IV Rank vs IV Percentile: Key Differences

A concise guide comparing IV Rank and IV Percentile—how they’re calculated, pros/cons, and when to use each for options trading.

When trading options, knowing that a stock's implied volatility (IV) is 30% isn't enough. Is 30% high or low for this stock? That’s where IV Rank and IV Percentile come in. Both compare today’s IV to its past year’s history, but they do it differently:

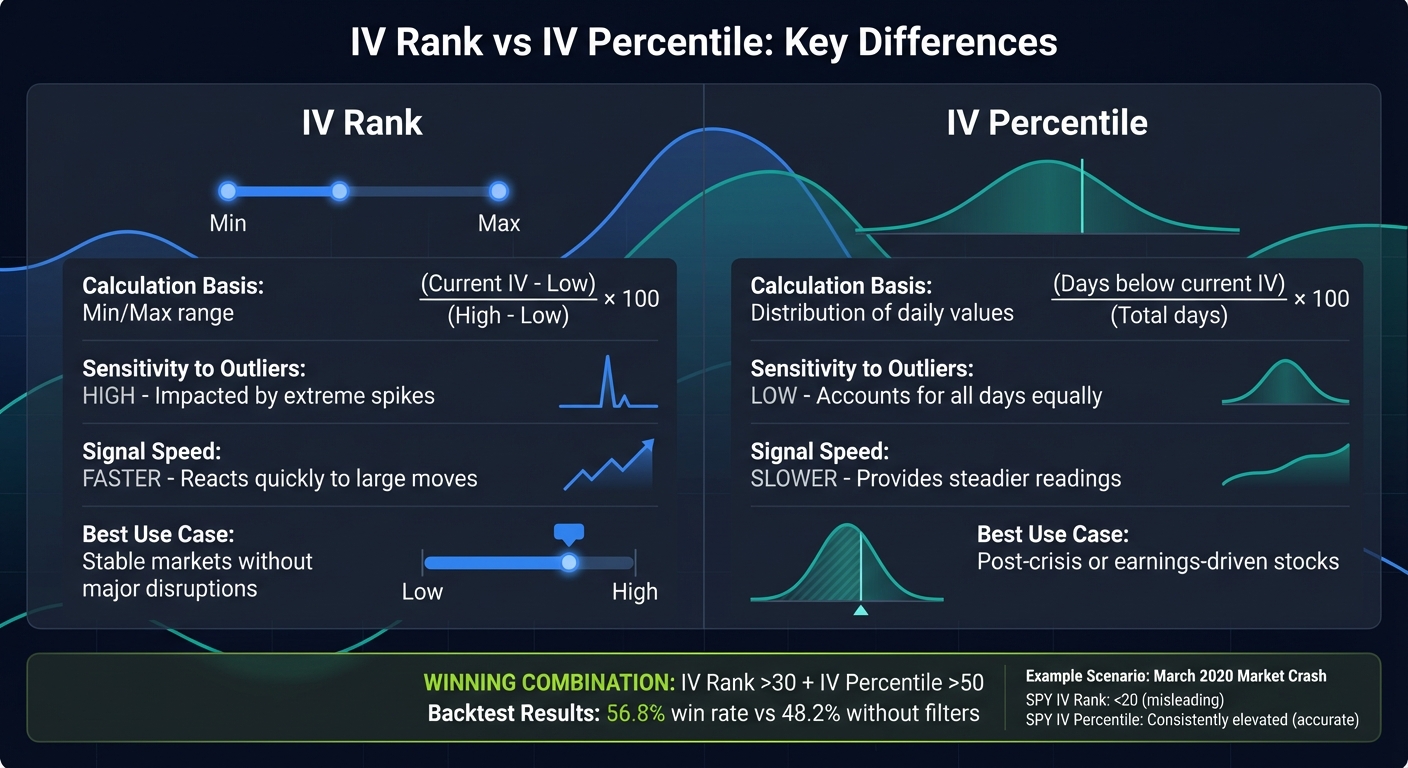

- IV Rank: Measures where today’s IV falls between its 52-week high and low, expressed as a percentage.

- IV Percentile: Shows how many days over the past year had IV lower than today’s level.

Each has strengths: IV Rank reacts quickly to changes, while IV Percentile smooths out one-off spikes, offering a broader perspective. Traders often use both together to identify high or low volatility periods for strategies like premium selling or buying options.

Here’s why it matters: Backtests show filtering trades with IV Rank > 50 and IV Percentile > 50 improves win rates for strategies like short iron condors from 48.2% to 56.8%. You can also use AI-powered portfolio analysis to monitor these metrics in real-time. Let’s break down how these metrics work and when to use them.

What Is IV Rank and How Is It Calculated?

IV Rank measures today's implied volatility (IV) in relation to its range over the past year. It places the current IV on a scale from 0 to 100, where 0 represents the lowest IV in the last 52 weeks and 100 represents the highest.

The IV Rank Formula

The formula for IV Rank is:

(Current IV - 52-week Low IV) / (52-week High IV - 52-week Low IV) × 100

To calculate IV Rank, you’ll need three key values: the current IV, the lowest IV in the past year, and the highest IV during that same period. For instance, if Apple (AAPL) has a current IV of 28%, a 52-week low of 18%, and a 52-week high of 45%, the calculation would look like this:

(28 - 18) / (45 - 18) × 100 = 37%.

How Traders Use IV Rank

Traders rely on IV Rank to assess whether options are priced high or low compared to their historical range. This assessment is a critical step when using an options strategy planner to select the right trade. When the IV Rank is above 50, options are considered relatively expensive. Conversely, a rank below 30 suggests they are relatively cheap.

However, IV Rank has its limitations. A single extreme volatility spike can skew the 52-week high, leading to misleading results. To address this, traders often pair IV Rank with IV Percentile, which provides a broader perspective. For example, some traders set thresholds like an IV Rank above 30 combined with an IV Percentile above 50 to filter out anomalies and avoid false signals.

Next, we’ll look at how IV Percentile can enhance these evaluations.

sbb-itb-a9ac3c2

What Is IV Percentile and How Is It Calculated?

IV Percentile gauges how often implied volatility (IV) has been below its current level. Instead of just comparing the highest and lowest IV points over the past year, it calculates the percentage of trading days when IV was lower than it is now.

The IV Percentile Calculation Method

The formula is simple:

(Number of Days with IV Below Current IV ÷ Total Trading Days in Period) × 100.

Typically, the calculation uses a 252-day lookback period, representing one calendar year.

Here’s an example: Imagine Tesla (TSLA) has a current IV of 55%. If, over the past 252 trading days, IV was below 55% on 189 of those days, the IV Percentile would be:

189 ÷ 252 × 100 = 75%.

This means Tesla's IV is in the 75th percentile.

One reason traders rely on IV Percentile is its ability to handle outliers. A sudden volatility spike - caused by something like a market crash or an earnings surprise - only counts as a single day in the calculation. This keeps the IV Percentile stable, unlike IV Rank, which could be skewed for an entire year by that one event. As FlashAlpha explains:

Percentile is telling the truth [after a spike]. Current IV is near the top of the stock's normal operating range - the spike was an outlier that has nothing to do with today's opportunity.

How Traders Use IV Percentile

Traders use IV Percentile to spot consistent premium opportunities rather than relying on one-off extremes. When IV Percentile is above 50%, it typically signals that options are priced higher than usual, making it a good time for premium-selling strategies. If it climbs above 70% or 80%, it suggests volatility is at the upper end of its historical range.

For strategies with higher risk, like short strangles, traders often wait for IV Percentile to exceed 60%. On the other hand, when IV Percentile drops below 25% or 30%, options are considered historically inexpensive. This creates opportunities for buyers, favoring strategies such as long straddles or debit spreads.

Main Differences Between IV Rank and IV Percentile

IV Rank vs IV Percentile Comparison Chart for Options Trading

Grasping the distinctions between IV Rank and IV Percentile is essential for traders looking to analyze market conditions effectively and time their trades with precision.

How the Calculations Differ

IV Rank compares today's implied volatility (IV) to its high and low over the past year, while IV Percentile measures how often IV has been lower than today's value during the same period. Essentially, IV Percentile reflects the percentage of trading days when volatility was below the current level.

The way these metrics are calculated leads to notable differences. IV Rank, being based solely on the annual high and low, can be heavily influenced by outliers. For example, imagine Apple (AAPL) typically trades with an IV range of 18% to 45%, and the current IV is 28%. This would result in an IV Rank of 37%. However, if a market crash once pushed the IV high to 65%, the same 28% IV would yield an IV Rank of only 21%, making volatility appear misleadingly low. IV Percentile, on the other hand, incorporates all 252 trading days, so a one-time spike like this would carry much less weight - only about 0.4% of the data - providing a more balanced perspective.

These subtle differences impact how each metric identifies trading opportunities, which is further clarified in the comparison below.

Side-by-Side Comparison: IV Rank vs IV Percentile

The table below outlines the key differences between these two metrics:

| Attribute | IV Rank | IV Percentile |

|---|---|---|

| Calculation Basis | Min/Max range | Distribution of daily values |

| Formula | (Current IV - Low) / (High - Low) × 100 | (Days below current IV) / (Total days) × 100 |

| Sensitivity to Outliers | High – impacted by extreme spikes | Low – accounts for all days equally |

| Signal Speed | Faster; reacts quickly to large moves | Slower; provides steadier readings |

| Best Use Case | Stable markets without major disruptions | Post-crisis or earnings-driven stocks |

These differences are especially noticeable during volatile market events. Take the March 2020 market crash: the IV Rank for SPY (S&P 500 ETF) dropped below 20 for months, even though implied volatility remained far above pre-pandemic levels. In contrast, IV Percentile consistently indicated elevated conditions, offering a clearer picture.

Many traders now combine both metrics as a filter, requiring an IV Rank above 30 and an IV Percentile above 50 before initiating short premium trades. This dual approach has been shown to improve outcomes. For instance, backtested results reveal a win rate of 56.8% for short iron condors when applying this filter, compared to just 48.2% without IV-based criteria.

When to Use Each Metric

Choosing between IV Rank and IV Percentile depends on the market environment. IV Rank is ideal for steady, predictable conditions, while IV Percentile shines after significant market disruptions. Let’s dive into the specifics.

When IV Rank Works Best

IV Rank performs well in stable markets. It measures where current implied volatility (IV) falls between its highest and lowest points over the past year, making it a quick and responsive tool. For short-term traders - especially during earnings season or when sector-specific news breaks - IV Rank provides actionable insights into volatility shifts.

This metric is particularly useful for stocks with consistent volatility patterns. Such securities avoid extreme, one-off spikes that could skew the data, allowing traders to spot when options premiums transition from low to high. This can signal opportunities for selling premiums or adjusting positions.

For example, an IV Rank above 70 before earnings suggests volatility is nearing its peak. This often sets up a favorable scenario for strategies like an earnings iron condor.

Now, let’s shift focus to IV Percentile and its strengths.

When IV Percentile Works Best

In the aftermath of major disruptions, such as the market crash in March 2020, IV Percentile proves more reliable. Unlike IV Rank, it consistently highlights historically high IV levels, making it a better choice for such conditions.

Michael Martin, Vice President of Market Strategy at TradingBlock, emphasizes this point:

"If I had to pick, I'd lean on IV Percentile since it smooths out one-off spikes."

– Michael Martin, Vice President of Market Strategy, TradingBlock

This metric is especially effective for stocks that frequently experience volatility spikes, such as biotech companies awaiting FDA approvals or tech firms with regular product launches. By considering all trading days, IV Percentile avoids the distortions that can affect IV Rank.

For long-term premium sellers, IV Percentile is invaluable. It helps confirm when volatility is genuinely elevated across the entire year, rather than being skewed by a single event. This reliability is crucial for strategies like short strangles or iron condors, where confidence in the costliness of implied volatility is key to success.

Applying These Metrics to Your Trading

Grasping the concepts of IV Rank and IV Percentile becomes much more impactful when you apply them to your trades. These metrics help you gauge whether options premiums are relatively cheap or expensive compared to historical levels, which plays a big role in timing your strategies.

Using IV Metrics to Spot High-Premium Opportunities

If you're selling premiums, elevated volatility works in your favor. The general rule? Sell when IV Rank and IV Percentile are high, and buy when they're low. But what's considered "high" depends on your strategy and risk tolerance.

For more conservative approaches like covered calls and cash-secured puts, target an IV Rank above 30 and an IV Percentile over 40. If you're venturing into higher-risk strategies like iron condors or short strangles, aim for an IV Rank above 50 and an IV Percentile between 50 and 60. Using both metrics together - such as requiring IV Rank >30 and IV Percentile >50 - helps filter out trades skewed by single, unusual volatility spikes, which can distort IV Rank for extended periods.

Backtesting shows that setting these dual thresholds can improve win rates.

For option buyers, the logic flips. When both IV Rank and IV Percentile drop below 25–30, you're paying less for time value. This creates ideal entry points for strategies like long calls, puts, or debit spreads - especially if you anticipate volatility increasing soon.

Simplifying this process is key, and that's where technology steps in to save time and effort.

How ThetaEdge Simplifies Volatility Analysis

ThetaEdge takes the guesswork out of applying IV metrics. The platform automates the analysis, incorporating IV Rank and IV Percentile into its screening process to highlight opportunities for covered calls and cash-secured puts when volatility conditions match your strategy.

ThetaEdge takes the guesswork out of applying IV metrics. The platform automates the analysis, incorporating IV Rank and IV Percentile into its screening process to highlight opportunities for covered calls and cash-secured puts when volatility conditions match your strategy.

Instead of manually tracking IV metrics across multiple stocks, ThetaEdge uses its Conviction Score algorithm to combine IV Rank, IV Percentile, realized volatility, and market trends into a single actionable metric. This allows you to quickly pinpoint the best risk-adjusted premium opportunities in your portfolio at any given moment.

By connecting to over 80 brokerages with read-only access, ThetaEdge analyzes your actual holdings and sends daily AI-generated opportunity digests via email. When a covered call expires, the platform identifies the next opportunity based on current volatility conditions - making premium selection far easier.

For those who want to go deeper, ThetaEdge also offers portfolio-level Greeks and supports multi-leg strategies, all framed with a focus on volatility. You stay in full control of your decisions, but with the added benefit of advanced analysis to help you time premium sales and choose strikes that balance risk and reward effectively.

Choosing the Right Metric for Your Strategy

Selecting the right metric for your trading goals requires aligning it with your strategy and the current market environment.

Neither IV Rank nor IV Percentile is inherently better - they serve different purposes. IV Rank reacts faster to absolute changes in volatility, making it a handy tool for identifying quick signals in stable markets. On the other hand, IV Percentile provides a more statistically balanced view, especially in the aftermath of volatility spikes, which can skew IV Rank over longer periods.

For strategies focused on income generation, such as iron condors or short strangles, an IV Percentile above 70–80% often signals you're selling premium at the higher end of historical volatility levels. If your goal is to profit from rising volatility, aim for trades with low IV levels - both metrics at or below 30 - so you can minimize time value costs.

A thoughtful approach involves using both metrics together. For instance, setting criteria like an IV Rank above 30 and an IV Percentile above 50 before selling premium can help filter out trades skewed by one-off volatility events. When the two metrics diverge significantly - such as an IV Rank of 22% paired with an IV Percentile of 78% - this usually reflects a recent volatility spike compressing the rank calculation. In such scenarios, it’s better to rely on the percentile for making trade decisions. As FlashAlpha puts it:

Use percentile for decisions. Use rank for quick communication.

FAQs

Why do IV Rank and IV Percentile sometimes disagree?

Implied Volatility (IV) Rank and IV Percentile can sometimes give conflicting signals because they each assess implied volatility in distinct ways. IV Rank measures how the current IV stacks up against its 52-week range, which means it's heavily influenced by extreme highs or lows in that range. On the other hand, IV Percentile calculates the percentage of trading days in the past year where IV was lower than it is now, providing a steadier perspective. This divergence often becomes noticeable after sudden volatility spikes, as those events can skew IV Rank while having less impact on IV Percentile.

What IV Rank/IV Percentile levels are “high” or “low” for my strategy?

When the IV Rank or IV Percentile climbs above 70-80%, it signals that implied volatility is near its highest levels from the past year. This often results in pricier options premiums and hints at potential market uncertainty. On the flip side, when these metrics drop below 20-30%, volatility is near its lows, making premiums more affordable.

For traders, these thresholds serve as a guide. High implied volatility can present opportunities to sell options, as premiums are expensive. Conversely, low volatility might encourage buying or holding, depending on the strategy at play.

How can I use both metrics to avoid false signals after a volatility spike?

When dealing with a volatility spike, relying solely on one metric can lead to misleading conclusions. That’s why using both IV Rank and IV Percentile together is a smarter approach.

IV Rank measures where the current implied volatility (IV) sits within its 52-week range. While useful, it can sometimes be distorted by extreme outliers. On the other hand, IV Percentile calculates the percentage of days over the past year when IV was lower than today’s level. Unlike IV Rank, it isn’t swayed by sudden volatility spikes.

By combining these two metrics, you can better assess whether volatility is genuinely high or just experiencing a temporary surge. This dual approach provides a clearer picture, helping you make more informed decisions about trade timing.