5 Factors to Consider When Picking Strike Prices

How to choose covered call strike prices: balance delta, volatility, income goals, assignment risk, and market outlook to fit your strategy.

When using a covered call strategy, choosing the right strike price is crucial - it determines your income, upside potential, and the chance of losing your shares. Here's what you need to know:

- Risk vs. Reward: Closer strikes offer higher premiums but increase assignment risk. Farther strikes reduce income but preserve upside.

- Delta as a Guide: Delta helps estimate assignment probability. For example, a 0.30 delta means a 30% chance of assignment and a 70% chance of keeping your shares.

- Volatility Matters: High-volatility stocks yield larger premiums but require lower deltas for reduced assignment risk. Low-volatility stocks need higher deltas for meaningful income.

- Income Goals: Decide if you prioritize income, upside potential, or holding shares. A 30-delta strike often balances income and retention.

- Market Outlook: Bullish? Choose out-of-the-money strikes. Neutral? At-the-money strikes maximize premiums. Bearish? In-the-money strikes offer protection.

Key takeaway: Match your strike price to your goals, risk tolerance, and market view for better results. Using an options strategy planner can help you visualize these trade-offs before execution.

Strike Price Selection Guide: Delta Ranges, Premiums, and Assignment Risk by Strategy

1. Risk Tolerance

Risk/Reward Trade-offs

Figuring out how much risk you're comfortable with is the starting point for choosing strike prices that match your investment goals. The strike price you pick should reflect your risk appetite. For example:

- Conservative traders often aim for a delta around 0.20 (roughly a 20% chance of assignment).

- Balanced traders typically choose a delta between 0.20 and 0.30.

- Aggressive traders might go for a delta of 0.40 or higher to chase larger premiums.

The closer your strike price is to the current stock price, the higher the premium you'll collect - but this comes with a greater chance of assignment. On the other hand, choosing a strike price farther away lowers the premium but gives you more room for potential upside. This trade-off sets the foundation for how market conditions can further shape your strike price decisions.

Assignment Likelihood

Knowing the probability of your shares being called away is key to making smart choices. Here's a breakdown of how different strike price strategies align with various risk levels:

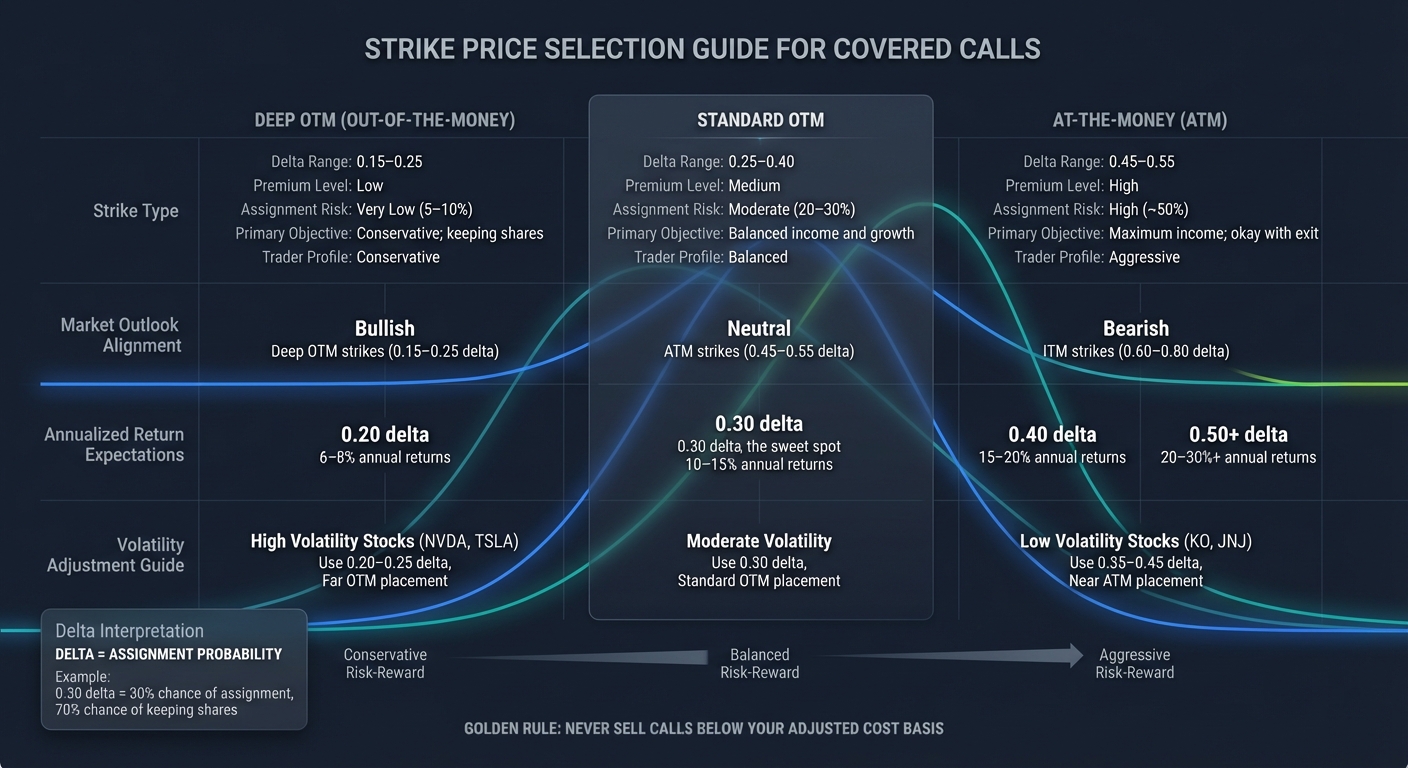

| Strike Type | Delta Range | Premium Level | Assignment Risk | Primary Objective |

|---|---|---|---|---|

| Deep OTM | 0.15–0.25 | Low | Very Low (5–10%) | Conservative; keeping shares |

| Standard OTM | 0.25–0.40 | Medium | Moderate (20–30%) | Balanced income and growth |

| At-the-Money | 0.45–0.55 | High | High (~50%) | Maximum income; okay with exit |

This table provides a snapshot of how strike prices can align with your risk profile. Once you've determined your comfort level, incorporating volatility measures can help you refine your strategy further.

One key rule applies no matter your risk level: never sell calls with a strike price below your adjusted cost basis (your purchase price minus any premiums you've already collected). Doing so guarantees a realized loss if you're assigned. This "golden rule" ensures you avoid turning a temporary paper loss into a permanent one.

To reduce the chances of routine assignments, consider using the 14-day ATR (Average True Range) multiplied by 1.5 to 2. Add this buffer to the current stock price to set a strike that accounts for typical price swings.

sbb-itb-a9ac3c2

2. Stock Volatility

Volatility Metrics

Once you understand how your risk tolerance affects strike price selection, adding volatility into the mix can refine your approach. Volatility plays a key role in determining both the premiums you can collect and the likelihood of assignment. Two key metrics to consider are Implied Volatility (IV), which reflects the market's expectations for future price swings, and Historical Volatility (HV), which shows how much the stock has fluctuated in the past. Additionally, the Average True Range (ATR) measures actual daily price movements, giving you a practical way to factor in normal fluctuations.

The ATR is particularly useful for strike placement. By multiplying the 14-day ATR by 1.5 to 2 and adding that buffer to the current stock price, you can identify strike prices that stay outside typical daily trading ranges. Another helpful tool is Bollinger Bands, which adjust to market volatility by expanding and contracting. Choosing strike prices just outside these bands can improve the odds of a successful trade. Together, these tools not only inform strike placement but also help shape your premium expectations. You can also use portfolio intelligence tools to analyze these trade-offs across your entire account.

Income Potential

Volatility directly impacts the premiums you can collect. Stocks with higher volatility, like NVDA or TSLA, offer larger premiums but require wider, lower-delta strikes (around 0.20–0.25) to reduce the chance of assignment. On the other hand, low-volatility stocks such as KO or JNJ yield smaller premiums, so closer strikes with higher deltas (0.35–0.45) are often necessary to generate meaningful income.

For instance, consider AMD trading at $155. Writing a 30-day call with a $160 strike at a 0.30 delta might yield a $3.50 premium. This setup provides a balance between income and a 5% buffer for potential upside. Historically, a 30-delta strike has delivered annualized yields of 10% to 15% in similar scenarios.

Here’s a quick breakdown of strategies based on stock volatility:

| Stock Volatility Type | Recommended Delta | Strike Placement | Key Outcome |

|---|---|---|---|

| High Volatility | 0.20–0.25 | Far OTM | Minimize assignment risk while capturing higher premiums |

| Moderate Volatility | 0.30 | Standard OTM | Strike a balance between income and growth potential |

| Low Volatility | 0.35–0.45 | Near ATM | Maximize premiums from stable price movement |

3. Income Goals

Once you’ve gauged your risk tolerance and grasped how volatility affects premiums, the next step is to align your strike price selection with your income objectives.

Risk/Reward Trade-offs

Your income goals directly influence the trade-offs you’ll make with potential capital gains. While higher premiums may seem appealing, they come at the cost of limiting your upside. As Mike Thornton from The Multiplier explains:

"Most people pick strikes by looking at the premium column and choosing the biggest number, but premium isn't free. It's what you get paid for capping your upside."

For example, a call option that pays 1% to 2% of your share value might require you to give up 5% to 10% in potential price appreciation.

Choosing the right strike price depends on your market outlook. If you’re feeling bullish, out-of-the-money (OTM) strikes allow for both premium income and potential stock price gains. If your stance is neutral, at-the-money (ATM) strikes maximize premium collection through time decay. And if you’re bearish or planning to exit, in-the-money (ITM) strikes provide more downside protection and facilitate a smoother exit. This balance plays a crucial role in determining the annualized returns you can achieve with a covered call strategy.

Income Potential

The delta you select significantly affects your potential annualized returns. A conservative approach with 0.20-delta strikes tends to deliver returns in the 6% to 8% range annually. A more balanced 0.30-delta strategy typically generates 10% to 15%, while a more aggressive 0.40-delta approach might yield 15% to 20%. For those willing to take on higher risk, 0.50-delta or higher ATM strikes could potentially achieve returns of 20% to 30% or more.

QuantWheel highlights the 30-delta strike as a sweet spot for many traders:

"The 30-delta strike offers the best balance between premium collection and keeping your shares for most wheel strategy traders."

To help refine your approach, tools like ThetaEdge offer portfolio-aware options analysis, making it easier to assess risk/reward trade-offs and ensure your strike price choices align with your income goals.

4. Market Outlook and Stock Forecast

Market Sentiment Alignment

Choosing the right delta for your stock forecast depends on your market outlook. If you're strongly bullish, deep out-of-the-money (OTM) strikes with a delta of 0.15–0.25 are a popular choice. These strikes protect your upside potential while keeping assignment risk low, typically around 5% to 10%. On the other hand, a bearish perspective might lead you to in-the-money (ITM) strikes with a delta of 0.60–0.80, which offer downside protection and can facilitate an exit.

For those with a mildly bullish or neutral view, standard OTM strikes in the 0.25–0.40 delta range strike a balance between income generation and growth potential. Meanwhile, a neutral outlook often pairs well with at-the-money (ATM) strikes, which fall in the 0.45–0.55 delta range and focus on maximizing premium income. If your outlook leans bearish, ITM strikes remain the go-to for added downside protection and strategic exits.

Once your sentiment is clear, you can refine your strike selection by factoring in technical metrics.

Volatility Metrics

Market volatility adds another layer to consider. As discussed earlier, the IV Rank is a key measure here. Higher volatility typically means higher option premiums, but it also requires adjusting your strikes further OTM (lower delta) to maintain your desired probability of keeping shares.

To maximize your strategy, consider selling calls just below key resistance levels. This approach takes advantage of price stalling or potential reversals. For example, a 30-delta call has about a 30% chance of finishing ITM, leaving you with a 70% chance of retaining your shares. By combining these technical insights with your market sentiment and risk tolerance, you can fine-tune your strike selection to align with your overall goals.

5. Probability of Assignment and Willingness to Sell

Assignment Likelihood

Understanding the probability of assignment is a key factor when aligning your covered call strategy with your income goals. This is where delta comes into play. Delta serves as a reliable estimate of assignment probability. For instance, a call option with a 0.30 delta has about a 30% chance of ending in-the-money at expiration, leaving a 70% chance that you'll keep your shares. This makes delta a practical tool for gauging assignment risk.

Many covered call traders gravitate toward the 30-delta strike. Why? It strikes a balance between earning a meaningful premium and maintaining a solid chance of holding onto shares for long-term growth. For those who prefer a more conservative approach, aiming for strikes with a delta between 0.15 and 0.25 reduces assignment risk. On the other hand, if your goal is to exit or prioritize income, strikes with a delta of 0.40 to 0.50 offer higher premiums but come with a 40%–50% assignment probability.

Risk/Reward Trade-offs

Your willingness to sell your shares plays a huge role in strike selection. If holding onto your shares is a priority, focus on out-of-the-money strikes with lower assignment risk. However, if you're ready to exit or want to maximize income, at-the-money or in-the-money strikes may better suit your needs.

"Never sell a covered call on shares you're not willing to part with." - QuantWheel

Income Potential

The income you collect from premiums is directly tied to assignment probability. Higher-delta strikes, which are closer to at-the-money, generate larger premiums but also increase the likelihood of your shares being called away. For example, consider an investor holding 100 AMD shares with a $150 cost basis. They sell a 30-delta $160 strike call when AMD is trading at $155. This trade collects $3.50 per share in premium, totaling $350, and offers a 70% chance of retaining the shares. If the shares are assigned, the investor would realize a total profit of $1,350, including a $10 capital gain per share plus the premium.

To manage risk and secure profits, many traders close their covered calls once they achieve 50% of the maximum profit. This approach helps lock in gains, free up capital, and reduce the risk of assignment.

Advanced tools like ThetaEdge can make this process even smoother. These tools provide detailed portfolio analytics, helping you assess assignment probabilities and align your strike prices with your broader investment strategy. By integrating these insights, you can fine-tune your covered call approach for better results.

Comparison Table

This table breaks down the differences between ITM (In-The-Money), ATM (At-The-Money), and OTM (Out-Of-The-Money) strikes, focusing on key factors like delta ranges, premium income, downside protection, upside potential, and assignment probabilities.

| Strike Type | Delta Range | Premium Income | Downside Protection | Upside Potential | Assignment Probability |

|---|---|---|---|---|---|

| ITM | 0.55 to 1.00 | Highest (Intrinsic + Extrinsic) | High (Intrinsic cushion) | Limited to the strike price | High (>50%) |

| ATM | ~0.50 | High (Max Extrinsic) | None | Limited to the strike price | Moderate (~50%) |

| OTM | 0.01 to 0.45 | Lowest (Extrinsic only) | None | Greater (Up to strike price) | Low (<50%) |

For instance, consider adjusting the strike price on AMD from an ITM $150 to an OTM $165. This shift dramatically impacts the premium you earn and the likelihood of assignment. ITM strikes deliver the highest premium and a built-in cushion (intrinsic value), but they cap your upside. ATM strikes focus on maximizing extrinsic value, offering moderate assignment risk. Meanwhile, OTM strikes provide more room for growth, albeit with lower premiums and reduced assignment probabilities. The choice boils down to your priorities: income, protection, or growth - and your willingness to let go of your shares.

Tools like ThetaEdge simplify this decision-making process by offering portfolio-specific comparisons. They highlight risk/reward metrics and assignment probabilities tailored to your holdings, making it easier to weigh the trade-offs and choose strikes that fit your investment strategy.

Conclusion

Choosing the right strike price involves balancing factors like risk tolerance, market volatility, income targets, and the likelihood of assignment. These elements work together to create a strategy that aligns with your specific objectives. For instance, if keeping your shares is a priority, you might lean toward 20- to 30-delta options (out-of-the-money). On the other hand, if generating higher income takes precedence, 50+ delta strikes (at-the-money or in-the-money) could be more appropriate. Many traders gravitate toward the 30-delta strike due to its mix of reasonable premium and a lower chance of losing shares, with historical annual yields often ranging between 10% and 15%.

It’s also crucial to avoid selling calls below your adjusted cost basis unless you’re prepared to accept a loss.

These strategies are supported by tools designed to make the process more efficient. For example, ThetaEdge offers portfolio-aware analysis customized to your holdings. The platform highlights covered-call opportunities by presenting detailed risk and reward metrics - such as strike price, expiration, premium, assignment probability, and breakeven - making it easier to evaluate your options. Additionally, the Thetix AI assistant provides answers to plain-language questions about your portfolio, using live market data to inform decisions. Importantly, ThetaEdge doesn’t execute trades, ensuring you maintain complete control. With features like daily AI-generated opportunity reports, income tracking dashboards, and tools for managing roll strategies, ThetaEdge equips you with the insights you need to make informed decisions while staying in charge.

FAQs

How do I pick a strike if I don’t want to lose my shares?

When selecting a strike price, aim for a balance between generating income and reducing the chance of losing your shares. If the strike is too close to the stock's current price, a sudden rally could result in your shares being called away. On the other hand, strikes set too far out-of-the-money might not bring in enough premium to make the trade worthwhile. A practical approach is to target a strike price with a delta in the 30-40 range, ensuring it’s also above your cost basis. This strategy helps lower the risk of assignment while still providing a reasonable income opportunity.

Which volatility number should I use to choose a strike?

When choosing implied volatility, aim for levels that match both the current market environment and your comfort with risk. This is typically expressed through the option's delta or its out-of-the-money (OTM) percentage. For example:

- A delta in the 30-40 range is often used in more cautious strategies.

- For LEAPS (Long-Term Equity Anticipation Securities), a higher delta, such as 0.75 to 0.85, might be more suitable.

These figures incorporate both the market's volatility expectations and the time value of the option, helping you align your approach with your goals.

When should I close a covered call early?

When managing a covered call, closing it early can sometimes make sense. This approach allows you to lock in profits or reduce exposure to potential risks if market conditions take an unexpected turn. For instance, if your call option has gained most of its value before expiration, closing it early lets you secure those gains without waiting for the contract to expire.

Similarly, if the market shifts unfavorably - perhaps the stock price is climbing quickly toward your strike price - you might choose to close the position to avoid having your shares called away. This flexibility allows you to adjust your strategy as needed, whether to protect gains or respond to new developments.

Ultimately, the decision to close early should align with your personal risk tolerance, profit goals, and how you see the market evolving. Balancing these factors will help you determine the right move for your portfolio.