IV drops 40%, and your option is worth less than you paid for it." - FlashAlpha

To maximize the effectiveness of these strategies, validate your thesis with open interest and volume data. Look for unusual options activity, where current volume exceeds the prior day's open interest. This can indicate new positions are being opened, rather than existing ones being closed.

ThetaEdge: Tools for Whisper-Driven Options Analysis

Once you’ve got a handle on the basics of options strategies, tools like ThetaEdge can help you apply them with precision. During earnings season, when whisper numbers often spark volatility, having the right analysis tools becomes crucial. ThetaEdge is an Options Intelligence platform tailored for self-directed investors, offering insights specific to your portfolio. Unlike generic screeners that start with random tickers, ThetaEdge connects to over 80 brokerages through read-only access, analyzing your actual holdings. It filters and ranks earnings opportunities based on the stocks you already own.

By leveraging real portfolio data, ThetaEdge helps you navigate the volatility that earnings reports can bring. The platform tracks key metrics like earnings exposure, Greeks, and price momentum across your positions. This makes it easier to spot when whisper-driven volatility creates opportunities for strategies such as covered calls, cash-secured puts, or multi-leg setups. Each opportunity is presented with detailed trade-off insights, including strike price, expiration, premium, delta-based assignment probabilities, and breakeven points - giving you the context needed to decide if a stock's implied volatility premium is worth acting on.

"Options intelligence is continuous, not a one-time lookup." – ThetaEdge

ThetaEdge has analyzed over $300 million in assets, helping users generate $6.3 million in premiums. With an average portfolio size of $350,000, its users tend to be serious investors seeking advanced analysis without the complexity of institutional-grade tools. This focus on tailored insights makes ThetaEdge a valuable resource for refining your approach to earnings volatility.

Features for Earnings Volatility Analysis

ThetaEdge’s analysis engine evaluates dozens of potential setups for each position, identifying the best annualized yield while factoring in structured risk metrics. For earnings events, the platform lets you compare strategies - like a covered call on one stock versus a cash-secured put on another - filtered by your personal risk tolerance and premium goals. It offers three customizable risk profiles, so you can adjust the analysis to match your preferences.

During earnings season, real-time monitoring becomes indispensable. ThetaEdge tracks profit and loss with time decay while flagging changes like rising assignment risk or hitting preset profit targets. For instance, if you sold a covered call ahead of an earnings report and the stock rallies on a whisper beat, ThetaEdge will alert you when assignment risk increases or when you’ve captured around 35% of the maximum premium. This allows you to lock in gains before implied volatility (IV) drops after the report. For multi-leg strategies like straddles, strangles, or iron condors, the platform provides full Greeks, probability models, and defined-risk metrics - essential for managing IV crush. On top of these features, Thetix AI simplifies real-time decisions even further.

Using Thetix AI for Whisper Analysis

Thetix AI, ThetaEdge’s plain-English assistant, takes portfolio data and live market feeds and turns them into actionable insights. Instead of sifting through raw data, you can ask Thetix questions like, “What happens to my TSLA covered call if the stock beats the whisper number by 5%?” or “Should I roll my AMD put before earnings?” Thetix provides verified numbers and clear explanations, steering clear of guesswork.

Ahead of earnings, Thetix lets you model what-if scenarios around whisper beats or misses. For example, on May 5, 2026, Advanced Micro Devices Inc (AMD) had a whisper number of $1.34 compared to Wall Street’s consensus of $1.29, showing a 4.03% positive spread. With Thetix, you could explore how a 4% upside surprise might affect your position’s breakeven or assignment probability, helping you decide whether to adjust your strikes or hold steady.

The AI also remembers context across sessions, so you can build on earlier queries without starting over - a big plus when juggling multiple earnings plays. Additionally, ThetaEdge sends out a daily AI-generated email digest, highlighting new opportunities as your portfolio and market conditions evolve. For those curious to try it out, the platform offers a 14-day free trial with no credit card required, making it easy to test its features during earnings season.

Conclusion

Whisper numbers reveal the market's true expectations during earnings season, offering insights that go beyond consensus estimates. For options traders, understanding this gap is critical. A stock can surpass consensus estimates but still fall short of the whisper number, leading to a price drop - a nuance that can make or break a trade.

The data highlights this dynamic: stocks beating the whisper number typically close higher by an average of 1.8% and rise 59.9% of the time. On the other hand, stocks that beat consensus but miss the whisper number close lower 55.4% of the time. For options traders, this distinction becomes even more crucial when paired with IV crush. Even if you're correct about the stock's direction, a whisper miss can trigger both a price drop and a volatility collapse, potentially wiping out gains on a long call position.

ThetaEdge offers a tailored approach to navigating earnings volatility. By analyzing your actual portfolio and factoring in key metrics like Greeks, assignment probabilities, and breakeven points, it evaluates whether a stock's implied volatility premium justifies the trade. Whether you're considering an iron condor to capitalize on IV crush or a covered call in anticipation of a whisper beat, the platform focuses on your specific holdings rather than generic screeners. This personalized analysis provides a practical framework for managing earnings-related risks.

From decoding whisper numbers to applying complex options strategies, the insights shared here underscore the value of aligning trades with genuine market expectations. By integrating whisper number awareness with structured options analysis, you can turn earnings volatility into a calculated opportunity. Knowing what the market truly anticipates - and understanding how it impacts your positions - allows you to make deliberate, informed decisions rather than reactive moves.

FAQs

Where can I find a stock’s whisper number?

Whisper numbers for a stock can be found on platforms that gather unofficial earnings estimates from traders and other market participants. These include websites dedicated to earnings whispers and platforms that compile aggregated forecasts. Such sources offer a glimpse into market expectations beyond the official guidance, which can help inform trading strategies and timing decisions.

How can I tell if a stock’s price already reflects a whisper beat?

When a stock trades above the whisper number before earnings are announced, it could mean that the market has already priced in a potential "whisper beat." Stocks tend to gain when they surpass the whisper number and face losses when they miss it. Watching how a stock's price moves leading up to earnings can offer clues about investor expectations.

How do I trade earnings when IV crush can wipe out long options?

To navigate earnings trades and sidestep the impact of implied volatility (IV) crush on long options, it’s essential to reduce vega exposure. One approach is to sell options using strategies like vertical spreads or iron condors. These setups allow you to take advantage of the IV drop after earnings while keeping your risk under control.

Another tactic is to purchase options well ahead of the earnings announcement when IV is still low. By closing or rolling these positions before the announcement, you can avoid holding them during the peak IV period, reducing the chance of significant losses from the volatility drop.