How Vega Impacts Portfolio Risk

Net vega can turn steady income trades into sudden losses—manage vega or risk catastrophic drawdowns.

Vega measures how sensitive an option's price is to changes in implied volatility. For every 1% change in volatility, vega shows the dollar impact on the option's price. This makes it a crucial metric for options traders managing risk, especially during events like earnings announcements or market shocks.

Key points about vega:

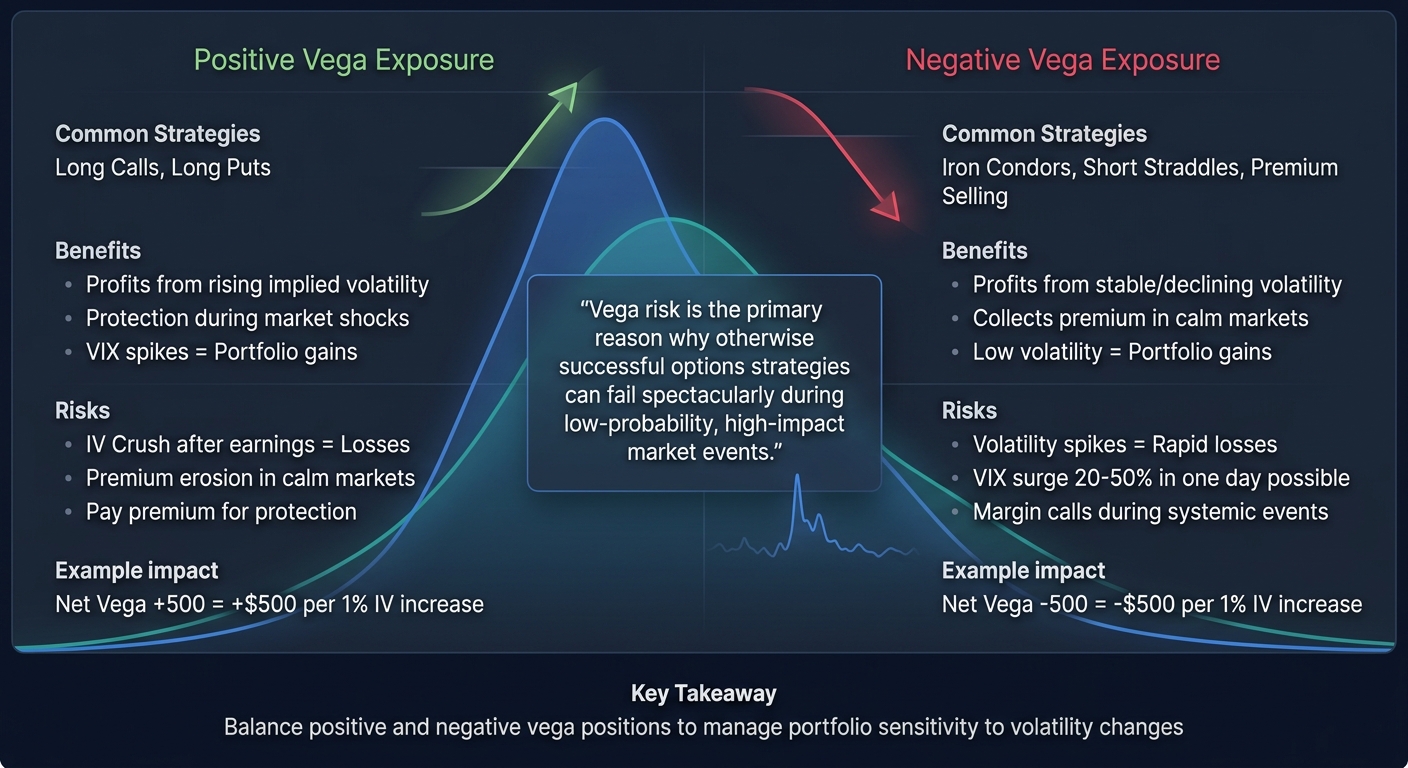

- Positive Vega: Found in long options (calls or puts). Profits from rising volatility but loses when volatility drops (e.g., "IV crush").

- Negative Vega: Found in premium-selling strategies (Iron Condors, Short Straddles). Benefits from stable or declining volatility but risks losses during volatility spikes.

-

Factors Influencing Vega:

- Time to Expiration: Longer-dated options have higher vega.

- Moneyness: At-the-money (ATM) options have the highest vega.

- Stock Price: Higher-priced stocks result in higher vega.

Managing vega involves balancing portfolio exposure to volatility shifts. Techniques include:

- Vega-Neutral Portfolios: Offsetting positive and negative vega positions.

- Vertical Spreads: Reducing vega sensitivity while limiting risk.

- Adjustments During High Volatility: Reassessing exposure and using spreads or VIX-linked products to hedge.

Tracking tools like ThetaEdge can simplify monitoring portfolio vega and provide tailored insights to help traders manage risk effectively.

How Vega Affects Portfolio Risk

Positive vs Negative Vega Exposure: Impact on Options Portfolio Risk

Understanding what vega measures is just the beginning - next comes assessing how it impacts your portfolio's risk. Your Net Vega, which is the total of all individual position vegas, reveals how sensitive your portfolio is to changes in implied volatility. For example, a Net Vega of -500 indicates that your portfolio would lose $500 for every 1-point increase in implied volatility. This becomes especially critical during market shocks, where the VIX can surge by 20% to 50% in a single day. Such rapid shifts can turn otherwise manageable positions into significant losses. Let’s explore how the direction of your vega exposure affects portfolio performance.

Positive vs Negative Vega Exposure

The way your portfolio reacts to volatility changes depends largely on whether you have positive or negative vega exposure. Positive vega positions, often held by buyers of calls and puts, benefit from increasing implied volatility but face losses during an "IV crush", which happens when volatility contracts after events like earnings announcements. On the other hand, negative vega positions, such as those created through premium-selling strategies like Iron Condors or Short Straddles, thrive in stable or declining volatility but are vulnerable to sharp volatility spikes.

"Vega risk is the primary reason why otherwise successful options strategies can fail spectacularly during low-probability, high-impact market events." – QuantStrategy.io Team

Volatility buyers often pay a premium for protection, which can yield significant rewards during turbulent times. However, that premium erodes steadily in calm market conditions. Balancing these exposures is crucial for fine-tuning your options strategy when market volatility fluctuates.

Vega's Role in Value at Risk (VaR) Calculations

Vega exposure also plays a significant role in Value at Risk (VaR) calculations, a key metric for estimating potential losses over a specific period. High net vega amplifies your portfolio's sensitivity to volatility shocks, potentially leading to rapid capital losses or even margin calls during systemic events. For example, if you're running a short-premium strategy with significant negative vega during a period of market uncertainty, your VaR must account for the possibility of implied volatility surging beyond typical levels. Traders often adjust their Net Vega accordingly - neutralizing it in times of high uncertainty or maintaining slight negative exposure when volatility is low.

Managing vega exposure is not just about mitigating risk but also ensuring your portfolio remains resilient under varying market conditions.

sbb-itb-a9ac3c2

How to Manage Vega Risk

Once you understand how vega influences your portfolio, the next step is to actively manage it. The goal isn’t to eliminate vega entirely but to keep it under control, especially during periods of market turbulence. This involves balancing positions, using specific spread strategies, and making tactical adjustments when volatility spikes. These methods allow you to adapt as market conditions evolve.

Building Vega-Neutral Portfolios

A vega-neutral portfolio is designed to minimize sensitivity to changes in implied volatility. The concept is straightforward: the portfolio’s total vega adds up to zero. To achieve this, calculate the net vega by summing the vegas of all positions - long options contribute positive vega, while short options contribute negative vega. For instance, if your portfolio has a net vega of -300, you’d need to add positions with positive vega to offset this exposure. Use the formula N = Vₚ / Vₐ, where Vₚ is the portfolio’s net vega and Vₐ is the per-unit vega of the option, to determine the number of contracts needed.

Keep in mind that implied volatility isn’t uniform across maturities, so it’s important to account for each position’s time to expiration when managing vega. For broader protection, products linked to the VIX, such as VIX futures, VIX calls, or exchange-traded products like VXX, can be effective. These instruments typically carry high positive vega and tend to perform well during market-wide volatility spikes. Additionally, structural hedges like ratio backspreads - where you buy more options than you sell - can help add positive vega to portfolios that are short volatility.

"A vega-neutral strategy makes profits from the bid-ask spread of implied volatility or the skew between the volatilities of the calls and puts." – CFI Team

Using Vertical Spreads to Control Vega

Vertical spreads are a practical way to manage vega exposure while keeping risks defined. This strategy involves buying and selling options at different strike prices but with the same expiration date. The positive vega from the long option is partially offset by the negative vega from the short option, reducing the overall sensitivity to volatility changes.

For more precise vega adjustments, ratio spreads can be used to modify the number of options bought versus sold. Butterfly spreads, which combine multiple vertical spreads, are another popular choice for creating vega-neutral setups. These strategies allow traders to focus on other factors, such as how time decay impacts options, while keeping vega exposure in check. One major advantage of vertical spreads is that they limit your potential losses while maintaining low vega sensitivity, offering protection against large portfolio swings during volatile periods.

Adjusting Positions During High Volatility

When volatility spikes, it’s essential to reassess and adjust your positions. Start by recalculating your net vega to understand your exposure. During uncertain times - like before major Federal Reserve announcements or geopolitical events - traders often aim to neutralize their net vega to mitigate risk.

If you hold positive vega positions, consider selling short-term, at-the-money options to lock in gains and offset elevated premiums. For those using negative vega strategies, such as Iron Condors, high volatility requires careful adjustments. Transform naked short options into vertical spreads to cap potential losses and reduce sensitivity to volatility. Calendar and diagonal spreads are also effective in these scenarios, as their longer-dated legs introduce positive vega, providing a buffer against sudden changes in implied volatility. As before, use the formula N = Vₚ / Vₐ to fine-tune your portfolio’s vega exposure.

Tools for Tracking Vega Exposure

Managing vega effectively requires tools that provide real-time monitoring. Without these, traders can unknowingly take on excessive vega risk, especially when positions tied to similar volatility factors stack up. This can be particularly harmful to those focused on collecting theta, as they might carry significant negative vega exposure, leaving their portfolio vulnerable during a volatility spike. The right tracking tools are essential for implementing sound vega management strategies, enabling traders to anticipate and adapt to shifts in volatility with precision.

Portfolio Greeks Analysis

To manage vega across a portfolio, it's crucial to aggregate individual position Greeks into a unified view. Portfolio vega represents the potential gain or loss across all holdings for every one-percentage-point change in implied volatility. This comprehensive perspective can uncover hidden risks, such as sector-specific exposure or directional imbalances, which might not be apparent when reviewing positions individually.

"Portfolio Greeks tell you whether your entire book is about to get wrecked by a single market move." – AInvest Options Pilot Research

Advanced tools update Greeks and P&L within seconds, allowing traders to respond quickly to sudden market changes. Many platforms also offer stress testing features, enabling users to simulate scenarios like an implied volatility (IV) crush after earnings or a sharp market drop. These simulations help traders assess how such events might impact vega and overall portfolio performance. Monitoring portfolio vega daily, especially before key events like Federal Reserve announcements or major earnings reports, is a critical habit.

During times of market stress, correlations often converge, meaning positions that seem diversified can move in tandem. Tools designed to account for these shifts help traders understand how a single sector's volatility could impact multiple positions simultaneously.

Using ThetaEdge for Vega Management

One standout tool for vega management is ThetaEdge, designed specifically for self-directed investors. Unlike generic platforms that analyze tickers in isolation, ThetaEdge connects directly to over 80 brokerages via read-only access to analyze your actual holdings. This ensures that every recommendation is tailored to your portfolio.

"ThetaEdge analyzes your actual holdings, not generic tickers, so every opportunity is filtered, ranked, and contextualized before it reaches you." – ThetaEdge

With its Thetix AI assistant, ThetaEdge allows users to ask plain-language questions like, "What’s my net vega exposure?" or "How would a 5-point VIX spike affect my positions?" The platform provides answers based on live data, along with concentration risk alerts and AI-driven explanations. These features help pinpoint where vega exposure is concentrated and suggest potential adjustments. By offering these insights, ThetaEdge empowers traders to make proactive decisions and maintain a balanced options portfolio in volatile markets.

ThetaEdge is available for $999 per year ($83.25 per month, billed annually) and includes a 30-day free trial with no credit card required. While the platform provides detailed risk analysis and tracking, it does not execute trades or offer investment advice, leaving all final decisions in the hands of the user.

Conclusion

Vega measures the dollar change in an option's price for every 1% shift in implied volatility. It's a key factor in managing options risk and demands close attention. For instance, if your portfolio has a net vega of –500, a 1-point increase in volatility during a market stress event could result in a $500 loss.

To manage this risk effectively, consider implementing strategies tailored to counteract vega exposure. Techniques like constructing vega-neutral portfolios, using calendar or diagonal spreads, and adding VIX hedges can help stabilize your portfolio's performance and reduce the impact of market turbulence.

"You don't have to fear Vega, but you do have to respect it. Hedging Vega isn't about eliminating risk - it's about smoothing your equity curve and avoiding sharp drawdowns".

Additionally, advanced tracking tools can enhance your risk management approach. Platforms like ThetaEdge and portfolio Greeks analysis offer real-time insights and tailored recommendations, making it easier to respond to sudden volatility spikes. By combining these strategies with robust tracking tools, you can better navigate unpredictable markets and shield your portfolio from unexpected volatility.

FAQs

What net vega is too risky for my account size?

The amount of net vega that becomes too risky varies based on your account size and how much risk you're comfortable taking on. As a general guideline, having a high positive or negative vega - anything beyond 5-10% of your account's value - can significantly increase your exposure to market swings, particularly when volatility changes unexpectedly. Keeping a close eye on your vega exposure and managing it carefully is crucial to protecting your portfolio from large losses during sudden spikes in volatility.

How can I hedge negative vega before earnings or the Fed?

Managing negative vega ahead of major events like earnings reports or Federal Reserve announcements requires careful planning. To handle volatility risk, you might explore tools like VIX futures or options, which are specifically designed for volatility management.

Other strategies to consider include:

- Ratio spreads: These can help balance your exposure by adjusting the number of options contracts at different strike prices.

- Calendar spreads: Useful for capitalizing on differing volatility levels between short-term and long-term options.

- Protective puts: These provide a safety net by limiting downside risk, especially during unpredictable volatility spikes.

These tactics are particularly relevant during times of elevated implied volatility. They can help you navigate sudden volatility changes while keeping portfolio risk under control.

How does vega change as options move ITM or OTM?

When an option moves closer to being at-the-money (ATM), vega increases. On the other hand, vega tends to decrease as the option shifts deeper into in-the-money (ITM) or out-of-the-money (OTM) territory. This happens because vega measures sensitivity to implied volatility, which peaks near ATM but fades as options drift further into ITM or OTM zones.