Portfolio Greeks and Cash-Secured Puts Explained

Combine cash-secured puts with portfolio Greeks (delta, theta, gamma, vega) to earn steady retirement income while managing risk.

Managing a retirement portfolio can feel complex, but combining portfolio Greeks with cash-secured puts simplifies the process while generating steady income. Here’s the key idea:

- Cash-Secured Puts: You sell a put option, collect a premium upfront, and hold enough cash to buy the stock if needed. This strategy works best when you're comfortable owning the stock at the agreed price.

- Portfolio Greeks: Metrics like Delta, Theta, and Gamma help you measure risk, income potential, and market sensitivity across your portfolio, keeping your strategy on track.

By using these tools together, you can manage risk, define your income goals, and make informed adjustments. For example, the CBOE PutWrite Index, which tracks put-selling strategies, delivered an annualized return of 9.54% from 1986 to 2018 with lower volatility than the S&P 500. Even during downturns like 2022, it outperformed by limiting losses.

The secret lies in understanding how Greeks impact your trades and aggregating them across your portfolio to maintain balance. Let’s break down how these elements work and how they can help you achieve consistent income in retirement.

Understanding Cash-Secured Puts

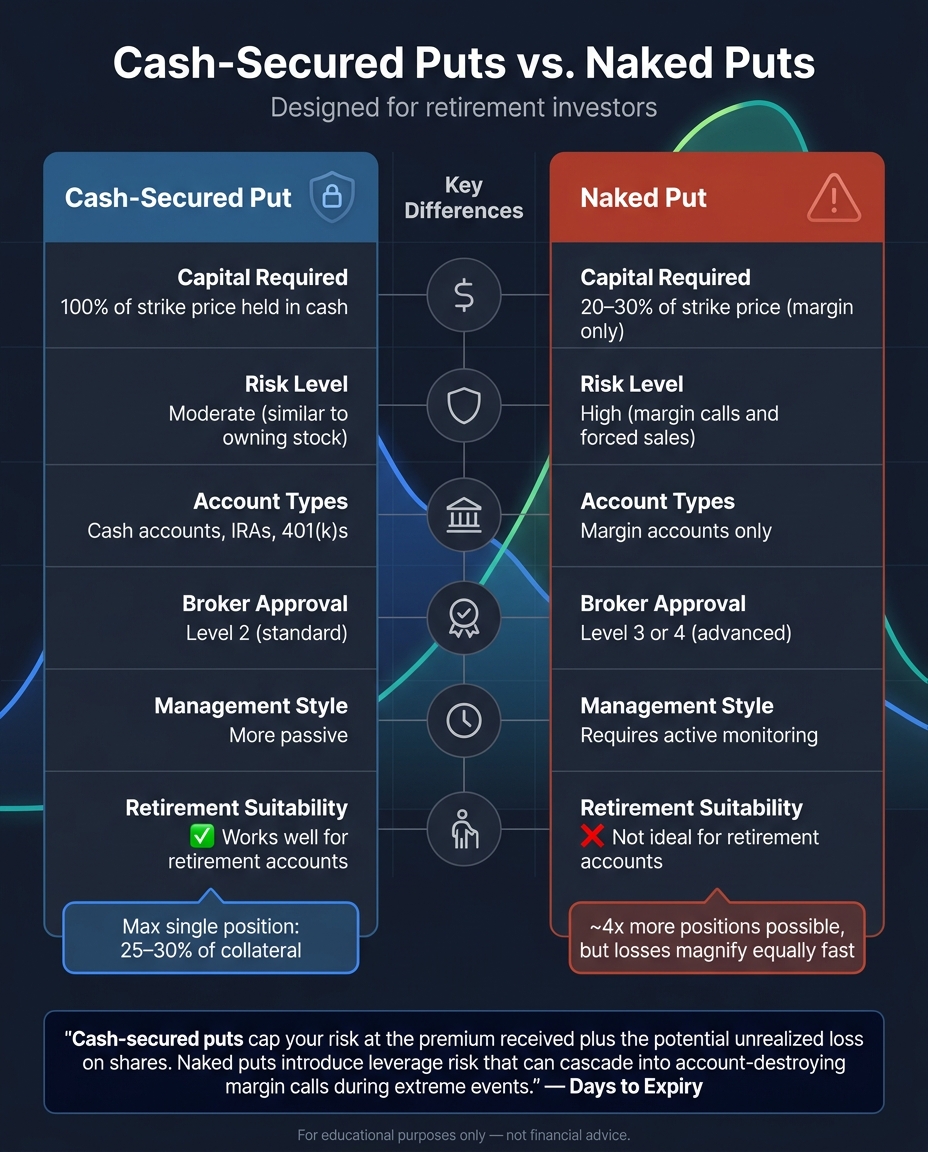

Cash-Secured Puts vs. Naked Puts: Key Differences for Retirement Investors

What Are Cash-Secured Puts?

A cash-secured put is an options strategy where you sell a put option while holding enough cash to buy the stock if you're assigned. In return, you collect a premium upfront - money that's yours to keep no matter how the trade plays out.

Here's how it works: if the stock stays above your strike price when the option expires, the option becomes worthless, and you pocket the premium. But if the stock falls below the strike price, you’ll need to buy the shares at that price using the cash you set aside. You can calculate risk for cash-secured puts by determining your breakeven point, which is the strike price minus the premium you received. For instance, selling a $170 strike put for a $7.77 premium means your breakeven is $162.23 per share. Plus, as the option gets closer to expiration, its value drops due to theta decay, which can further boost your income potential.

Benefits and Risks of Cash-Secured Puts

One of the main advantages is the immediate income you earn from the premium. If you're assigned, you end up buying a stock you already wanted to own, and the premium effectively lowers your purchase cost.

For retirement portfolios, this strategy can make your cash work harder. Reserved funds can earn returns in T-Bills or money market accounts while you aim for monthly income ranging from $500 to $1,500 per $100,000 of capital.

However, there are trade-offs. Your profit is limited to the premium, so if the stock price skyrockets, you won't benefit from the full upside. On the flip side, a sharp drop in the stock price could leave you buying shares at a price much higher than their market value. As a general rule of thumb:

"Never sell a put on a stock you wouldn't be thrilled to own at the strike price. That's the entire safety net." - Mike Thornton, Founder, The Multiplier

To manage risk, it's wise to avoid allocating more than 25% to 30% of your collateral to a single cash-secured put position.

Cash-Secured Puts vs. Naked Puts

A naked put differs because it doesn’t involve setting aside cash for potential stock purchases. Instead, it relies on margin, which typically requires only 20–30% of the strike price. While this allows for greater leverage, it also introduces higher risks.

Here’s a comparison of the two approaches:

| Factor | Cash-Secured Put | Naked Put |

|---|---|---|

| Capital Required | 100% of strike price in cash | 20–30% of strike price (margin) |

| Risk Level | Moderate (similar to owning stock) | High (margin calls and forced sales) |

| Account Types | Cash accounts, IRAs, 401(k)s | Margin accounts only |

| Broker Approval | Level 2 (standard) | Level 3 or 4 (advanced) |

| Management Style | More passive | Requires active monitoring |

| Retirement Suitability | Works well for retirement accounts | Not ideal |

For those managing retirement savings, cash-secured puts are often the safer choice. As noted:

"Cash-secured puts cap your risk at the premium received plus the potential unrealized loss on shares. Naked puts introduce leverage risk that can cascade into account-destroying margin calls during extreme events." - Days to Expiry

While naked puts let you open about four times as many positions on the same account size due to leverage, that leverage can magnify losses just as fast.

sbb-itb-a9ac3c2

Portfolio Greeks: Core Metrics for Options Analysis

Greeks help explain how an option's price reacts to various factors. For cash-secured put sellers, understanding these metrics can mean the difference between a well-managed strategy and unexpected losses.

Key Greeks Explained

Each Greek measures a distinct aspect of risk or reward. Here's how they apply to put sellers:

| Greek | What It Measures | Impact on Put Sellers |

|---|---|---|

| Delta | Price change per $1 move in the stock | Indicates directional exposure and assignment probability |

| Theta | Daily time decay | Primary source of income, collected daily |

| Gamma | Rate of change in delta | Increases risk near expiration, working against sellers |

| Vega | Sensitivity to implied volatility | Short vega benefits from falling IV but suffers when IV spikes |

| Rho | Sensitivity to interest rate changes | Minimal effect on short-term positions (30–45 DTE) |

"Theta is the engine - reliable income from 45 to 21 DTE. Delta is the steering wheel - strike selection at 0.20–0.30 delta. Vega is the weather - sell in elevated IV for structural edge. Gamma is the cliff - benign above 21 DTE, destructive in the final week." - ThetaLoop Research

Gamma deserves special attention. As expiration approaches, gamma risk intensifies. At just 1 day to expiration, gamma is about 7.8 times larger than at 60 DTE. For instance, a $1 stock drop close to expiration can significantly amplify losses. This is why seasoned sellers often close or roll their positions well before the final week.

Next, let’s explore how these Greeks influence your cash-secured put strategy.

How Greeks Affect Cash-Secured Puts

When selling cash-secured puts, these Greeks directly impact your risk and return. For those seeking stability in a retirement portfolio, leveraging these metrics can refine your strategy. You can even use Thetix for AI-powered portfolio analysis to see how these Greeks shift in real-time.

Delta reflects your bullish stance as a put seller. A negative delta essentially means you're betting the stock price will remain above your strike price. As a practical tool, delta also serves as a probability indicator: for example, a 20-delta put suggests a 20% chance the option will be assigned.

Theta drives income by eroding the option's value daily. Most of this decay happens as expiration nears. For example, with a $2.00 at-the-money option opened at 45 DTE, about 60.5% of the total decay occurs between 45 and 7 DTE, while the remaining 39.5% is compressed into the final week. This highlights the importance of managing gamma risk early to protect your gains.

Vega introduces an unpredictable element. As a put seller, you're short vega, which means rising implied volatility can hurt your position. This creates a "double blow": when a stock drops, implied volatility often spikes, compounding losses. For instance, imagine Apple (AAPL) trading at $255, and you sell a $240 strike put (20-delta) for $2.43. If AAPL falls $15 and IV rises by 10 points, the position could suffer a combined loss of approximately $516, factoring in delta, gamma, vega, and theta effects. That’s more than double the initial premium collected. This scenario emphasizes the value of selling puts when IV Rank is above 50%, allowing you to collect higher premiums and potentially profit when volatility normalizes.

Understanding these metrics is essential for navigating risks and optimizing returns in your cash-secured put strategy.

Managing Portfolio Greeks Across Multiple Positions

After examining individual Greeks, the next step is to combine them to evaluate your total portfolio risk. While tracking Greeks for each position offers useful insights, effective risk management depends on understanding the aggregate exposure - the sum of Greek values across all open positions.

Aggregating Greeks Across Positions

For retirement-focused portfolios, understanding aggregated Greeks is key to balancing income goals with risk management. Calculating portfolio Greeks is straightforward: sum up each Greek across all positions, and for delta, multiply by the standard contract size (typically 100 shares). To get a clearer picture of your dollar risk, apply dollar-weighted delta by multiplying each position's delta by the stock's price. This adjustment is crucial because a short put on a $500 stock exposes you to significantly more capital risk than one on a $50 stock, even if their deltas are identical.

Here’s an example of a three-position portfolio after aggregating the Greeks:

| Position | Delta (×100) | Theta (Daily) | Gamma | Vega |

|---|---|---|---|---|

| Short 1 AAPL Put | +30 | +$8 | −1.1 | −$12 |

| Short 1 SPY Put | +25 | +$12 | −0.8 | −$15 |

| Long 1 MSFT Put (Hedge) | −40 | −$14 | +3.6 | +$32 |

| Portfolio Total | +15 | +$6 | +1.7 | +$5 |

In this scenario, the portfolio is close to delta-neutral, generating $6 daily in theta decay. The long MSFT put hedge offsets much of the negative gamma and vega from the short positions. Without aggregating Greeks, such balances - or imbalances - might go unnoticed.

However, keep in mind that during market stress, stocks that typically behave independently can begin to move together. For instance, a portfolio spread across tech stocks like AAPL, NVDA, and CRM may seem diversified, but a sector-wide downturn could cause your Greeks to shift dramatically. This could transform what looks like a balanced portfolio into a concentrated directional bet.

Aggregating Greeks not only reveals your overall risk but also helps you make informed adjustments to improve portfolio performance.

Using Greeks to Improve Portfolio Performance

Tracking your aggregated Greek values allows you to adjust positions proactively, aligning them with your risk tolerance and income targets. Regular rebalancing ensures your portfolio stays within your desired Greek levels. For example, price movements can alter your net delta, requiring adjustments to maintain your target exposure. Many professional risk managers recommend limiting single-stock positions to 5% and sector exposure to 25% of the portfolio. If your net delta becomes overly positive, you might close bullish positions or add a small hedge with negative delta.

Maintaining a net positive theta is also important for consistent income. If long positions dominate or multiple contracts approach expiration at the same time, your daily income from time decay can quickly diminish. To avoid this, stagger your expirations by entering new positions gradually as older ones near 21 days to expiration. This approach smooths out theta earnings and reduces income volatility.

Gamma risk deserves special attention, particularly as expiration dates approach. Gamma becomes more pronounced near expiration, meaning your portfolio’s risk profile can shift dramatically in a short period. Managing trades when profits reach 50% or when 21 days remain until expiration helps keep the balance between risk and theta in check.

Tools like ThetaEdge can assist by providing portfolio-level Greek analysis, helping you monitor aggregated exposure and make adjustments before risks exceed your targets. These platforms simplify the process, ensuring you stay ahead of potential portfolio imbalances.

Using Portfolio Greeks to Manage Retirement Portfolio Risk

Risk Management with Portfolio Greeks

Retirement portfolios demand a more cautious approach compared to aggressive trading accounts. By setting conservative Greek thresholds, you can protect your long-term capital and maintain a steady income stream. These thresholds act as a safety net, helping you avoid scenarios where a single bad week wipes out months of premium income.

| Risk Metric | Retirement Threshold |

|---|---|

| Delta (per position) | Target range: 0.15–0.20; avoid exceeding 0.30 |

| Max Position Size | Limit to 5% of total portfolio per single stock |

| Sector Concentration | No more than 25% of portfolio in a single sector |

| Gamma Management | Stick to a 21 DTE exit strategy to manage gamma risk |

| Vega Management | Enter positions when IV Rank > 50% |

| Liquidity Reserve | Maintain 70–80% of portfolio in cash |

To minimize assignment risk, aim for a delta range of 0.15–0.20 per position. This usually means placing strikes about 10–15% out of the money. For example, a 16-delta put - often referred to as a "one standard deviation" move - historically finishes in the money only about 5% of the time, thanks to the volatility risk premium embedded in options pricing.

Vega management is especially critical for retirement accounts. When stocks drop, implied volatility tends to spike, intensifying losses. Selling puts when the IV Rank exceeds 50% allows you to collect higher premiums upfront and take advantage of eventual volatility mean-reversion.

Given the complexity of tracking these metrics across multiple positions, automated tools can be a game-changer.

How ThetaEdge Supports Portfolio Analysis

Managing Greeks across a multi-position retirement portfolio can feel overwhelming. Delta, theta, gamma, and vega values fluctuate daily due to price changes, time decay, and shifts in volatility. Missing a threshold could expose you to gamma acceleration, where a small market dip snowballs into a larger loss.

ThetaEdge simplifies this by aggregating real-time Greek data from all your positions. It connects to over 80 brokerages - including Schwab, Fidelity, Interactive Brokers, and Robinhood - via read-only access. This setup ensures your live portfolio data is secure since the platform cannot execute trades. For retirement investors wary of third-party tools, this read-only design provides peace of mind.

The platform also offers features like Position Monitoring, which alerts you when a cash-secured put hits a profit target or when assignment risk increases. Additionally, its roll analysis tool identifies alternative strikes and expirations, complete with a credit or debit breakdown. This gives you actionable choices rather than vague warnings.

"The research that would take hours of manual work, delivered in minutes across your entire portfolio." - ThetaEdge

For self-directed retirement investors juggling multiple cash-secured puts, ThetaEdge provides the clarity needed to stay within your Greek thresholds. By addressing small imbalances early, you can prevent them from escalating into larger issues.

Conclusion

Portfolio Greeks turn cash-secured put selling into a structured and repeatable strategy. Delta helps estimate assignment probabilities, theta reveals your daily income potential, gamma highlights when risk might escalate, and vega measures your sensitivity to volatility changes.

From 2020 to 2025, systematic cash-secured put strategies delivered an 18.3% average annual return on cash at risk, with a maximum drawdown of just 8.2% during the 2022 technology downturn. These results highlight the effectiveness of a disciplined approach informed by Greeks.

Generating steady retirement income requires careful attention to Greek thresholds, diversification across sectors, and disciplined position sizing. Maintaining a cash reserve of 10–15% of total assets, aiming for a 0.20 delta, and staggering expirations are key practices that can help avoid costly mistakes while ensuring consistent income.

For those juggling multiple positions, having a centralized tool can make a world of difference. ThetaEdge simplifies the process by consolidating your portfolio Greeks in real time, identifying cash-secured put opportunities tailored to your holdings, and alerting you when thresholds shift. With connections to 80+ brokerages via read-only access, it keeps your data secure while providing actionable insights. While the platform handles the analysis, the final call remains in your hands.

FAQs

What delta should I target when selling cash-secured puts in retirement?

When selling cash-secured puts during retirement, targeting a delta between 10 and 20 is a popular approach. A delta closer to 10 means there's a lower likelihood of the option being assigned, but it still allows you to collect premium income. This range strikes a balance between minimizing assignment risk and maintaining income potential, which is why it's often favored for managing retirement portfolios.

When should I close or roll a cash-secured put to control gamma risk?

When the delta of a cash-secured put approaches 0.30 or higher, it signals a growing chance of the option being assigned. This also reflects rising gamma, which peaks when options are at-the-money. Keeping an eye on delta can help you manage this risk effectively.

To address the situation, consider rolling the position. This involves moving to a later expiration date or adjusting the strike price. Such a move can help lower your exposure, particularly during periods of high volatility or when significant price changes could disrupt your portfolio's balance.

How do I track my total portfolio Greeks across multiple put positions?

To get a clear picture of your portfolio's overall Greeks, consider using portfolio-level analysis. This approach consolidates essential metrics like Delta, Theta, Gamma, and Vega into a single view. Tools such as the Portfolio Greeks Dashboard from ThetaEdge can sync with your brokerage account, offering real-time insights into your total risk exposure. By aggregating these Greeks, you can better gauge how your options portfolio reacts to market shifts, time decay, and changes in volatility, helping you make more informed decisions.