Covered Calls: Choosing the Right Strike for Maximum Premium

Strike selection balances premium, assignment risk, and upside—use delta and expirations to match goals and maximize covered-call income.

Covered calls let you generate income by selling call options on stocks you own. The key decision? Choosing the right strike price. This determines:

- Premium income: Higher premiums come with closer strikes.

- Assignment risk: Lower strikes increase the chance of losing your shares.

- Upside potential: Farther strikes allow more stock appreciation but offer smaller premiums.

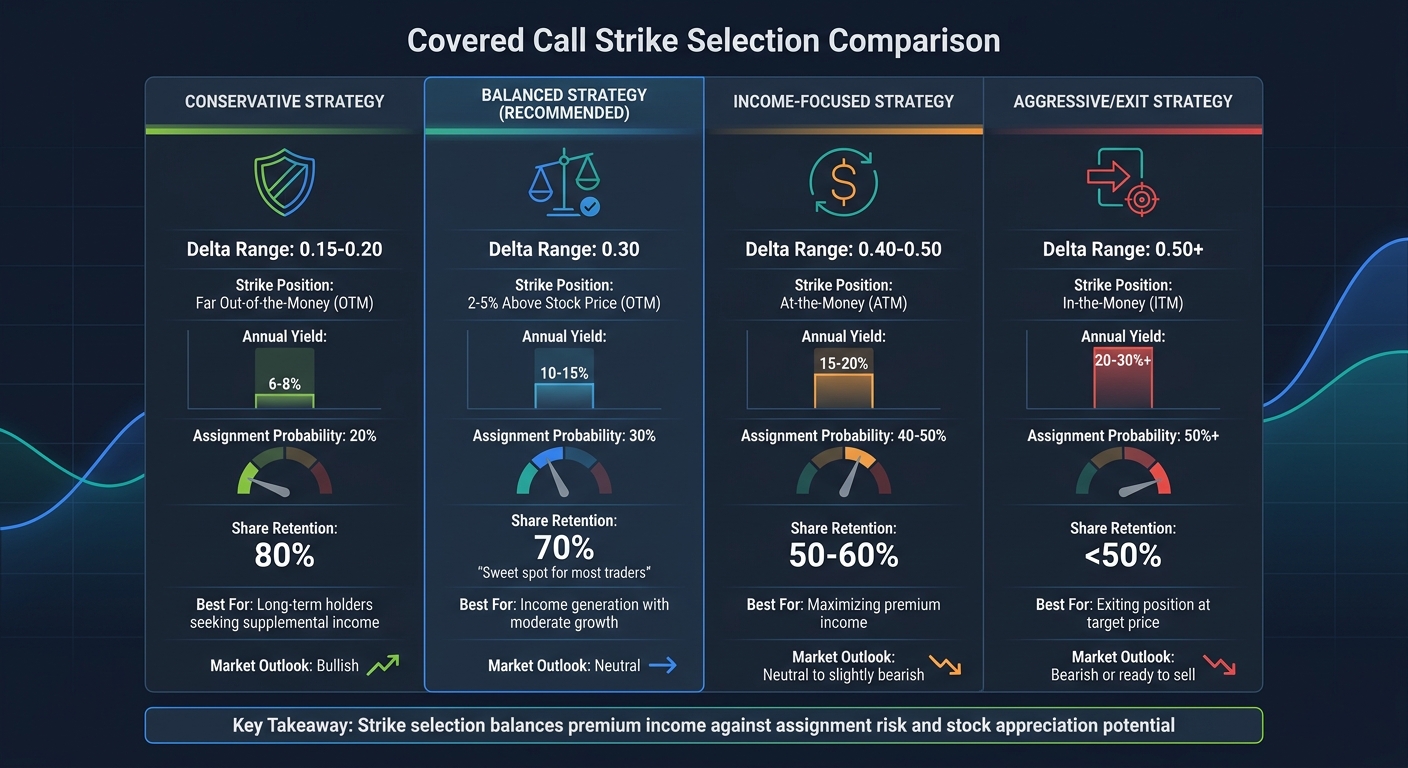

Key takeaway: Strike selection is about balancing income, risk, and your investment goals. For example:

- 0.30 delta strikes (2–5% above stock price) often yield 10–15% annually with a 30% assignment chance.

- 0.20 delta strikes are safer, with 6–8% annual yield and 80% share retention.

- 0.50+ delta strikes maximize income (20–30%+ annually) but come with high assignment risk.

The best choice depends on your market outlook and whether you want to hold or sell your stock. Below, we break down how to match strikes to your goals, calculate profits, and manage risk effectively.

Covered Call Strike Selection Guide: Delta Ranges, Returns, and Assignment Risk

Strike Price Trade-Offs: Premium Income vs. Stock Upside

How Strike Prices Determine Premium and Maximum Profit

The strike price you choose directly impacts both the premium you collect and the potential for stock gains. A strike closer to the current stock price offers a higher premium but limits your upside sooner. On the other hand, a strike further away reduces the premium but allows more room for the stock to grow before hitting the cap.

Take AMD trading at $155 in February 2026 as an example. A trader selling a $160 strike (0.30 delta) with 30 days to expiration earned $3.50 in premium ($350 total). If assigned, the trader would make $10 in capital gains ($160 strike minus $150 cost basis) plus the $3.50 premium, for a total of $13.50 per share ($1,350). Compare this to selling a $150 strike (in-the-money): the premium increases to $8.50, but the stock's potential for capital appreciation is eliminated since the sale price is already fixed.

A similar pattern emerges with Microsoft (MSFT) trading at $28 for a 46-day expiration. The $27 strike (in-the-money) offered a maximum gain of $52 (1.86% return) with 5.43% downside protection. The $28 strike (at-the-money) delivered a higher maximum gain of $91 (3.25% return) but with 3.25% downside protection. The $29 strike (out-of-the-money) provided the highest potential gain of $149 (5.32% return) but offered only 1.75% downside protection. As strikes move higher, premium income decreases, but the opportunity for stock appreciation increases.

"Strike selection is the balance between how much premium you collect and how likely you are to lose your shares." - QuantWheel

Balancing Income Goals with Risk Exposure

The examples above highlight the trade-offs between collecting premium income and preserving stock upside. The critical question is whether the premium compensates for the potential gains you're giving up. For instance, a 0.50+ delta (at-the-money or in-the-money) can generate annualized yields of 20-30% or more, but it comes with a 50%+ chance of your shares being called away. Conversely, a 0.20 delta (out-of-the-money) reduces the likelihood of assignment to 20%, but the annualized yield drops to 6-8%.

Your approach should align with your market outlook. If you're bullish, selling a lower-delta strike (0.15-0.20) allows for more stock appreciation while still earning some income. If you're neutral or considering selling the stock, a higher-delta strike (0.40-0.50) maximizes premium and increases the odds of assignment. For a bearish outlook, selling an in-the-money call with a 0.65 delta provides the highest premium and downside protection, though profit potential is limited to the option's extrinsic value.

One practical method to evaluate strike prices is to multiply the stock's 14-day ATR (average true range) by 1.5 or 2 and add it to the current price. If your strike falls below this level, it’s within the stock’s typical daily volatility range. This means you’re collecting premium for risk already embedded in the stock’s movement. While this isn’t inherently bad, it does increase the likelihood of assignment during routine price fluctuations.

sbb-itb-a9ac3c2

Using Market Outlook and Time Horizon to Select Strikes

Matching Strike Prices to Stock Price Expectations

Your market outlook plays a key role in determining the strike price that fits your strategy. For a bullish outlook, consider strikes with a 15–30 delta. These strikes keep assignment risk lower while still allowing room for upside gains. If your outlook is neutral, 30–40 delta strikes are more suitable. They strike a middle ground - providing solid premium income while keeping assignment risk manageable. A 30-delta strike, for example, often has about a 70% chance of expiring worthless, which means you’re likely to retain your shares. For a bearish perspective, your choice depends on your intent. If you’re ready to exit the position, 50+ delta strikes maximize both premium income and the exit price. On the other hand, if you plan to hold through the decline, a 20-delta strike offers some premium income while limiting assignment risk to roughly 20%.

"The 30-delta strike offers the best balance between premium collection and keeping your shares for most wheel strategy traders." - QuantWheel

If the stock experiences a sharp rise, you can adjust by lowering your delta range from 40–50 to 20–30 to reduce the likelihood of assignment.

| Market Outlook | Recommended Delta | Strike Zone | Primary Goal |

|---|---|---|---|

| Bullish | 15–30 Delta | Out-of-the-Money (OTM) | Capital gains + supplemental income |

| Neutral | 30–40 Delta | OTM / At-the-Money (ATM) | Maximize income |

| Bearish (Exiting) | 50+ Delta | In-the-Money (ITM) | Maximize exit price and premium |

| Bearish (Holding) | 20 Delta | Far OTM | Defensive premium collection |

Once you’ve identified the right strike range based on your outlook, the next step is refining your approach by considering the expiration timeline.

Factoring Time Horizon into Strike Selection

After aligning delta with your market expectations, the expiration date becomes the next critical factor. Your investment timeline will influence how far the strike price is from the stock’s current price while still delivering a worthwhile premium. Short-term expirations (7–14 days) often require strikes closer to the current price, while longer expirations (30–45 days) allow for further out-of-the-money strikes with lower deltas.

Weekly options decay faster, which means they demand more active management and often involve higher-delta strikes. On the other hand, monthly options (30–45 days to expiration) let you take advantage of the 21–30 day window where theta decay accelerates. This timeframe supports lower-delta strikes, offering flexibility and reduced assignment risk. For traders focused on generating income, shorter expirations paired with 40–50 delta strikes can work well. If your goal is stock growth, longer expirations with 15–20 delta strikes help minimize assignment risk while keeping growth potential intact.

Options typically lose around 50% of their extrinsic value in the last 21 days before expiration. Many traders prefer to close or roll their positions once they’ve captured about 50% of the maximum profit or when there are around 21 days left. This approach allows them to harvest theta efficiently while maintaining flexibility. By balancing premium income with risk, this method aligns well with a thoughtful covered call strategy.

Tools like ThetaEdge can provide visual aids and risk metrics, helping you fine-tune your strike and expiration choices to match your outlook and timeline effectively.

Calculating Profit, Breakeven, and Loss Scenarios

How to Calculate Maximum Profit and Breakeven Price

Understanding how to calculate potential profit and breakeven points is essential for aligning your strike price with your income and risk preferences. The formula for maximum profit is simple: (Strike Price - Stock Purchase Price) + Premium Received. This assumes the stock price reaches or exceeds the strike price by expiration. For example, if you purchase AMD at $150.00 and sell a $160.00 call for $3.50, your maximum profit would be $13.50 per share. This includes a $10.00 gain from the stock price increase plus the $3.50 premium.

The breakeven price shows how much the stock can drop before you start incurring a loss. It’s calculated as: Stock Purchase Price - Premium Received. Using the same AMD example, your breakeven would be $146.50. This means the stock could fall by $3.50 (or 2.3%) before you experience a net loss. The premium effectively lowers your cost basis, offering some downside protection.

For In-the-Money (ITM) calls, the calculation changes slightly because most of the premium consists of intrinsic value. In these cases, the maximum profit is limited to the extrinsic value of the premium, as the strike price is already below your purchase price. While this setup provides greater downside protection, it also significantly limits your upside.

"Never sell calls below your adjusted cost basis unless you want to realize a loss." - QuantWheel

These calculations help you evaluate how much downside protection your covered call strategy provides and whether it aligns with your goals.

Measuring Downside Protection and Loss Potential

Accurate calculations don’t just clarify potential profits; they also help you gauge the risks tied to your covered call position. It’s important to note that while premiums reduce downside risk, the protection they offer is limited. To measure this, you can calculate the downside protection percentage by dividing the premium received by the stock purchase price. For example, a $3.50 premium on a $150.00 stock gives you 2.3% protection. Stocks with high implied volatility, like NVDA or TSLA, can generate 3-5% monthly premiums, offering a more noticeable cushion. In contrast, blue-chip stocks like JNJ or KO typically yield only 0.5-1% per month.

If the stock price drops below your breakeven point, losses will grow in line with the stock’s decline. The maximum loss occurs if the stock’s value falls to zero, which would equal your stock purchase price minus the premium received. While such extreme scenarios are rare, this calculation underscores that covered calls don’t eliminate risk - they only reduce it slightly. Strike selection plays a critical role here: ITM strikes offer the most downside protection but sharply limit your upside, while OTM strikes provide less protection but allow for greater capital gains. Choosing the right strike price is key to balancing premium collection with stock appreciation.

Many seasoned traders prefer to close or roll their positions after capturing 50% of the maximum profit. This approach helps reduce exposure to sudden market reversals while keeping their strategy flexible. Tools like ThetaEdge can assist in visualizing profit and loss scenarios across various strike prices, making it easier to align your choices with your risk tolerance and investment timeline.

Matching Strike Prices to Your Investment Goals

When choosing strike prices, the key is to ensure they align with your investment objectives. Whether you're aiming to exit a position profitably or hold for long-term growth, your strike decision hinges on balancing assignment probability with the capped upside.

"Strike selection is about aligning your choice with your investment goal." - QuantWheel

Delta is a helpful tool here. It gives you a rough estimate of assignment probability: a 0.50 delta means a 50% chance of assignment, while a 0.20 delta lowers that to about 20%. By understanding delta, you can tailor your strike selection to match your specific goals.

Strike Selection When You Want to Sell Your Stock

If your goal is to sell your shares, consider at-the-money (ATM) or in-the-money (ITM) strikes. These options provide the highest premiums and increase the likelihood of assignment. A delta of 0.50 or higher is ideal for maximizing both income and the probability of selling your shares.

For instance, selling a $150.00 ITM call on AMD, trading at $155.00, could earn you an $8.50 premium. This approach not only captures significant extrinsic value but also positions you for a likely exit at your chosen price.

However, it's important to avoid selling calls below your adjusted cost basis. For example, if you bought the stock at $160.00, selling a $155.00 call just to collect a premium could lock in a loss if assigned. Instead, focus on strikes that allow a profitable exit while still generating strong income. Historical data shows that aggressive strike selection with a 0.50+ delta can yield annual returns of 20-30%, compared to 6-8% for more conservative 0.20 delta strikes.

If your intention is to hold onto your shares for longer-term growth, a different approach is necessary.

Strike Selection When You Want to Keep Your Stock

For those focused on long-term growth but looking to generate supplemental income, out-of-the-money (OTM) strikes are the way to go. Strikes with a delta between 0.15 and 0.30 work well here, as they keep assignment risk low while still offering worthwhile premiums. A 0.30 delta strike gives you about a 70% chance of retaining your shares, while a 0.20 delta strike raises that to 80%.

"Choosing a strike too far out yields minimal premium. You've committed your shares for an entire cycle to collect $25. Pick a strike too close, and a normal rally pulls your shares away." - Mike Thornton, The Multiplier

To refine your strategy, consider using the 14-day Average True Range (ATR) method. Multiply the ATR by 1.5 to 2 and add it to the current stock price. This buffer helps you set strikes beyond typical price swings, reducing the risk of assignment. Additionally, avoid selling calls that expire during earnings periods, as unexpected price jumps from earnings surprises can push your strike into the money.

Conservative 0.20 delta strikes typically offer annual returns of 6-8%, while balanced 0.30 delta strikes can yield 10-15%. The trade-off is simple: lower assignment risk means lower premiums, but you retain the potential for stock appreciation, which is critical for long-term holdings.

Selecting Expiration Dates to Optimize Premium Income

Choosing the right expiration date plays a key role in shaping your covered call strategy. It influences how much premium you can collect, how often you'll trade, and how much time you’ll spend managing your positions. Longer expirations typically offer higher premiums because they account for more potential price movement, but they may not always align with your goals or trading style. Just as selecting a strike price balances premium and risk, picking an expiration date fine-tunes your income strategy.

As a covered call seller, you benefit from time decay - referred to as theta. However, theta doesn’t erode evenly over time. Instead, it starts off slowly and speeds up significantly as the expiration date nears. The challenge is to match the expiration period with both your income goals and the time you’re willing to invest in managing your portfolio.

"The theoretical rate of decay will tend to increase as time to expiration decreases. As a result, the amount of theta is usually gradual at first and accelerates as the expiration date approaches." - Snider Advisors

Balancing Expirations with Your Strategy

Different expiration periods offer distinct advantages depending on how actively you want to manage your portfolio and how much premium income you’re targeting:

- Weekly options (7–14 days): These take advantage of the fastest theta decay, allowing you to collect premiums more frequently - up to four times a month. However, they require more hands-on management and often involve selecting closer strike prices to generate meaningful income.

- Monthly options (30–45 days): This range is often considered the sweet spot. Theta decay begins to accelerate after 30 days, providing a balance between premium collection and manageable trading frequency. Many traders favor expirations in the 21–30 day range for this reason.

- Long-term options (90 days to six months): If you prefer a less active approach, longer expirations work well. They allow you to check your portfolio less frequently - just a few times a year - while still collecting reasonable premiums.

A good rule of thumb is to aim for a premium of about 2% of the stock’s value for the expiration period you choose. Monthly options also tend to offer better liquidity compared to weeklies, resulting in tighter bid-ask spreads and less slippage. To further optimize your strategy, consider closing or rolling positions when they reach 50% of their maximum profit, especially with 21 days or fewer until expiration. This resets the decay cycle and helps lock in gains efficiently.

Managing Positions and Responding to Assignment Risk

Once you've sold a covered call, your job isn't done. Keeping an eye on your position as stock prices shift and expiration dates approach is crucial. The goal? Knowing when to accept assignment, compare covered calls vs cash-secured puts to adjust your strategy, or let your shares go.

What to Do When Assignment Occurs or Is Imminent

Assignment happens when the buyer exercises their right to purchase your shares at the strike price. If your call moves in-the-money as expiration nears, you have a few options: accept assignment, close the position early, or roll the contract to a new strike or expiration date.

Rolling involves buying back the existing call and selling a new one, typically at a higher strike and later expiration. This can give your stock more room to appreciate while earning additional premium. However, rolling only makes sense if you can collect a net credit. Paying to extend the position turns an income-focused strategy into a cost.

There are times when rolling is no longer practical:

- If the new expiration date stretches beyond six months

- If rolling fails to generate a net credit

- If your market outlook changes significantly

Some traders prefer to close positions once they've captured 50% of the maximum profit, using the opportunity to start a new position.

"If you haven't accepted that selling a call means you might sell your shares, you're not ready to write calls." - Mike Thornton, The Multiplier

If you do get assigned, resist the urge to repurchase shares at inflated prices. Instead, consider selling a cash-secured put to earn premium while waiting to re-enter at a more favorable price.

Adjusting Positions When Stock Prices Shift

Beyond assignment risk, stock price movements often require you to tweak your strategy. If your stock rallies and your call moves deep in-the-money, you can roll the position up and out - adjusting to a higher strike and later expiration - but only if this adjustment results in a net credit. If the call's delta reaches 0.80, rolling may no longer make sense, and accepting assignment could be the better option.

If the stock drops, you can roll to a lower strike to earn more premium and improve downside protection. However, avoid setting the strike below your adjusted cost basis (the purchase price minus premiums collected), as this could lock in a loss.

To manage risk during volatile periods, consider staggering your expirations across different weeks. This reduces the likelihood of multiple positions facing assignment during a market rally. Additionally, avoid selling calls right before earnings announcements - unexpected overnight price jumps of 10–15% can push the stock far beyond your strike price before you have a chance to act.

| Market Condition | Position Adjustment After Price Moves | Target Delta |

|---|---|---|

| Bullish (Rising) | Roll up and out to a higher strike | 20–30 Delta |

| Neutral (Sideways) | Close at 50% profit and reset | 30–40 Delta |

| Bearish (Declining) | Roll to a lower strike to recapture premium and improve downside protection | 20 Delta |

| Exiting Position | Sell in-the-money calls | 50+ Delta |

(Source for delta targets:)

Effectively managing your positions after the initial sale is just as important as picking the right strike price. By balancing income generation with risk control, you can keep your strategy on track.

Conclusion

Choosing the right strike price comes down to three key factors: your market outlook, investment goals, and risk tolerance. The balance between earning premium income and maintaining stock upside is at the heart of this decision. For those seeking higher premium income with an increased chance of assignment, strikes in the 0.30–0.40 delta range can deliver annual returns of 10–20%. Many traders gravitate toward a 0.30 delta strike, which often provides a balanced outcome - annual premiums of 10–15% and about a 30% chance of assignment.

"Premium isn't free. It's what you get paid for capping your upside" - Mike Thornton, The Multiplier

Timing plays a major role in maximizing returns. Selling calls during periods of elevated implied volatility can boost premiums, while sticking to 30–45 day expirations often captures the most effective theta decay. It's also wise to align strikes with technical resistance levels and avoid selling below your adjusted cost basis unless you're prepared to lock in a loss. This straightforward approach can help streamline decision-making and protect your returns.

For self-directed investors juggling multiple positions, evaluating every trade-off manually can feel daunting. ThetaEdge simplifies this process by connecting directly to your portfolio across 80+ brokerages, highlighting covered call opportunities tailored to your holdings. It provides a comprehensive view, including risk analysis, assignment probabilities, breakeven points, and payoff scenarios. Its AI assistant, Thetix, answers portfolio-related questions in plain English, and continuous monitoring ensures you're alerted when positions require adjustments or rolling.

"Every month without a systematic approach is premium income left on the table" - ThetaEdge

The key takeaway? Consistently turning analysis into action is what drives results.

FAQs

What delta should I use for covered calls if I want to keep my shares?

To find a middle ground between earning premium income and minimizing the risk of your shares being called away, aim for a strike price with a delta of approximately 0.30 (30%). This strategy allows you to collect a fair premium while improving the chances of holding onto your shares.

How do I pick a strike that won’t get hit by normal volatility?

When aiming to manage the impact of normal market fluctuations, look for options with a delta in the range of 0.30 to 0.40. This range strikes a balance between collecting a decent premium and minimizing the likelihood of your shares being called away. Prioritize out-of-the-money strikes and time your call sales during periods of moderate implied volatility (IV). Steering clear of high-IV environments can help reduce the risk of sudden price swings disrupting your strike. These practices can help you manage risk effectively while still earning premium income.

When should I roll or close a covered call to reduce assignment risk?

If the stock price approaches the strike price, particularly within 14-21 days of expiration, it might be wise to think about rolling or closing your covered call to lower the risk of assignment. However, avoid rolling too soon unless you've already secured at least 50% of the profit. Pay close attention to your positions during periods of high volatility or around ex-dividend dates. These moments can increase the likelihood of unexpected assignment, so careful monitoring can help you manage risks while still aiming to maximize your income.