When to Use Straddles vs Strangles

Compare straddles vs strangles: trade-offs in cost, breakeven, and when to buy or sell based on implied volatility and risk.

Straddles and strangles are options strategies designed to profit from significant price movements regardless of direction. The key difference lies in their structure:

- Straddles use at-the-money (ATM) options with the same strike price and are ideal when moderate implied volatility (IV) and significant price moves are expected. They have higher upfront costs but require smaller movements to break even.

- Strangles use out-of-the-money (OTM) options with different strike prices, offering lower upfront costs but needing larger price swings to turn profitable. They work best in high IV conditions.

Both strategies can be used for buying (long) or selling (short), depending on your outlook for price movement and volatility. Long positions benefit from volatility increases, while short positions profit from stability and time decay.

Quick Comparison

| Feature | Straddle | Strangle |

|---|---|---|

| Strike Prices | Same (ATM) | Different (OTM) |

| Premium Cost | Higher ($500–$2,000) | Lower ($200–$1,000) |

| Breakeven Range | Narrow | Wider |

| Best For | Moderate IV, smaller moves | High IV, larger moves |

| Risk (Short) | Unlimited | Unlimited |

Your choice depends on the market's volatility, your capital, and your risk tolerance. Each strategy has unique trade-offs that align with different market conditions.

Straddles vs Strangles: Options Strategy Comparison Chart

What Are Straddles?

A straddle is a trading strategy designed to take advantage of significant price movement in either direction. It involves using both a call and a put option on the same asset, with identical strike prices and expiration dates. Typically, these options are at-the-money (ATM), meaning their strike price aligns with the asset's current market value. The beauty of this approach lies in its neutrality - profits come from substantial price swings, regardless of direction.

Straddles come in two variations. A long straddle involves buying both the call and the put (a net debit trade) to profit from big moves in price. On the other hand, a short straddle involves selling both options (a net credit trade), aiming to benefit from a stable market where prices stay within a narrow range. The combined delta of the call and put in a straddle is close to zero, reflecting its lack of directional bias.

Straddle Construction

To create a long straddle, you buy one ATM call and one ATM put with matching strike prices and expiration dates. The total premium paid represents your maximum loss. In contrast, a short straddle involves selling one ATM call and one ATM put, where the premium collected upfront is the maximum possible profit. However, the risk for a short straddle is theoretically unlimited.

Breakeven points for a straddle are calculated as follows:

- Upper breakeven: Strike price + total premium

- Lower breakeven: Strike price - total premium

For example, if you purchase a $100 strike straddle for a $10 combined premium, your breakeven prices are $110 on the upside and $90 on the downside. Any movement beyond these points results in profit.

When to Buy Straddles

Long straddles are ideal when you expect a significant price movement, but you're unsure of the direction. Events like earnings reports, FDA approvals, Federal Reserve decisions, or major legal rulings often create these opportunities. Timing is critical here - entering when implied volatility (IV) is low, ideally below the 70th percentile, helps avoid overpaying for the options. For earnings plays, the best entry window is typically 14 to 30 days before the event.

Historical data from 2020 to 2024 highlights the effectiveness of long straddles in certain sectors. For example:

- Tech stocks like NVDA, AMD, and TSLA showed a 55% win rate.

- Utilities and consumer staples had a much lower success rate at just 28%.

"The straddle is the quintessential play for traders who expect a 'volatility breakout.'" - CBOE

One key risk with long straddles is IV crush, where implied volatility drops sharply after a major event. This can erode the value of both options, even if the stock moves. For instance, a 10-point drop in IV on a $100 stock with 30 days to expiration can impact the straddle's value as much as a $4.50 price move in the underlying asset. To mitigate this, many traders exit the position shortly after the event, especially if the anticipated move hasn't occurred.

While long straddles thrive on volatility, short straddles are better suited for calm, stable markets.

When to Sell Straddles

Short straddles generate profit when the underlying stock remains stable and IV declines. Here, the premium collected upfront decreases over time due to time decay (theta), and falling IV further reduces the options' value. The optimal time to sell a straddle is when IV is elevated - above the 50th percentile and ideally at least 5 points higher than historical volatility.

Experienced traders often aim to lock in profits once they've captured 50% to 70% of the maximum potential gain. Holding the position until expiration can expose the trade to late-stage gamma risk, where sudden price swings can turn a profitable trade into a loss. That said, short straddles carry significant risk: if the underlying asset makes a large move in either direction, losses can be unlimited.

| Strategy Component | Long Straddle | Short Straddle |

|---|---|---|

| Construction | Buy ATM Call + Buy ATM Put | Sell ATM Call + Sell ATM Put |

| Outlook | Anticipating significant movement | Expecting price stability |

| Max Profit | Unlimited | Limited to the premium received |

| Max Risk | Limited to the premium paid | Theoretically unlimited |

| Theta (Time) | Negative (value decreases daily) | Positive (value increases daily) |

| Vega (Volatility) | Positive (benefits from rising IV) | Negative (benefits from falling IV) |

sbb-itb-a9ac3c2

What Are Strangles?

A strangle is an options strategy that involves using a call and a put on the same asset. Both options share the same expiration date but have different strike prices. Unlike straddles, which use at-the-money (ATM) options, strangles rely on out-of-the-money (OTM) options. In this setup, the call strike is placed above the current market price, and the put strike is set below it.

This approach comes with much lower upfront costs. OTM options reduce the initial expense while still providing exposure to volatility. For example, consider a stock trading at $70. A straddle using the $70 strike might cost $2.80, but a strangle with a $68 put and a $72 call might only cost $1.40 - cutting the entry cost by half.

There are two main types of strangles. A long strangle involves purchasing both the OTM call and put, aiming to profit from significant price swings in either direction. On the other hand, a short strangle involves selling both options to collect a premium when the stock remains range-bound and volatility decreases. The tradeoff here is that while strangles are cheaper to enter, they require a larger price movement to reach profitability.

Strangle Construction

To create a long strangle, you buy one OTM call and one OTM put with the same expiration date but different strike prices. For a long strangle, the maximum loss is limited to the total premium paid. Conversely, a short strangle collects premium as its maximum profit but comes with unlimited risk.

The breakeven points for a strangle are calculated as follows:

- Upper breakeven: Call strike price + total premium paid

- Lower breakeven: Put strike price - total premium paid

Let’s look at an example. In January 2026, NVIDIA (NVDA) was trading at $900. A trader compared a straddle and a strangle ahead of earnings. The straddle, involving the $900 call and put, cost $90, with breakevens at $810 and $990. Meanwhile, the strangle, using a $950 call and an $850 put, cost $55, with breakevens at $795 and $1,005. While the strangle needed a larger price move to turn profitable, it reduced capital risk by 39% and was less affected by the post-earnings volatility crush.

When to Buy Strangles

Long strangles are particularly useful when significant price swings are anticipated. They are ideal for scenarios where the direction of the move is uncertain, but the magnitude is expected to be substantial. This makes them well-suited for events like FDA drug approvals, major product launches, or earnings announcements.

For instance, in June 2021, Biogen Inc. (BIIB) shares jumped over 38% in a single day after the FDA approved its Alzheimer’s drug, Aduhelm. A long strangle would have captured this dramatic move regardless of the outcome. Similarly, in October 2024, Tesla (TSLA) shares dropped 9% within 24 hours after unveiling its "Cybercab", allowing traders to profit from a sharp downward move despite the uncertainty.

"Strangles are particularly worthwhile during events or market conditions that typically generate significant price volatility." - Investopedia

The best time to enter earnings-related strangles is typically one to four weeks before the announcement. This allows traders to benefit from rising implied volatility. However, long strangles are highly sensitive to time decay. If the expected price movement doesn’t happen quickly, the position can lose value rapidly. Many traders close their long strangles immediately after the event to avoid losses from volatility crush and theta decay.

When to Sell Strangles

While long strangles thrive on volatility, short strangles are designed for steadier markets. This strategy works best when the underlying stock is expected to remain within a specific range with only moderate price movement. Short strangles profit from time decay and falling implied volatility. Traders often target stocks with implied volatility above the 67th percentile to maximize premium collection and benefit from volatility contraction.

For example, in 2025, a trader sold a 0.20-delta strangle on ARM Holdings by shorting a $90 put and a $140 call for the following month. This trade required $1,061 in buying power and offered a maximum return on capital of 51%, provided the stock stayed between the strikes. By choosing wider strikes, the trader increased the probability of profit compared to a short straddle, though the premium collected was lower upfront.

"When selling strangles, remember that your maximum profits are limited but your potential losses aren't. Experienced traders learn to respect the risk asymmetry." - Investopedia

Short strangles offer a broader safety range and a higher probability of success. Most traders aim to exit after capturing 50–70% of the potential profit to avoid the risks associated with sudden price movements, also known as gamma risk.

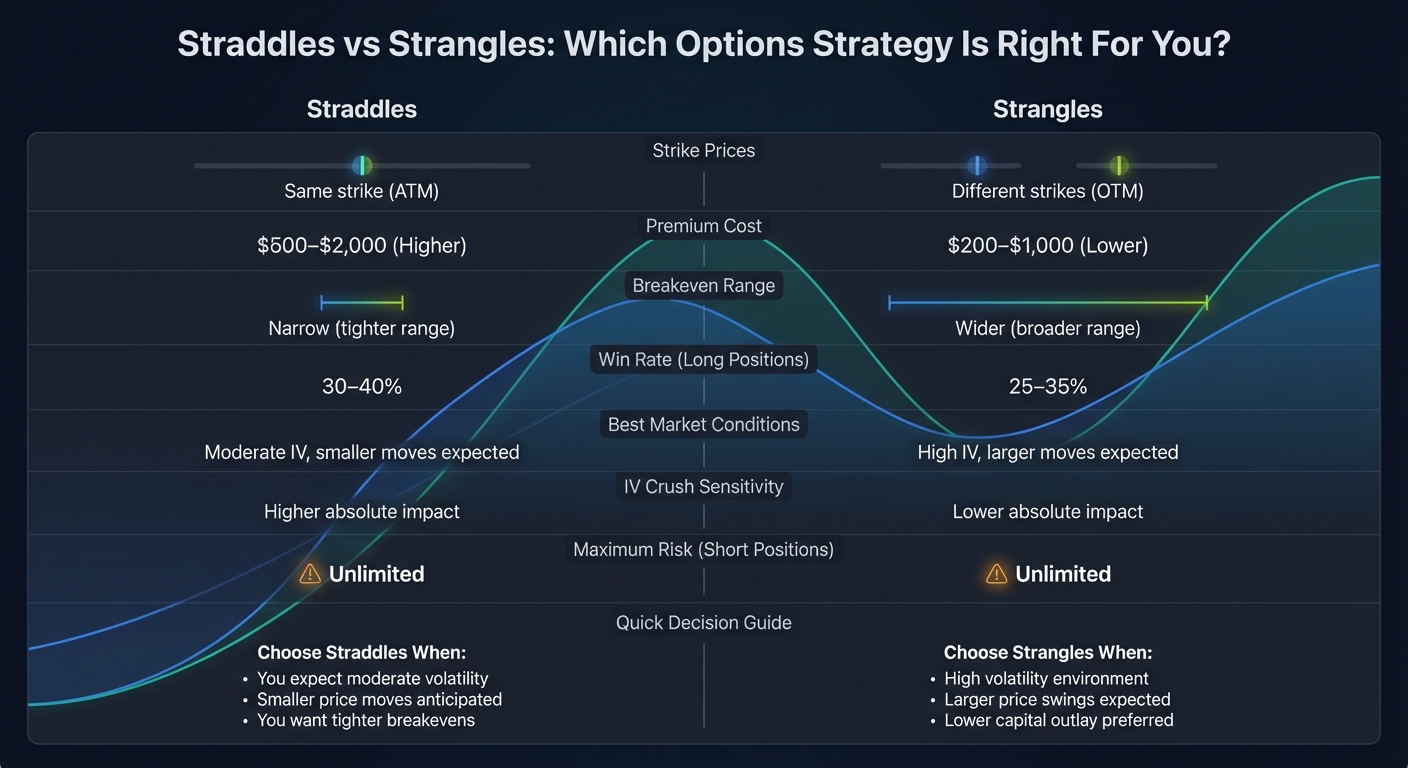

Straddles vs. Strangles: Key Differences

Straddles and strangles might seem similar at first glance, but the differences in their structure and cost make them suited for distinct scenarios. Straddles involve at-the-money (ATM) options with identical strike prices, resulting in higher premiums ranging from $500 to $2,000. These strategies require smaller price movements to become profitable. On the other hand, strangles use out-of-the-money (OTM) options with different strike prices. They come with lower premiums, typically $200 to $1,000, but demand larger price swings to generate returns. Choosing between the two depends on your outlook for volatility and your specific investment goals.

"The key difference is cost vs. probability: straddles cost more but require less movement; strangles cost less but need bigger moves to profit." - ApexVol Trading Team

When it comes to success rates, long straddles generally achieve a win rate of 30–40%, while long strangles hover slightly lower at 25–35%. This is due to the broader breakeven range associated with strangles. However, as options trader Sean Ryan explains, the expected value for both strategies often evens out over time: "Your probability of profit increases, but the amount you win when you are correct decreases". The table below provides a concise comparison of the two strategies for easy reference.

Side-by-Side Comparison

| Feature | Straddle | Strangle |

|---|---|---|

| Strike Prices | Same strike (ATM) | Different strikes (OTM) |

| Premium Cost | Higher ($500–$2,000) | Lower ($200–$1,000) |

| Breakeven Range | Narrow breakeven range | Wider/Further from current price |

| Win Rate (Long) | 30–40% | 25–35% |

| IV Crush Sensitivity | Higher absolute impact | Lower absolute impact |

| Best For | Moderate IV, significant move expected | High IV, massive move expected |

This comparison highlights how each strategy aligns with different market scenarios and risk profiles.

For those considering selling strategies, the dynamics shift. Short straddles collect higher premiums but depend on the stock price staying very close to the strike. In contrast, short strangles offer a wider margin for error but come with lower upfront returns. Many seasoned traders lean toward short strangles because the wider strike prices reduce delta hedging costs and require fewer adjustments. Just as timing matters for long positions, choosing the right selling strategy can make a significant difference in stable market conditions.

Choosing Based on Market Conditions

Deciding between straddles and strangles often comes down to understanding the market environment and how each strategy performs under specific conditions.

Volatility Levels

Implied volatility (IV) plays a key role in determining which approach makes the most sense. When IV is moderate, straddles can provide a sharper tool for trading the gap between market expectations and actual outcomes. Options trader Sean Ryan highlights their precision:

"Straddles are the purest way to trade the implied vs realized move. You get the right feedback, and the right time, and are able to adjust your trades accordingly".

Strangles, on the other hand, shine in periods of high IV spikes. For instance, during events like NVIDIA's earnings, strangles have been shown to reduce capital risk by up to 39% while limiting exposure to IV crush in absolute dollar terms. The QuantStrategy.io Team emphasizes this advantage:

"The Strangle is often preferred by traders who recognize [a stock's] tendency for large moves but wish to reduce capital outlay and hedge against an unexpected, smaller move".

Situations like pre-earnings announcements, where IV tends to spike, make strangles particularly appealing. Beyond volatility, though, factors like time decay and directional neutrality also influence performance.

Time Decay and Directional Neutrality

Both strategies aim to maintain delta neutrality, but they differ in how they handle time decay. Straddles experience faster erosion due to the higher theta of at-the-money options, which hold the most extrinsic value. This means premiums decay faster for buyers but also allow sellers to collect profits more quickly.

Strangles, using out-of-the-money options, face slower time decay since these options carry less premium from the start. This makes them more forgiving in markets that move sideways. For sellers, strangles offer a wider range where the stock can drift without requiring defensive adjustments. Professional traders often favor selling strangles because the looser delta management thresholds reduce transaction costs and the need for frequent portfolio rebalancing.

How ThetaEdge Can Help

Navigating the intricacies of volatility strategies demands a deep understanding of multiple factors - implied volatility, time decay, breakeven points, and probabilities. For self-directed investors, this can mean hours of painstaking research. ThetaEdge streamlines this process by delivering insights tailored to your portfolio, offering pre-analyzed opportunities that save time and effort.

Portfolio-Aware Analysis

ThetaEdge integrates with more than 80 brokerages, including Schwab, Fidelity, Interactive Brokers, and Robinhood, using secure, read-only access. Instead of starting with generic stock tickers, the platform evaluates your existing portfolio and identifies multi-leg strategies based on holdings, Greeks, volume, and momentum. Each opportunity is presented as a trade-off, not a recommendation, allowing you to weigh options like the higher cost and tighter breakevens of an at-the-money straddle against the lower entry cost and broader profit range of an out-of-the-money strangle.

You can fine-tune risk preferences to align with your goals - for example, filtering for opportunities with a 15% assignment risk. This customization ensures that the strategies presented match your risk tolerance. To date, the platform has analyzed over $300 million in assets, with users collectively earning $6.3 million in premiums through its insights. These features integrate seamlessly with decision-making tools, enhancing your ability to make informed choices.

Decision Support Tools

ThetaEdge goes beyond identifying opportunities by equipping you with tools to evaluate and refine your strategies. The Thetix AI assistant simplifies complex setups and runs "what-if" scenarios using live market data and your portfolio specifics. You can compare different strikes and expirations, visualizing the impact of time decay (theta) and volatility shifts on each position. Real-time monitoring of profit and loss (P&L) keeps you informed, with alerts triggered when profit targets are reached - such as a short strangle hitting 35% of its max premium - or when it's time to consider rolling a position.

"More people want to make their own destiny, and ThetaEdge empowers them to do it with the same tools the elite have always used".

Conclusion

When deciding between straddles and strangles, consider your goals and the current volatility environment. Straddles offer tighter breakevens and direct exposure to volatility, making them ideal for moderate implied volatility (IV). On the other hand, strangles come with lower costs and wider profit zones, making them more appealing in high IV conditions.

Market data underscores the importance of timing. For instance, long straddles tend to perform better in low-volatility environments, winning 58% of the time when IV percentiles are below 25%. However, their success rate drops to just 22% when IV exceeds 75%. Similarly, short sellers often target high IV percentiles (above 67%) and aim to lock in profits when they reach 50–70% of their maximum potential gain. These figures highlight the need to tailor your approach to the prevailing market volatility.

Your personal investment goals also play a key role. Strangles are generally more accessible for those with lower capital, offering volatility exposure at a fraction of the cost of straddles. For premium sellers, strangles often require less frequent adjustments since both legs start out-of-the-money, making them easier to manage over time.

"Straddles are the purest way to trade the implied vs realized move. You get the right feedback, and the right time, and are able to adjust your trades accordingly." - Sean Ryan, Options Trader

To help you make informed decisions, ThetaEdge provides cutting-edge analytical tools designed to integrate seamlessly with your portfolio. With features like real-time Greeks and comprehensive risk metrics, ThetaEdge enables you to evaluate the trade-offs between straddles and strangles, aligning your strategy with both market conditions and your investment objectives.

FAQs

How do I choose the right strikes for a strangle?

When picking strikes for a strangle, focus on out-of-the-money options that outline a price range you anticipate the asset will stay within until expiration. Strikes with delta values between 0.20 and 0.30 are often used, as they strike a balance between earning premium and the likelihood of the options being exercised. Remember, choosing wider strike ranges means the asset needs to make larger price moves for the trade to be profitable. Factor in market volatility and your personal risk tolerance when making these decisions.

How can I reduce IV crush risk on earnings trades?

Reducing the risk of implied volatility (IV) crush in earnings trades requires a thoughtful approach. Certain strategies are more vulnerable to the sharp drop in volatility that often follows an earnings announcement. For example, selling naked options or using short straddles and strangles can expose you to significant IV-related risks, making them less ideal in this context.

Instead, consider strategies that either thrive on pre-earnings volatility or are less impacted by the post-event drop. Buying straddles or strangles, for instance, can take advantage of the heightened IV and potential price movements leading up to the announcement. Additionally, leveraging portfolio-aware trading platforms can provide valuable insights into the risks and trade-offs of specific strategies, tailored to your current holdings. These tools can help you make more informed decisions while managing IV crush effectively.

When should I close a short straddle or short strangle?

You should exit a short straddle or short strangle before expiration to manage the unlimited risk these strategies carry and to prevent large losses. This is usually achieved by buying back the options if the underlying asset moves outside the range where the position remains profitable.